[ad_1]

Revealed on January twenty seventh, 2023 by Quinn Mohammed

The Dividend Kings are a selective group of shares which have elevated their dividends for not less than 50 years in a row. We imagine the Dividend Kings are among the many highest-quality dividend progress shares to purchase and maintain for the long run.

With this in thoughts, we created a full record of all of the Dividend Kings. You may obtain the total record, together with necessary monetary metrics reminiscent of dividend yields and price-to-earnings ratios, by clicking the hyperlink beneath:

The latest member to hitch this record is S&P World (SPGI). S&P World, like all Dividend Kings, has a really spectacular dividend observe document. It has paid a dividend yearly since 1937 and has raised its dividend for 50 years in a row. The corporate most lately raised its dividend by 6.4% on January 25th, 2023.

This text will focus on the corporate’s enterprise overview, progress prospects, aggressive benefits, and anticipated returns.

Enterprise Overview

S&P World is a worldwide supplier of monetary providers and enterprise data. The corporate traces its roots again to 1917 when McGraw Publishing Firm and the Hill Publishing Firm got here collectively. The corporate was first named McGraw Hill Monetary. In 1957, McGraw Hill launched the S&P 500, probably the most widely-recognized index of all large-cap U.S. shares.

S&P World affords monetary providers to the worldwide capital and commodity markets, together with credit score rankings, benchmarks, analytics, and different information to commodity market individuals, capital markets, and automotive markets. The corporate’s 5 divisions are: Scores, Market Intelligence, Commodity Insights, Mobility, and S&P Dow Jones Indices.

S&P World has a extremely worthwhile enterprise mannequin. It’s the business chief in credit score rankings and inventory market indexes, which permits it to generate high-profit margins and progress alternatives.

Supply: Investor Presentation

Notably, on February twenty eighth, 2022, S&P World merged with HIS Markit. The merger permits the corporate to supply a stronger, extra numerous product portfolio on an excellent bigger scale. The corporate at the moment has a market capitalization of almost $120 billion and generates $12 billion of annual income.

On October twenty seventh, 2022, S&P World reported third-quarter outcomes. The corporate posted adjusted earnings-per-share of $2.93, which was 13 cents forward of expectations however 4% decrease year-over-year. Then again, income grew by 37% in comparison with the prior 12 months interval however was $60 million wanting estimates. Adjusted working revenue decreased by 200 foundation factors to 46.0% of income in comparison with Q3 2021.

Our 2022 adjusted earnings-per-share estimate stands at $11.10.

Progress Prospects

S&P World has a powerful observe document. The corporate has grown its earnings-per-share yearly for over a decade. Nonetheless, this streak could finish as soon as fourth quarter 2022 outcomes are reported, as we’re forecasting S&P World to declare it has generated $11.10 in EPS for 2022, which can also be in line with the analysts’ consensus. Nonetheless, S&P World has grown its earnings-per-share at a staggering price of 19.3% over the past eight years.

The corporate’s previous progress has been the results of a collection of secular traits, that are, in truth, nonetheless current at the moment. On condition that company debt has been very fashionable within the final decade, buoyed by low international rates of interest, enterprise rankings have been necessary. With the current enhance in rates of interest, buyers are prone to preserve an in depth eye on these rankings. Nonetheless, on account of elevated charges, fewer debt issuances come up, negatively impacting S&P World’s outcomes.

Moreover, the growing demand for monetary evaluation and ETFs ought to assist in rising the corporate’s merchandise and earnings.

Share buybacks can even assist in progress on a per-share foundation. As of the top of the third quarter of 2022, S&P World had repurchased $11 billion price of shares on its $12 billion accelerated share repurchase program. Over the past eight years, S&P World has diminished its excellent shares by roughly 1.5% yearly.

The corporate has additionally been very lively in acquisitions and divestments to reinforce its enterprise. First, the corporate accomplished a big merger with HIS Market in February 2022.

Then on December 6th, 2022, the corporate acquired the Shades of Inexperienced enterprise from the Middle for Worldwide Local weather Analysis. This acquisition will develop S&P World Scores’ second-party opinions (SPOs) providing.

And on January 17th, 2023, S&P World agreed to promote its Engineering Options Enterprise to KKR for $975 million in money, which might equal roughly $750 million after tax and be utilized to repurchase its personal shares.

