[ad_1]

Printed on April 14th, 2023 by Jonathan Weber

3M Firm (MMM) has elevated its dividend for greater than 60 years in a row, which makes for an distinctive dividend progress monitor report. As we speak, 3M’s dividend yield is at a stage that’s approach larger than the historic norm, at round 5.7%.

The corporate’s shares have underperformed the broad market over the past yr and over a multi-year timeframe, primarily because of headwinds from lawsuits that 3M continues to battle.

3M Firm is likely one of the high-yield shares in our database.

Additionally it is a part of our ‘Excessive Dividend 50’ sequence, the place we cowl the 50 highest yielding shares within the Positive Evaluation Analysis Database.

We now have created a spreadsheet of shares (intently associated REITs and MLPs, and so on.) with 5% or extra dividend yields.

You possibly can obtain your free full record of all securities with 5%+ yields (together with vital monetary metrics equivalent to dividend yield and payout ratio) by clicking on the hyperlink under:

On this article, we’ll analyze the outlook for 3M Firm.

Enterprise Overview

3M Firm is a diversified industrial firm that sells a really wide selection of merchandise, from adhesives to private safety gear. Its product portfolio consists of greater than 60,000 totally different merchandise, and the corporate is lively in additional than 200 international locations across the globe.

This diversification throughout totally different product traces and totally different geographic markets has allowed 3M Firm to be extra resilient in comparison with many different industrial corporations. 3M has greater than 90,000 workers, was based greater than 100 years in the past, in 1902, and is headquartered in St. Paul, Minnesota.

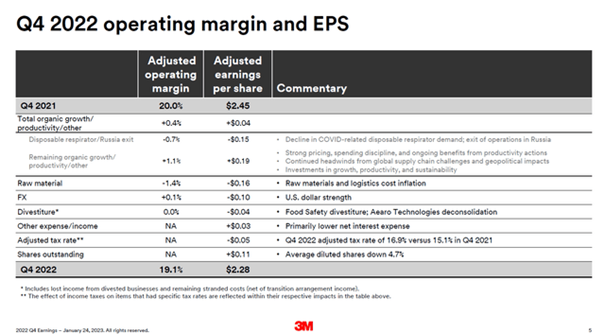

The corporate reported its most up-to-date quarterly outcomes on January 24. The corporate’s gross sales got here in at $8.1 billion for the quarter, which was down 6% in comparison with the earlier yr’s quarter, which was just about according to the Wall Road consensus estimate.

3M Firm’s earnings-per-share for the interval got here in at $2.28, which was barely lower than anticipated, and which was down from the earlier yr’s quarter. A large number of headwinds for financial progress and industrial exercise, equivalent to excessive inflation, rising rates of interest, and an power disaster in Europe, are answerable for the destructive enterprise progress that 3M has skilled through the interval.

Supply: Investor Presentation

Greater uncooked materials costs have been the principle contributor to the margin decline 3M skilled through the interval, whereas unfavorable forex charge actions additionally had a destructive influence. The US Greenback strengthened versus most currencies in 2022, which made 3M’s ex-US income value much less as soon as denominated in US {Dollars}.

Progress Prospects

3M Firm has delivered stable earnings-per-share and enterprise progress over the past decade. Between 2013 and 2022, its earnings-per-share rose from $6.72 to $10.10, which pencils out to an annual progress charge of 5%. That’s not spectacular, however very stable for a dependable and established blue chip firm equivalent to 3M Firm.

