[ad_1]

The worldwide push for monetary inclusion has led to the event of revolutionary monetary merchandise designed particularly for the unbanked and underbanked inhabitants. These people, who’ve historically been excluded from the formal monetary system, at the moment are getting access to a variety of providers, together with financial institution accounts, e-wallets, pre-paid playing cards, loans, and digital fee platforms. Whereas this progress is undoubtedly optimistic, it additionally exposes these weak teams to new and distinctive fraud dangers.

Fraudsters are fast to take advantage of any vulnerabilities within the system, and the unbanked and underbanked inhabitants is especially inclined attributable to a mixture of things, together with low monetary literacy, lack of monetary schooling, and restricted expertise with formal monetary providers. As we work in direction of increasing monetary inclusion, it’s essential that we additionally prioritize defending these people from fraud and monetary exploitation not solely by means of present methods, but additionally new, revolutionary and customized options.

Balancing Development and Fraud Safety

The fast enlargement of real-time funds, digital banks and fee service suppliers (PSPs) has introduced new alternatives for monetary inclusion, however it has additionally raised issues in regards to the prioritization of progress over fraud safety. As these establishments concentrate on buying new clients and rising market share, there’s a danger that they might overlook the significance of sturdy fraud prevention measures.

Conventional fraud safety strategies might not be efficient in defending the unbanked and underbanked inhabitants, who’ve distinctive vulnerabilities and restricted expertise with formal monetary providers. It’s essential for banks and PSPs to develop fraud fashions and guidelines which are tailor-made to the particular wants and circumstances of this demographic.

Fraud prevention measures ought to think about the potential influence of even small losses on low-income people and households. What might seem to be a nominal quantity to a monetary establishment could be devastating for somebody dwelling in poverty. As such, fraud thresholds and response protocols have to be adjusted to reduce the hurt brought on by fraudulent actions.

Monetary establishments should strike a fragile stability between enabling entry to monetary providers and defending customers from fraud. TJ Horan, FICO’s vice chairman of product administration, factors to “smart friction” – guaranteeing that we stability the benefit and pace of cash motion with the correct controls and buyer communication alongside the best way, to determine and deal with potential pink flags.

This requires a proactive method to fraud prevention that leverages superior applied sciences, resembling machine studying and synthetic intelligence, in addition to efficient and bespoke buyer communication and engagement to detect and stop fraudulent actions in real-time.

A few of the concerns which are price maintaining in thoughts are centered on the therapy and communication:

- If you wish to entice extra of the underbanked inhabitants, how will you adapt your messaging & therapy?

- Do you might have the pliability to phase your buyer base, and permit numerous buyer teams for:

- completely different limits

- tailor-made fraud methods

- bespoke fraud messaging flows

- At what level of your buyer journey do you graduate a buyer from an underbanked method of therapy?

- What does the client journey in monetary literacy and banking expertise appear like?

- How do you mature your therapy and communications alongside that?

The Significance of Monetary Literacy

Probably the most important challenges in defending the unbanked and underbanked from fraud is the widespread lack of monetary literacy. A global research led by the OECD discovered that simply 17% of surveyed adults (each banked and unbanked) thought-about their monetary data to be excessive. And whereas the overwhelming majority had been conscious of the monetary merchandise obtainable to them, 20% nonetheless turned to household and buddies for borrowing or saving. This lack of understanding or understanding makes it tough for people to navigate the monetary system and make knowledgeable selections about their cash.

The Findex report discovered that about two-thirds of unbanked adults would want assist utilizing an account in the event that they opened one at a monetary establishment. This highlights the necessity for accessible and complete monetary teaching programs that may assist people perceive and make the most of monetary providers successfully.

