[ad_1]

Up to date on September eighth, 2023 by Nikolaos Sismanis

H.B. Fuller (FUL) has elevated its dividend for 54 years in a row. That places the corporate among the many elite Dividend Kings, a small group of shares which have elevated their payouts for no less than 50 consecutive years. You may see the entire listing of all 50 Dividend Kings right here.

We’ve created a full listing of all 50 Dividend Kings, together with vital monetary metrics equivalent to price-to-earnings ratios and dividend yields. You may entry the spreadsheet by clicking on the hyperlink under:

H.B. Fuller has remained a comparatively small firm, buying and selling at a market capitalization of simply $3.8 billion. Nevertheless, a small market cap just isn’t a detrimental characteristic when investing; fairly the opposite.

Regardless of its small dimension, H.B. Fuller has promising development prospects due to the expansion potential of the area of interest market wherein it operates. The inventory gives a 1.1% dividend yield, which is decrease than the yield of the S&P 500.

Nevertheless, there’s ample room for a lot of future dividend raises due to a low payout ratio and the corporate’s development prospects.

Enterprise Overview

H.B. Fuller is a world market chief in adhesives, sealants, and different specialty chemical merchandise. It has 69 manufacturing services and 38 know-how facilities and sells its merchandise in 125 nations.

Adhesives is an exceptionally engaging area of interest market. Adhesives are important supplies in quite a few functions, however they comprise only a small expense for H.B. Fuller’s prospects. Adhesives make up lower than 1% of the price of items for many prospects.

As well as, every adhesive has distinctive chemistry, with most product formulations together with 3-10 chemical substances. Additionally it is uneconomical for patrons to change to a different provider. General, H.B. Fuller’s prospects have to make use of its important merchandise with out paying a lot consideration to their value, which is minor in comparison with their different prices.

Supply: Investor Presentation

H.B. Fuller has carried out properly over the previous few years, with the corporate rebounding very strongly from the coronavirus disaster in 2020. The corporate earned $3.47 in adjusted earnings-per-share in 2021, which was an enchancment over the corporate’s outcomes even previous to the pandemic.

In 2022, adjusted earnings-per-share grew additional to $4.00, a brand new all-time excessive for H.B. Fuller. This yr, we anticipate the corporate’s profitability to be equally sturdy.

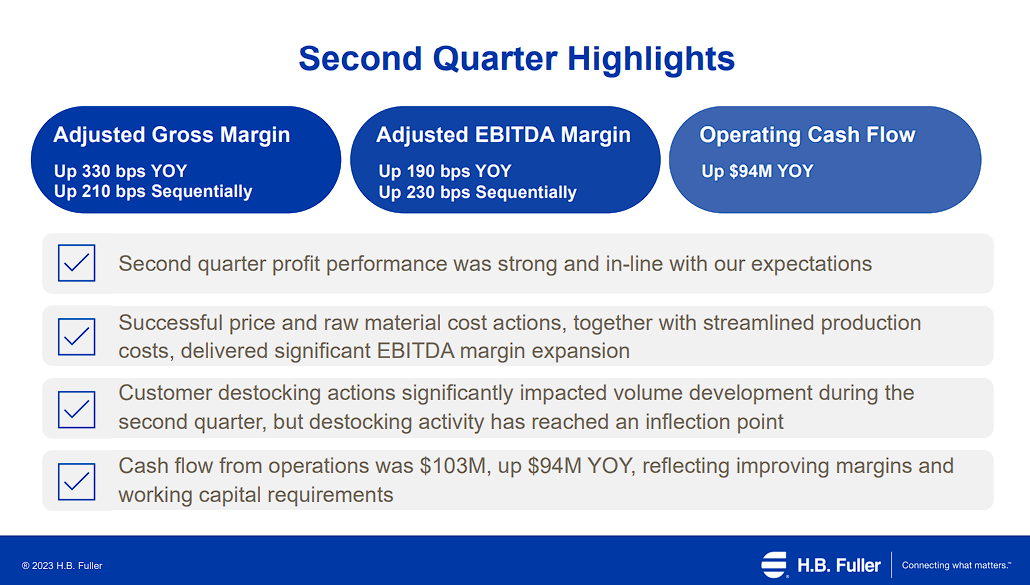

The corporate’s well being and hygiene adhesives benefited significantly from the pandemic due to a steep enhance within the demand for all these merchandise in addition to packaging materials and labeling. Nevertheless, after eight consecutive quarters of strong development, Q2-2023 marked the second consecutive decline in gross sales.

