[ad_1]

Talks of a US recession look like off the desk for now, however customers are nonetheless struggling to maintain up with bank card funds, as proven by the newest information from FICO. Balances rose once more in December, as did the energetic playing cards fee. Delinquency charges had been additionally greater, although not rising as quick because the earlier 12 months. Listed here are the US Credit score Card and Client Spending Highlights:

Financial Context

Many economists (roughly 76% of these surveyed) consider the prospect of recession is 50% or much less, in accordance with a December survey from the Nationwide Affiliation of Enterprise Economics. Listed here are a few of the indicators:

-

The US Actual Gross Home Product (GDP) ended 2023 with a 2.5% enhance over the 2022 annual stage as launched by the U.S. Bureau of Financial Evaluation. Main causes for the optimistic outcomes had been will increase in client bank card spending in areas of service and items (led by well being care and leisure items and autos).

-

U.S. Retail and meals gross sales transactions, reported by the U.S. Census Bureau, elevated 0.6% from November to December and are up 5.6% year-over-year. It is very important notice that gross sales are adjusted for seasonal variation and vacation and trading-day variations, however not for worth change.

- The U.S. Bureau of Labor statistics introduced the unemployment fee was regular at 3.7% in December and is 0.2% greater than December 2022. These figures stay higher than anticipated when in comparison with the Federal Reserve’s forecast that unemployment would rise to 4.1% by the tip of 2023.

-

The typical APR on a 30-year mounted fee mortgage has decreased over the previous two months after peaking at 7.8% in October. Common charges are regular round 6.7%.

-

The speed of Inflation (the year-over-year comparability of the Client Worth Index) was reported at 3.4% in December. The Client Worth Index seems to have peaked for now with month-over-month decreases since October 2023.

-

The Federal Funds Efficient Price has been held at 5.25%-5.5% because the final fee enhance in July regardless of hypothesis that there can be one other enhance of 0.25% earlier than year-end. Because of decrease inflation, the Federal Reserve is now penciling in fee cuts for 2024 starting in March.

There are conflicting headlines concerning how extreme bank card losses might be over the subsequent two years. Capital One believes their bank card delinquency and subsequent losses might not transform as unhealthy as what was predicted shortly following the pandemic. However, Goldman Sachs launched a report citing “bank card firms are racking up losses on the quickest tempo in nearly 30 years, outdoors of the Nice Monetary Disaster.” The report concludes that losses might not peak till the tip of 2024/starting of 2025.

Thankfully, a number one indicator to loss is bank card delinquency. The information shared under from FICO® Advisors’ Danger Benchmarking resolution exhibits an upward pattern in bank card delinquency, however this seems to be flattening during the last a number of months. We’ll dig into bank card delinquency developments, in addition to different credit score rating figures that characterize a nationwide pattern of roughly 130 million US accounts gathered from FICO shopper experiences generated by FICO® TRIAD® Buyer Supervisor and Adaptive Management System options.

Credit score Card Utilization and Funds

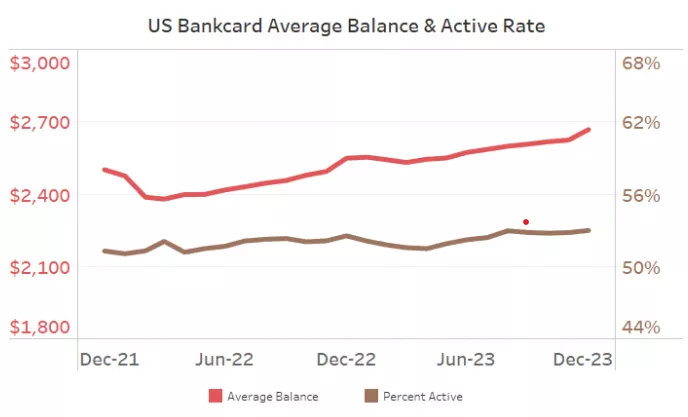

With elevated rate of interest inflation, elevated spend on journey and leisure, and a better value to carrying bank card debt, bank card balances have been climbing constantly for almost two years.