Lack of belief in monetary establishments is a big barrier to monetary inclusion, significantly among the many unbanked inhabitants. Within the Philippines, for instance, 15% of unbanked people cite an absence of belief as their major purpose for not opening an account. A current FICO research highlights that 69% of respondents view sturdy fraud safety as one of many prime three most necessary concerns when opening a checking account. Belief is important for changing the unbanked to the banked, and poor fraud controls can rapidly erode this belief, turning folks away from utilizing formal monetary providers.

Governments and policymakers have an important function to play in addressing this difficulty. They need to spend money on rules and governance that guarantee the provision of protected, inexpensive, and handy monetary merchandise for all in addition to concentrate on focused monetary literacy initiatives that cater to the particular wants of the unbanked and underbanked inhabitants. These packages needs to be a collaborative effort between regulators and monetary establishments, designed to assist people construct the abilities and confidence they should have interaction with the formal monetary system and defend themselves from fraud and exploitation.

The Function of Digital Identification in Monetary Inclusion

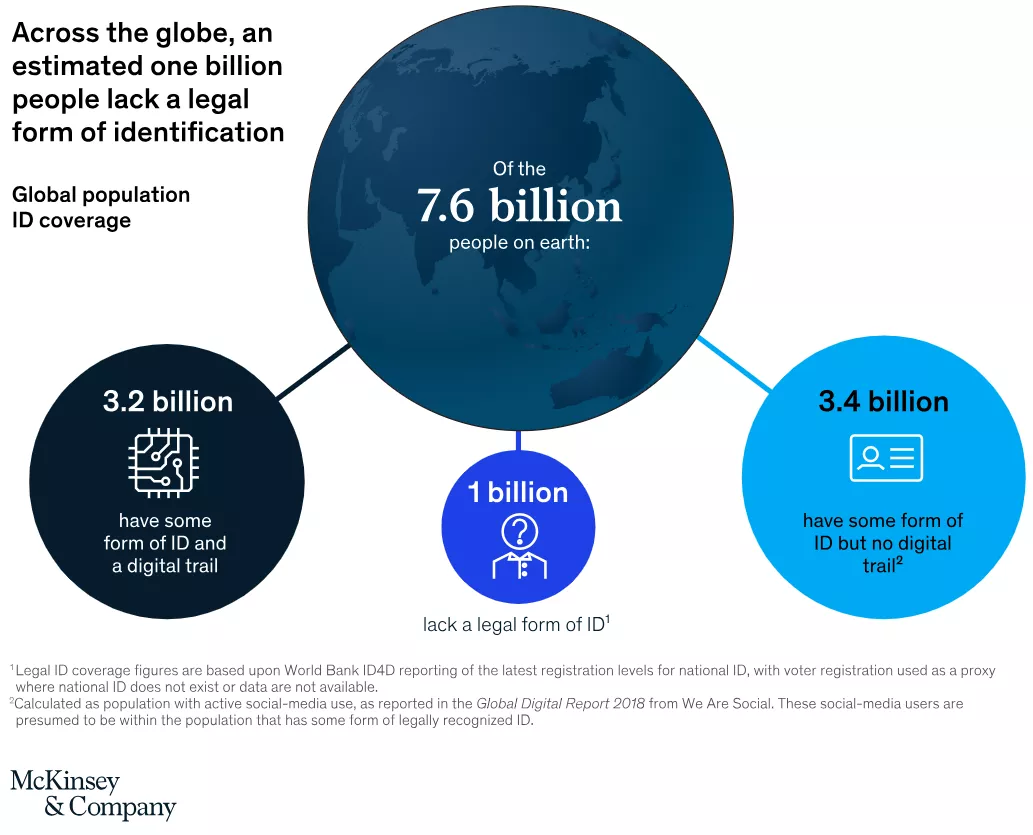

One other important barrier to monetary inclusion is the shortage of formal identification. Roughly 1 billion folks worldwide lack proof of identification, making it tough for them to entry formal monetary providers. Identification verification necessities range throughout international locations and establishments, leading to fragmented and infrequently difficult processes.

