[ad_1]

Up to date on February 2nd, 2023 by Nathan Parsh

PPG Industries (PPG) is without doubt one of the largest paint firms on the earth. It is usually one of the dependable dividend shares out there–PPG has paid dividends each quarter since 1899.

Furthermore, the corporate has elevated its dividend every year for the final 51 years, which qualifies it to be a member of the unique Dividend Aristocrats checklist.

This can be a group of 68 shares within the S&P 500 Index with at the least 25 consecutive years of dividend development.

We contemplate the Dividend Aristocrats to be among the many elite dividend-paying firms. With this in thoughts, we created a full checklist of all 68Dividend Aristocrats.

You may obtain the whole Dividend Aristocrats checklist, with essential monetary metrics like dividend yields and P/E ratios, by clicking on the hyperlink under:

The inventory can be on the unique checklist of Dividend Kings.

PPG’s outstanding dividend consistency offers it broad enchantment to the extra conservative members of the dividend development investing group.

Certainly, the corporate has a really protected dividend fee with room for regular dividend will increase every year, due to its sturdy enterprise mannequin. That is nonetheless very a lot the case right now.

This text will analyze PPG’s funding prospects intimately and decide whether or not the corporate deserves a purchase advice at present costs.

Enterprise Overview

PPG Industries was initially based in 1883 as a producer and distributor of glass. PPG stands for Pittsburgh Plate Glass, which is a reference to the corporate’s authentic operations.

Over time, PPG has made outstanding strides in turning into an trade chief within the paints and coatings trade.

With annual revenues of about $18 billion, PPG’s solely rivals of comparable measurement are fellow Dividend Aristocrat Sherwin-Williams (SHW), in addition to Dutch paint firm Akzo Nobel (AKZOY).

PPG Industries has grown to such a powerful measurement due to its worldwide working presence and deal with know-how and innovation.

Its analysis and improvement focus is a key differentiator between PPG and different paint & coatings firms. Due to its heavy R&D investments, PPG has grown to be a market chief right now.

As well as, PPG has a protracted historical past of accretive acquisitions which have helped it develop over time. PPG has been very busy in simply the previous couple of years, securing acquisitions that can add almost $2 billion in income to its prime line, and also will bolster its worldwide presence. It has a really lengthy historical past of profitable acquisitions, which means it may develop not solely organically, but in addition by means of buying scale and market share.

PPG reported fourth-quarter and full yr outcomes on January nineteenth, 2023.

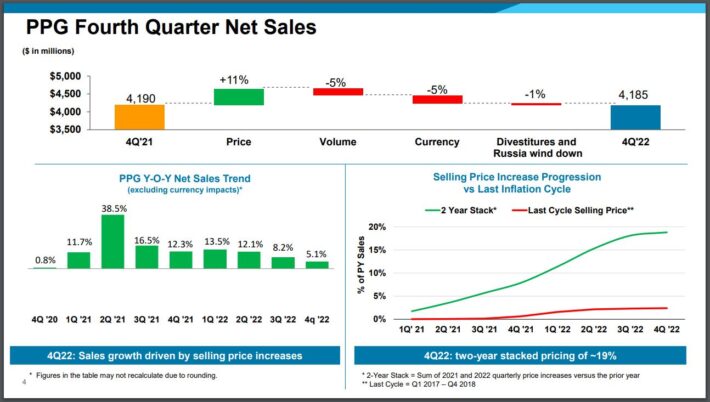

Supply: Investor presentation, web page 4

Income was flat for the quarter, however up 5.4% to $17.7 billion for 2022. Adjusted earnings-per-share fell to $1.22 from $1.26 for the quarter. Full yr earnings-per-share of $6.05 in contrast unfavorably to $6.77 in 2021.

PPG has developed unbelievable model loyalty over time, which has helped it to endure the rising enter value going through the corporate in recent times. PPG has largely offset these prices by elevating costs on its merchandise with out seeing a major drawdown in quantity. As you’ll be able to see, pricing added 11% to quarterly outcomes with quantity down a mid-single-digit determine.

Our preliminary estimate for 2023 is $6.99 in earnings-per-share.

Development Prospects

By and huge, an organization’s skill to extend revenues and income is a perform of its capital allocation.

PPG has spent billions of {dollars} in recent times shopping for its subsequent technology of development. It tries to keep up a considerably balanced capital allocation technique, however it is usually not afraid to spend huge on acquisitions when alternatives current themselves.

PPG has spent way more of its deployed money on share repurchases than its rivals, which has been a significant supply of earnings-per-share development over time.

It is usually probably that mergers and acquisitions will likely be a continued focus for PPG shifting ahead, as the corporate strikes again in the direction of its core competency of portfolio optimization.

