[ad_1]

This week, Minimize the Crap Investing founder Dale Roberts shares monetary headlines and affords context for Canadian traders.

U.S. inflation cools in November

We’ll get to the speed hike choice in a minute, however first let’s take a look at the Tuesday inflation studying that set the desk for serving up a 50-basis level (bps) hike within the U.S.. This transfer south of the border follows the 50-bps charge hike in Canada final week.

Right here’s the current Canadian charge hike historical past:

- 1%: up 50 bps on April 13

- 1.5%: up 50 bps on June 1

- 2.5%: up 100 bps on July 13

- 3.25%: up 75 bps on September 7

- 3.75%: up 50 bps on October 26

- 4.25%: up 50 bps on December 7

The U.S. inflation studying got here in cooler than anticipated. The whole (all objects) shopper value index (CPI) estimate for November was a 7.3% improve. The print got here in at 7.12%—0.18% “cooler” than anticipated. Core inflation was anticipated to come back in at 6.10%, however the quantity ticked down to five.96%—0.14% higher than consensus.

Inventory markets have been initially giddy with the bump and so they charged out of the gates Tuesday on the open of buying and selling. Shares have been up 2.5% in early buying and selling earlier than settling down. The S&P 500 (IVV:NYSE) completed the day forward 0.7%. Canadian and worldwide shares additionally went alongside for the trip.

There was—and maybe is—hope that with inflation not off course, the Fed will quickly be capable to pivot. Today a pivot means much less extreme charge hikes. We would then see a rate-hike hiatus, when the Fed can maintain off to guage the financial impact. There’s a lag impact; it may take a 12 months or extra earlier than the speed hikes work their method by way of the financial system and do their factor. That being to deliver down spending, financial exercise and inflation.

The Fed follows Canada with a 50-bps charge hike

The Fed did downshift to a 50-bps hike, as anticipated. And, that could be a becoming analogy as charge hikes work like a brake on the financial system.

But it surely’s like driving with one foot on the accelerator and one foot on the brake. The driving force, the central braker, er, make that central banker, doesn’t understand how arduous to press on the brakes.

As I advised in August 2022, that is the place physics meets economics.

“Consider inflation as a ball connected to a protracted elastic band within the sky, and it’s falling. The objective is to use simply sufficient strain to extend that charge of descent, with the target being that the ball stops simply wanting crashing into the bottom. After which the ball has to bounce round and settle inside a desired vary. The central bankers’ flight plan is to maintain inflation at a 2% to three% degree.”

Right here’s the 2022 U.S. charge hike historical past:

- 0.5%: up 25 bps on March 17

- 1%: up 50 bps on Might 5

- 1.75%: up 75 bps on June 16

- 2.5%: up 75 bps on July 28

- 3.25%: up 75 bps on September 21

- 4%: up 75 bps on November 3

- 4.50%: up 50 bps on December 15

Powell mentioned in an announcement that getting inflation down towards the Federal Reserve’s 2% objective “will seemingly require a restrictive stance for a while,” after the central financial institution raised its benchmark charge by 50 bps to 4.5%. That’s a step down from the 75-bps charge hikes of the previous 4 conferences.

Nonetheless, the labor market stays “extraordinarily tight” and continues to be out of stability with demand exceeding provide, he added.

Powell additionally insisted the terminal charge goes to be increased than the earlier projection of 4.6%. That terminal-rate projection has now climbed to five% or above. Powell conceded that the Fed will transfer in decrease increments towards the terminal charge, as extra inflation information come by way of. This leaves room for the Fed to revise its estimate. They are going to be “information dependent.”

There could also be two or three extra 0.25% strikes in 2023 to achieve that closing vacation spot of 5% or 5.25%.

Right here’s some perspective from a publish on Looking for Alpha:

“ ‘The rate of interest mantra for 2023 is ‘Larger for Longer’,’ mentioned Bankrate Chief Monetary Analyst Greg McBride. ‘The arduous work remains to be forward. It has been straightforward—and needed—for the Fed to lift rates of interest aggressively in 2022, with rates of interest ranging from zero, unemployment beneath 4%, and inflation at a 40-year excessive. It will get so much more durable to lift charges as soon as the financial system slows, unemployment rises, and inflation stays stubbornly excessive.’ ”

There could also be robust work forward to get inflation to go from 4% all the way down to 2%. I wouldn’t be stunned to see the inflation goal modified sooner or later. Solely time will inform, and inflation remains to be driving the bus.

Listed below are some key time-stamped moments from the Fed’s press convention (all quotes are from Powell, and seem so as of what we predict is significance):

3:07 p.m. (EST): “Altering our inflation goal is one thing we’re not occupied with. We’re not going to think about that beneath any circumstances. We’ll use our instruments to get inflation again to 2%.”