Particularly, H.B. Fuller’s income and natural income fell by 9.6% and eight.3% year-over-year, respectively. This was as a consequence of worth hikes of 5.9% being greater than offset by a 14.2% decline in quantity decline. Decrease volumes can, in flip, be attributed to weaker demand amid de-stocking actions of its prospects and poor industrial demand.

The corporate’s top-line development for the quarter was additionally affected by international foreign money translation, which decreased internet income development by 3.4%, and acquisitions, which elevated internet income development by 2.1%.

Relating to its profitability, the corporate benefited from a lift in its adjusted gross margins, which expanded by 330 foundation factors to 29%. Nevertheless, greater curiosity bills and a powerful greenback led to earnings-per-share declining by 16%, from $1.11 to $0.93 in comparison with final yr.

As a result of a slowing world economic system, H.B. Fuller lowered its steering for earnings-per-share this yr from $4.10-$4.50 to $3.80-$4.20. On the midpoint, the corporate’s steering implies that earnings-per-share will stay eventually yr’s ranges.

Development Prospects

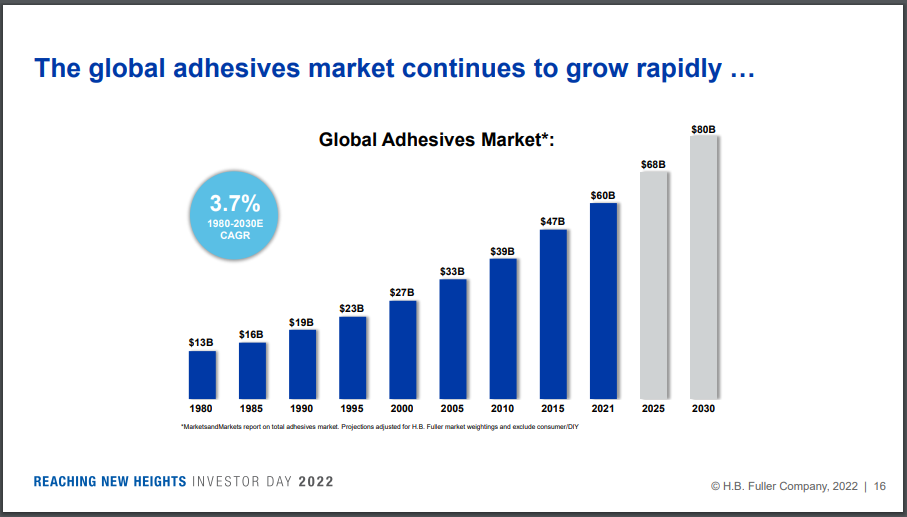

The adhesives market has exhibited a 3.8% common annual development price during the last 41 years. It has turn into a $60+ billion market that’s extremely fragmented, with the highest firms producing lower than 35% of the entire gross sales.

Supply: Investor Presentation

Due to the excessive fragmentation of this market, there’s a vital development potential for H.B. Fuller, which has persistently been the second-largest participant out there behind Henkel.

Furthermore, H.B. Fuller enjoys economies of scale that its smaller opponents can’t match, whereas the latter additionally lacks the worldwide attain to compete straight with H.B. Fuller. In consequence, H.B. Fuller will seemingly develop by gaining market share from its small opponents over time.

H.B. Fuller can also be more likely to continue to grow through vital acquisitions. In 2017, it acquired Royal Adhesives & Sealants for $1.6 billion. As the worth of that acquisition is two-thirds of the present market capitalization of H.B. Fuller, it’s evident that the merger, the most important within the firm’s historical past, was important. The acquisition enhanced the product vary of H.B. Fuller to extra specialised adhesives and boosted its annual gross sales by about $735 million (32%).

For the reason that acquisition, H.B. Fuller has been lowering its debt load at a quick tempo. When that course of is full, H.B. Fuller will shift its focus once more to potential takeover targets.

H.B. Fuller has grown its earnings per share at a mean annual price of 8.7% from 2013 to 2022. Given the promising development prospects of H.B. Fuller, we anticipate the corporate to develop its earnings per share at an 8.0% common annual price over the subsequent 5 years.

Aggressive Benefits & Recession Efficiency

H.B. Fuller’s prospects manufacture a variety of merchandise. Consequently, the efficiency of H.B. Fuller significantly relies on the prevailing financial circumstances, and thus, the corporate is weak to recessions. Within the Nice Recession, its earnings per share plunged 79%, from $1.68 in 2007 to $0.36 in 2008, and the inventory misplaced two-thirds of its market capitalization in lower than six months.