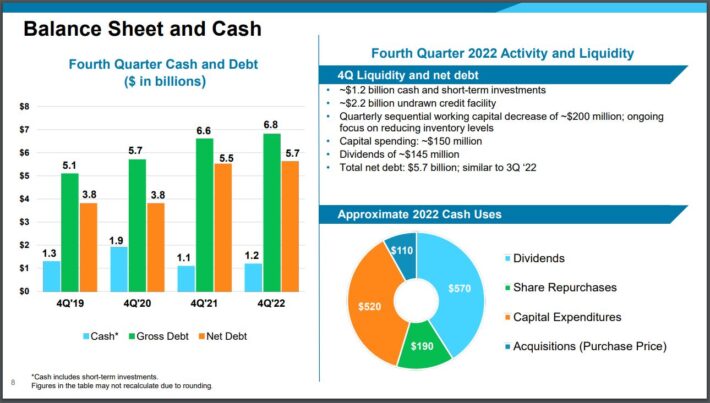

Acquisitions have been a key development driver for PPG for a few years. That development has come at a value, particularly a rise within the firm’s debt.

Supply: Investor Presentation, web page 8

PPG is now nearly solely a coatings enterprise. The transformation in recent times away from legacy companies like glass and chemical compounds has left the corporate with a powerful portfolio of coatings merchandise that collectively generate almost $18 billion in annual income.

PPG acknowledged years in the past that its future development can be in coatings, and has positioned itself accordingly.

Its monitor document means that its underlying enterprise is prone to proceed rising at a passable charge for the foreseeable future. Up to now decade, the corporate has grown its earnings-per-share at a median charge of just below 6%.

PPG has been an elite development inventory for a very long time. This development has not been linear, as there have been ups and downs from yr to yr, however over time, PPG has delivered spectacular development.

Given its very sturdy fundamentals and its deal with coatings, we imagine buyers can fairly count on 8% adjusted earnings-per-share development from PPG Industries by means of full financial cycles.

Nevertheless, PPG’s efficiency is prone to undergo in periods of financial recession. The excellent news is that we’d probably see such an occasion as a shopping for alternative for this high-quality enterprise.

Aggressive Benefits & Recession Efficiency

PPG enjoys quite a lot of aggressive benefits. It operates within the paints & coatings trade, which is economically enticing for a number of causes. First, these merchandise have high-profit margins for producers.

Additionally they have low capital funding, which leads to important money circulation. PPG has put this important money circulation to make use of over time, as mentioned above.

Given all this, it is smart that there are simply two coatings firms (Sherwin-Williams and PPG Industries) on the Dividend Aristocrats checklist.

With that mentioned, the paint and coatings trade isn’t very recession-resistant as a result of it relies on wholesome housing and development markets. This influence might be seen in PPG’s efficiency throughout the 2007-2009 monetary disaster:

- 2007 adjusted earnings-per-share: $2.52

- 2008 adjusted earnings-per-share: $1.63 (35% decline)

- 2009 adjusted earnings-per-share: $1.02 (37% decline)

- 2010 adjusted earnings-per-share: $2.32 (127% enhance)

PPG’s adjusted earnings-per-share fell by greater than 50% over the past main recession and took two years to recuperate.

As PPG’s 2020 outcomes confirmed, the decline in new development is the dominant issue for PPG throughout a recession. The 2020 recession was no totally different, as PPG confronted manufacturing facility shutdowns and severely decreased demand from shoppers, though that proved to be transitory.

Whereas the long-term prospects of this Dividend Aristocrat stay vibrant, buyers ought to be keen to just accept volatility in a recession.

If something, a recession and corresponding decline in PPG’s share worth would enable buyers to buy extra shares of this inventory at a way more enticing worth.

Valuation & Anticipated Complete Returns

We’re forecasting earnings-per-share of $6.99 for the fiscal yr of 2023, placing the price-to-earnings ratio at 19.2. That is simply above our truthful worth estimate of 19 instances earnings, which means PPG is barely overvalued right now.

As such, we count on a modest 0.2% headwind to complete returns from valuation within the coming years.

In complete, we challenge that PPG will return 9.5% yearly by means of 2028, stemming from 8% earnings development and the beginning yield of 1.9%, partially offset by a 0.2% headwind from a number of contraction. Given this, we proceed to charge PPG a maintain, although we’d discover the identify extra enticing on a slight pullback.

Ultimate Ideas

PPG Industries has most of the traits of a really high-quality enterprise. It has a confirmed enterprise mannequin and has generated sturdy development over the previous a number of years.

It additionally has a major worldwide presence and a number of catalysts for future development. Lastly, it has elevated its dividend for 51 years.

Nevertheless, the inventory is barely overvalued.

PPG’s dividend outlook is exemplary and we see many extra years of dividend will increase on the horizon. That mentioned, we propose ready for a pullback earlier than shopping for.

If you’re thinking about discovering high-quality dividend development shares appropriate for long-term funding, the next Certain Dividend databases will likely be helpful:

The main home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link