This lack of standardization can reinforce present disparities, excluding those that lack entry to assets and alternatives from the advantages of monetary inclusion. The adoption of digital identification can assist handle this difficulty, fostering higher inclusion and enabling higher supply of monetary providers. Digital identification creates a safe, digital illustration of a person’s identification utilizing private data and biometric information and can be utilized to authenticate and authorize people when accessing providers or performing transactions.

In the course of the COVID-19 pandemic, international locations that had already invested in digitizing monetary infrastructure and digital identification methods had been probably the most profitable in distributing assist effectively, with pace, accuracy, and scale. This highlights the potential for digital identification to boost resilience throughout occasions of disaster and uncertainty.

Nonetheless, attitudes in direction of digital ID know-how range considerably throughout the globe. Whereas 70% of shoppers in China and 57% in Brazil assist digital ID, roughly 71% of respondents within the US and Germany desire carrying a bodily ID. These various attitudes underscore the necessity for international leaders to lift consciousness about the advantages of digital ID methods and work in direction of their widespread adoption.

To drive the adoption of digital ID, governments and personal sector stakeholders should collaborate to develop and promote digital ID requirements, fund initiatives to drive innovation, and take legislative and regulatory motion to streamline efforts and keep away from fragmentation. By doing so, they will unlock the total potential of digital identification in selling monetary inclusion and defending the unbanked and underbanked from fraud.

How does a digital ID profit my fraud technique? It has a number of benefits over conventional IDs as a result of it’s:

- A safer and tamper-proof method of identification verification, making it more durable for fraudsters to create faux identities or steal somebody’s identification.

- Enabled for real-time identification verification, permitting you to detect and stop fraudulent actions extra rapidly.

- Significant data for ingestion, aggregation, and enrichment of your different information to raised defend your clients.

How You Can Assist Shield the Underbanked From Fraud

Defending the unbanked and underbanked from fraud is a posh and multifaceted problem that requires the collaboration of governments, monetary establishments, and know-how suppliers. A few of these challenges can solely be overcome by collaboration between completely different establishments, nonetheless there are belongings you as a corporation could be doing at present to arrange yourselves not just for the longer term inflow of the unbanked, but additionally to raised serve your new to banking clients at present.

1. Tailor-made Fraud Prevention Measures

To successfully defend the unbanked and underbanked from fraud, you will need to spend money on superior fraud prevention applied sciences and processes.

This consists of implementing real-time monitoring methods with functionality to:

- develop versatile guidelines

- deploy customized therapy methods

- construct fashions that may adapt to the distinctive behaviors of various demographics

- simulate new methods for various peer teams

- ship bespoke buyer communication

2. Digital Identification Infrastructure

Digital identities will play a important function in selling monetary inclusion and stopping fraud. To maximise their advantages, it is best to concentrate on enhancing your digital identification infrastructure. This entails investing in information ingestion and orchestration capabilities to make sure that related identification information is collected, verified, and built-in into fraud prevention processes seamlessly and on the proper time. By doing so, you may create a extra complete and correct view of your clients’ identities, enabling sooner and simpler service in addition to higher fraud detection and prevention.

3. Monetary Literacy Applications

Empowering the unbanked & underbanked with the data and expertise they should defend themselves from fraud is important. It is best to prioritize monetary literacy initiatives, resembling focused buyer communication campaigns and academic packages that assist people perceive the dangers of fraud and the way to keep away from it. Within the UK, regulatory necessities start to mandate that monetary establishments present tailor-made messaging and schooling to clients prone to falling sufferer to scams. By adopting comparable approaches for the underbanked, you may assist create a extra fraud-resilient buyer base and promote higher belief in formal monetary providers.

Because the world continues to digitize and extra folks acquire entry to formal monetary providers, establishments that prioritize these areas shall be well-positioned to drive higher progress by means of monetary inclusion, whereas defending their clients and their backside line from the evolving menace of fraud.

How FICO Helps Shield You and Your Prospects from Fraud

[ad_2]

Source link