3:05 p.m. (EST): “Our coverage is attending to a fairly good place,” and it’s near “sufficiently restrictive.” The upper charge “narrows the runway” for a comfortable touchdown, however he nonetheless thinks it’s potential.

3:01 p.m. (EST): The November inflation information “clearly do present a welcome discount” within the tempo of inflation. As for core providers inflation, excluding housing, “we do have a option to go there.”

2:47 p.m. (EST): The velocity of charge hikes is now not an important issue, “it’s not so necessary to consider how briskly we go” now, however the place the height charge finally ends up. “Then the query might be how lengthy we keep there,” he mentioned. It’s now about the place we land, and the way lengthy we keep there.

2:42 p.m. (EST): “We predict monetary circumstances have tightened considerably prior to now 12 months,” he mentioned. “Our focus shouldn’t be on short-term strikes, however persistent strikes.” He doesn’t take into account the coverage to be at a sufficiently restrictive coverage stance but.

2:40 p.m. (EST): Whereas the median Federal Open Market Committee (FOMC) charge projection for 2023 has elevated to five.1% from the earlier 4.6% expectation, the projections usually are not a plan to lift charges, Powell mentioned.

2:36 p.m. (EST): The central bankers want extra proof that inflation is headed decrease, he mentioned. As well as, dangers to inflation stay to the upside, he added.

On Wednesday, the U.S. market ended decrease by 0.60%.

Shares took a dive throughout/after Powell presser, with Financials resulting in draw back at this time; Well being Care sole sector up on day … NASDAQ misplaced most amongst broader indexes however weak point was widespread; Russell 1000 Worth continues to have greatest MTD and YTD mixture pic.twitter.com/Zw4OIEoUyG

— Liz Ann Sonders (@LizAnnSonders) December 14, 2022

Shares fell additional on Thursday as jobless claims within the U.S. got here in beneath estimates. The Fed is in search of extra weak point in employment. Additionally, the Financial institution of England additionally boosted its charge by 50 bps.

Shares fell sharply on Thursday (down modestly over the past week) and have declined by virtually 3% over the past month. Markets have digested the current rate-hike strikes and are nonetheless pricing in a comfortable touchdown. However, as I identified final week on this column, they will not be looking far sufficient to the earnings hit being perpetuated by the upper charges and the impact on companies and customers.

The subsequent Fed assembly isn’t till February 1, 2023, and once more on March 22, Might 3 and June 14. By Might/June, we is likely to be executed with any charge hikes and could also be in rate-hike hiatus (watch-and-see) mode.

Whereas the financial consensus is that we are going to enter a recession in 2023, different market members and specialists counsel a recession will not be essential to deliver down inflation.

U.S. Treasury Secretary, Janet Yellen, is of the view that inflation has peaked, or it’s already in decline. She’s additionally hopeful that the labor market will stay wholesome because the central financial institution continues to execute coverage based mostly on the teachings realized from the excessive inflation of the Nineteen Seventies.

Right here’s a quote from Yellen being interviewed on 60 Minutes from Sunday:

“Initially, transport prices have come down. Supply lags, which have been very lengthy—these have shortened. Gasoline costs are method down. I feel we’ll see a considerable discount in inflation within the 12 months forward … if there’s not an unanticipated shock.

“There are all the time dangers of a recession. The financial system stays liable to shocks, however look, we have now a really wholesome banking system. We’ve a really wholesome enterprise and family sector. … We’re at or past full employment. And so it’s not needed for the financial system to develop as quickly because it has been rising to place individuals again to work.”

We don’t know what we are going to get, and solely time will inform in these fascinating occasions.

That is an apt statement on human expectations and framing:

« traders »

pic.twitter.com/KqmgPpNeGd

— KKGB (Carlo Casio) (@INArteCarloDoss) December 14, 2022

If we take a look at the amusing tweet it is likely to be framing the before-the-worst-of-the-inflation storm worry and “the solar will come out tomorrow” optimism.

Inventory tales of the week

There are adjustments to Canadian financial institution scores and laws.

The Workplace of the Superintendent for Monetary Establishments (OSFI) introduced the DSB (home stability buffer) degree might be set at 3% as of Feb. 1, 2023. That primarily signifies that banks must play extra protection and shore up their stability sheets. In a earlier column, I wrote an outline on current Canadian financial institution earnings.

In response to the brand new laws, BMO issued shares, or primarily gave away $3.15 billion price of the corporate. Or, let’s say, you at the moment are sharing the earnings pot with $3.15 billion price of latest traders.