Supply: Investor Presentation

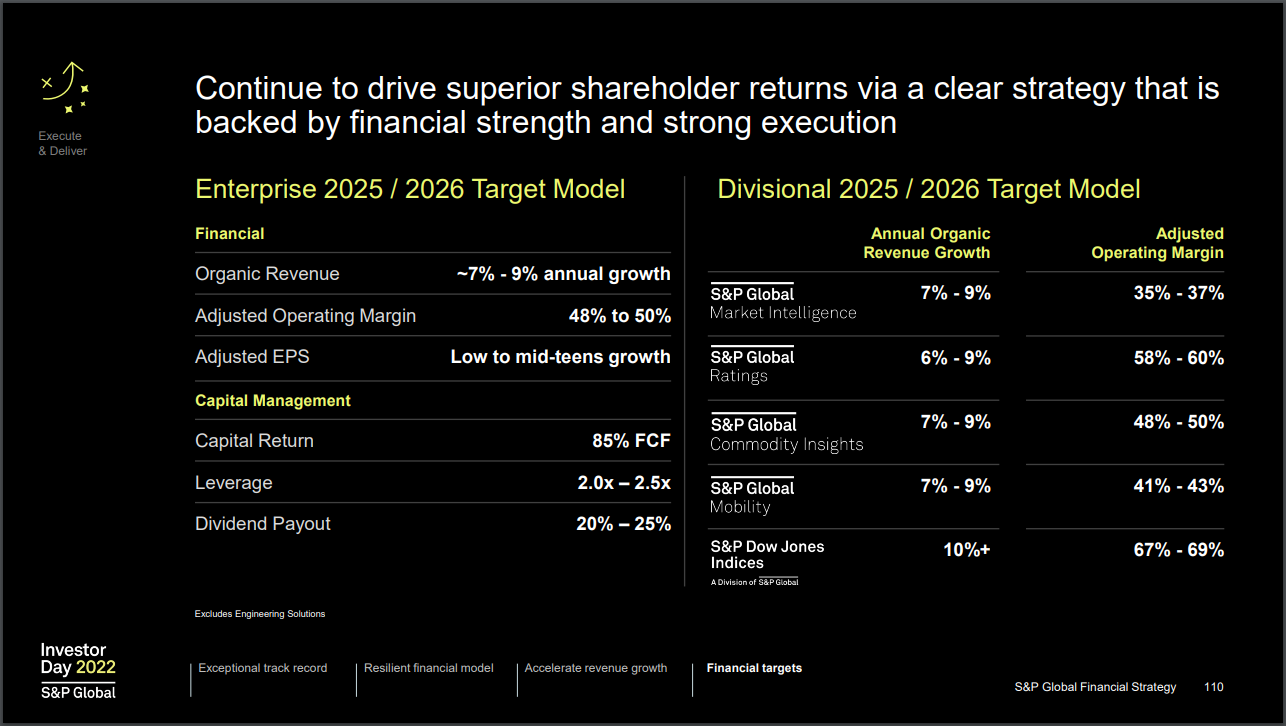

Management lately said that they count on to realize 7% to 9% natural annual income progress by 2025 – 2026. The corporate additionally expects to realize an adjusted working margin between 48% to 50% and low to mid-teens progress in annual adjusted diluted EPS.

Whereas S&P World is anticipated to take a lower in earnings-per-share for 2022, the corporate appears solidly on foot to return to progress instantly within the following 12 months and past, as its secular tailwinds are intact.

We forecast that S&P World can develop its earnings-per-share by 10% over the following 5 years.

Aggressive Benefits & Recession Efficiency

S&P World advantages from a number of aggressive benefits. The corporate operates within the extremely concentrated monetary rankings business. It’s one in every of solely three main credit standing businesses within the U.S. that management over 90% of world monetary debt rankings. The opposite two are Moody’s (MCO) and Fitch Scores.

The corporate possesses a powerful moat as there are large boundaries to entry in its business. New entrants would discover it tough, if not not possible, to garner the mandatory belief from the monetary business and authorities to grow to be an accepted score company.

S&P World’s aggressive benefit and moat enabled it to stay worthwhile even through the Nice Recession when earnings decreased by -21% to $2.33. Whereas many corporations had been on the point of collapse, S&P World was removed from reporting losses.

Through the COVID-19 pandemic disaster, S&P World’s outcomes held up tremendously, and the corporate achieved new document outcomes 12 months after 12 months.

Valuation & Anticipated Returns

Primarily based on our estimate for 2022 earnings-per-share of $11.10 and a present share worth of simply above $366, shares of S&P World are buying and selling at a P/E ratio of 33.0.

This valuation is wealthy for S&P World, which has traded for a mean P/E ratio of about 23 over the past 5 years. Our truthful worth estimate for the corporate is 26 instances earnings, contemplating the corporate has produced sturdy outcomes lately.

Shares look like overvalued, buying and selling nicely forward of our estimates. If shares had been to retreat to a price-to-earnings ratio of 26.0 over the following 5 years, buyers would see a discount in annual returns of 4.6%.

The inventory additionally has a present dividend yield of 1.0%. The dividend is extremely safe, with a payout ratio of solely 31%. Nonetheless, a 1.0% yield isn’t significantly engaging for earnings buyers.

Mixed with the estimated 10% earnings-per-share progress price, S&P World is forecasted to generate complete returns of 6.0% per 12 months by 2028. Given this price of return, S&P World shares aren’t very compelling right now.

Closing Ideas

S&P World has skilled large progress within the final decade. Its aggressive benefits and robust place in its score business oligopoly will proceed to guard the corporate’s draw back. Mixed with its sturdy share buyback program and strategic mergers & acquisitions exercise, the corporate has a shiny future nonetheless.

The corporate has now achieved Dividend King standing following its 50th consecutive annual dividend enhance. Nonetheless, the low dividend yield of 1.0% isn’t so interesting. One thing to remember is that the ahead dividend now’s 3 times the dividend paid in 2013.

For the time being, although, shares are buying and selling for a wealthy valuation, which gravely reduces the attractiveness of the inventory.

Moreover, the next Certain Dividend databases comprise probably the most dependable dividend growers in our funding universe:

If you happen to’re searching for shares with distinctive dividend traits, contemplate the next Certain Dividend databases:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link