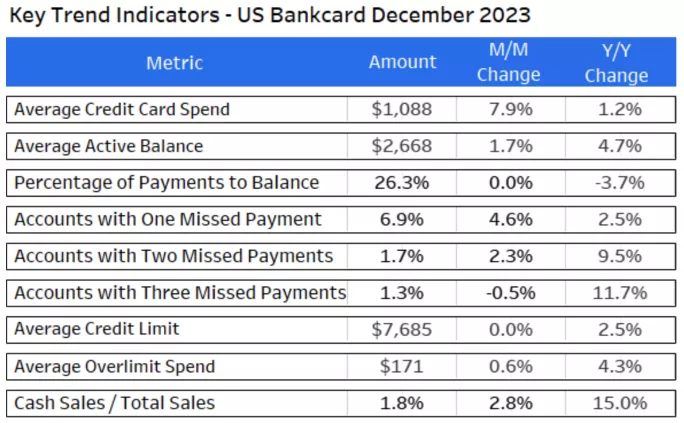

The typical bank card steadiness completed off 2023 at $2,668, a 4.7% enhance in comparison with December 2022. The speed of a client utilizing their bank card for transactions additionally continues to rise. December’s energetic fee of 53.0% is one other half a share level greater than final December and higher than three share factors greater than the pre-COVID common.

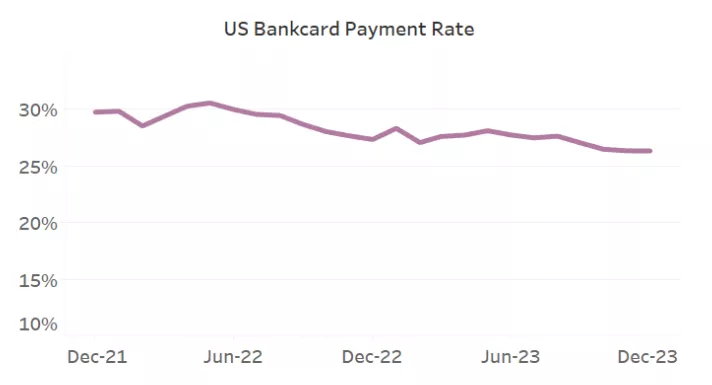

The bank card trade cost fee (share of earlier month’s steadiness that was paid again) continues its downward slide since peaking in mid-2022 at 30.6%. December’s bank card debt cost fee was 26.3%, which stays greater than the pre-COVID fee of 23.0%. Fewer clients pay their bank card debt steadiness in full (45.1% vs. 48.5% in December 2021) and extra clients are paying solely the minimal due on their bank cards (8.0% vs. 6.7% in December 2021).

Credit score Card Delinquency Charges

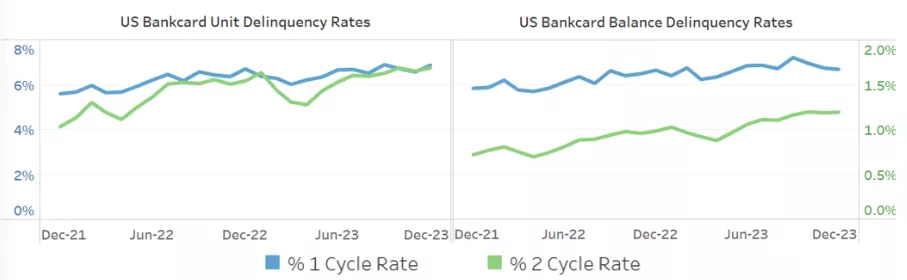

As talked about above, Goldman Sachs predicts that bank card losses will peak in late 2024 or early 2025. Equally, the 1-cycle delinquency developments from the US bankcard trade proven under point out that unit and steadiness delinquency charges of bank cards might have began to stage off resulting in the potential of decrease losses in roughly six months.

The proportion of bank card accounts which have missed one cost grew 2.4% year-over-year compared to the 19.9% development from December 2021 to December 2022. An identical smoothing impact has occurred with the 1-cycle steadiness fee, solely rising 0.5% year-over-year in comparison with the 13.9% enhance from December 2021 to December 2022.

Though the speed of client bank card accounts and balances lacking two funds has been calmer as properly, there have been nonetheless substantial will increase year-over-year, 9.7% and 21.4% respectively. This compares to the year-over-year will increase of 49.5% and 36.1%, respectively, from December 2021 to December 2022.

We’ll proceed to look at the macro surroundings change, as decrease rates of interest usually tend to have a optimistic affect on customers and issuers alike. It’s vital as a danger supervisor to observe bank card delinquency charges often together with repeatedly updating loss forecast fashions. If you’re a client who’s struggling, there are instruments obtainable at myFICO.com to assist preserve monitor of bank card utilization and your FICO Rating.

Bank card issuers can attain out to your FICO Resolution Success Advisor or FICO Key Account Managers for a dialogue and evaluation, in case you need assistance finishing an analysis of your portfolio.

You probably have questions or are fascinated about discussing these insights in additional element, please go away a touch upon this put up.

How FICO Can Assist You Handle Credit score Card Danger and Efficiency:

[ad_2]

Source link