Analysts have gotten way more cautious of the Canadian banking sector.

Elon Musk sells one other huge chunk of Tesla shares with a price of USD$3.6 billion. The decline of Twitter and Tesla (TSLA/NASDAQ) continues.

Microsoft (MSFT/NYSE) buys into the London Inventory Trade, whereas the FTC seems to be to dam Microsoft’s Activision acquisition.

Moderna (MRNA/NYSE) and Merck (MRK/NYSE) combat most cancers with mRNA know-how. In fact, that’s the know-how used to develop the most-used and most profitable COVID vaccines. Moderna shares popped 22%.

And a few Canadian craft beer fans is likely to be crying of their beer this week.

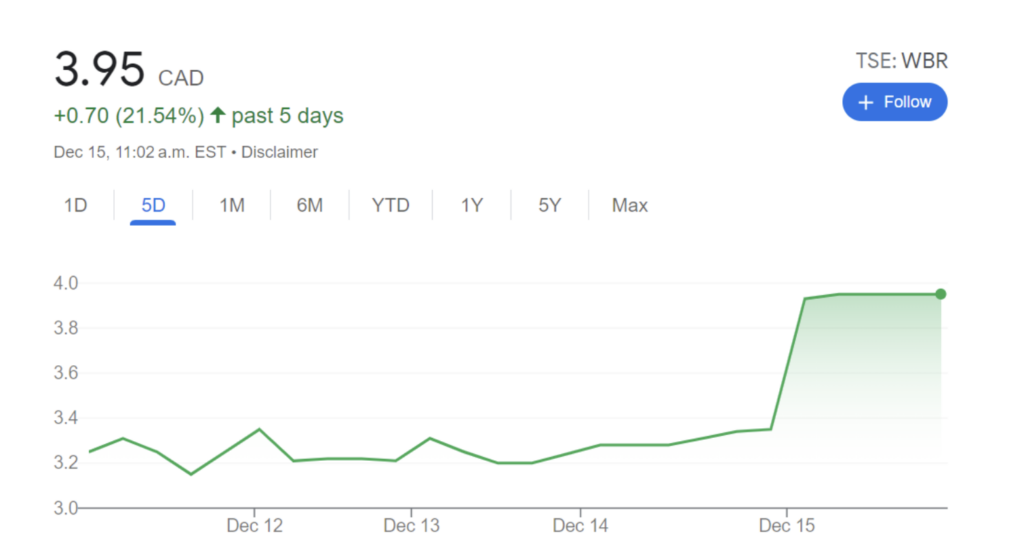

BREAKING NEWS: @WaterlooBrewing to be acquired by @CarlsbergGroup for $144 million. Look ahead to full particulars to be posted on the CBN web site tomorrow morning. pic.twitter.com/y2R5eckk61

— Canadian Beer Information (@cdnbeernews) December 15, 2022

The OG craft beer in Canada has been acquired by one of many large boys, Carlsberg. The inventory has had a tough go. The corporate shouldn’t be very worthwhile. That mentioned, the inventory (WBR/TSX) was up greater than 8% over the past 5 buying and selling periods earlier than the announcement. The inventory ripped on Thursday, up virtually 18%.

Hmmm?

Ring, ring.

Hiya.

Hiya, Ontario Securities Fee, have you ever seen that weekly inventory chart?

?

How it’s possible you’ll place your portfolio for 2023

I did a ton of analysis and listened to many market specialists and portfolio managers (that I’d give the time of day to) to pen this publish on Looking for Alpha: How one can put together your portfolio for 2023 (if the comfortable touchdown narrative is correct). In fact, this isn’t recommendation, merely my observations and ideas, however I’ll provide the gist of the potential positioning. What labored in 2022 (and these are the property that I’ve lengthy advised) would possibly proceed to work in 2023.

You might purchase good firms that make some huge cash (in defensive sectors). Financial moats could be greater than helpful in occasions of financial stress. You might need to add in vitality shares and ETFs. It is also smart for retirees and close to retirees to carry some bonds and money as nicely.

From that publish …

“Primarily, the funding theme of what has labored in 2022 would possibly proceed in 2023. Good firms with low or modest debt and beneficiant quantities of free money circulation. And sure, getting paid (dividends) might be necessary as nicely.”

High quality + an inflation hedge.

Dale Roberts is a proponent of low-fee investing, and he blogs at cutthecrapinvesting.com. Discover him on Twitter @67Dodge for market updates and commentary, daily.

The publish Making sense of the markets this week: December 18, 2022 appeared first on MoneySense.

[ad_2]

Source link