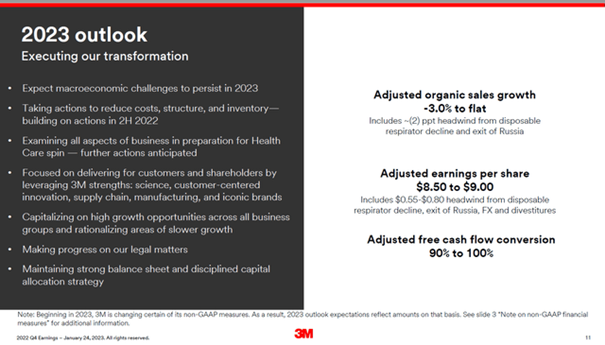

For the present yr, 3M expects an earnings-per-share decline, primarily because of a weakening macro-economic setting and a possible recession:

Supply: Investor Presentation

Up to now, earnings-per-share progress rested on a number of contributing elements. The corporate was in a position to develop its gross sales volumes over time, by getting into new markets and by introducing new merchandise. Worth will increase additionally contributed to income progress, whereas 3M Firm has additionally had a historical past of shopping for again its personal shares.

These buybacks have decreased 3M’s share rely over time, by round 20% over the past decade. A declining share rely interprets into a better portion of the corporate’s total web revenue per every remaining share, thus buybacks add to 3M’s earnings-per-share progress in the long term.

Normally, the identical progress drivers ought to stay intact going ahead, which is why we imagine that 3M Firm will be capable of develop its earnings-per-share at a mid-single digit tempo sooner or later, too. That being mentioned, the lawsuits and their unknown influence of them add some uncertainty about 3M’s future profitability.

Aggressive Benefits

3M’s aggressive benefits are principally centered round its product portfolio, patent portfolio, and profitable analysis and growth efforts.

The corporate’s product portfolio may be very vast and diversified, which signifies that 3M will not be very susceptible to weaknesses in single finish markets, as that may be balanced out by the outcomes from different product classes.

3M invests a mid-single digit proportion of its annual gross sales into R&D, which has traditionally paid off. Round 30% of 3M’s gross sales have been made with merchandise that didn’t exist 5 years in the past, which showcases 3M’s success in growing and commercializing new merchandise. There is no such thing as a assure that this can proceed sooner or later, however the R&D tradition appears to be sturdy at 3M, which must be advantageous.

3M has not been invulnerable throughout recessions, however it has proven stable resilience, particularly in comparison with many different industrial corporations. The corporate remained worthwhile through the Nice Recession and through the pandemic, when earnings-per-share declined by simply 4% within the 2019-2020 timeframe, earlier than hitting a brand new report excessive in 2021. The above-average resilience throughout opposed financial environments must be maintained sooner or later, too.

Dividend Evaluation

3M Firm has an excellent dividend progress monitor report, having raised its dividend for 64 years in a row. Over the past decade, dividend progress averaged 10% per yr, which is fairly sturdy.

As a consequence of the truth that 3M’s dividend progress charge was roughly twice as excessive as its earnings-per-share progress charge over the past decade, 3M’s dividend payout ratio has risen significantly in that timeframe. Primarily based on present earnings-per-share estimates, the 2023 dividend payout ratio is 68%, which is on the higher finish of the historic vary.

This may doubtless not trigger a dividend minimize, because the dividend continues to be coated simply, however 3M will doubtless not ship an analogous dividend progress charge in comparison with the previous. As an alternative, it appears doubtless that 3M will attempt to convey down its dividend payout ratio over time, which is why dividend progress within the coming years could possibly be subdued. Due to a excessive dividend yield of 5.7%, that won’t be a catastrophe, nevertheless.

Closing Ideas

3M Firm has been a nasty performer on a share value and whole return foundation over the past yr and the final 5 years. This was principally the results of a number of compression, nevertheless, and never the results of declining earnings or dividends.

Lawsuits associated to so-called “endlessly chemical compounds” and (presumably) defective listening to safety tools have launched uncertainties, which is why 3M has seen its valuation compress.

As we speak, 3M Firm trades at a transparent low cost in comparison with how the corporate was valued previously, which gives for some a number of growth potential going ahead.

We imagine that the corporate may ship double-digit annual returns over the subsequent 5 years, due to a mix of a excessive dividend yield, some earnings progress potential, and a few a number of growth potential.

In case you are inquisitive about discovering high-quality dividend progress shares and/or different high-yield securities and revenue securities, the next Positive Dividend sources shall be helpful:

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link