Nonetheless, the big selection of functions of its adhesives gives some diversification. For instance, throughout the pandemic, sturdy development in demand for well being and hygiene merchandise had principally offset the lower within the demand for adhesives in different classes.

Yr-to-date, as of Q2 2023, the corporate’s revenues have taken successful as a consequence of file demand in earlier quarters easing. Nevertheless, gross income have grown, and regardless of greater curiosity bills, internet revenue stays sturdy.

Furthermore, H.B. Fuller is the #1 or #2 participant in most of its markets, and thus, it could possibly endure a downturn extra readily than its small competitor, due to its economies of scale. Additionally it is value noting that its prime 10 prospects comprise a comparatively small quantity of its income, and thus, the corporate has restricted danger from any particular buyer.

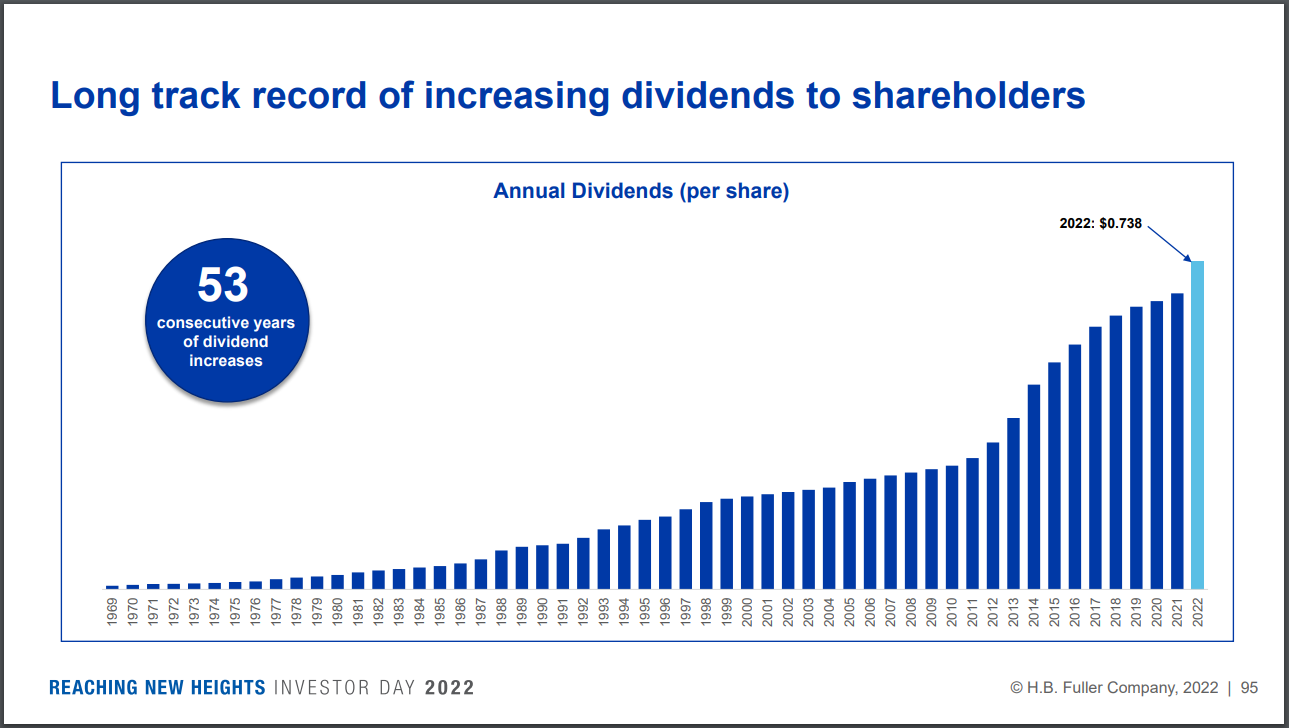

Lastly, it’s spectacular that an industrial producer intently tied to the underlying financial development has raised its dividend for 54 consecutive years. It is a testomony to this area of interest market’s sturdy development and the corporate’s wonderful enterprise execution. H.B. Fuller has achieved this distinctive dividend development file partly due to its low payout ratio.

Supply: Investor Presentation

The corporate has at all times focused a payout ratio of round 25% and thus has been in a position to hold elevating its dividend even in years when its earnings have briefly plunged. As a result of low payout ratio, the dividend is protected, however the resultant 1.1% dividend yield is lackluster.

Valuation & Anticipated Returns

H.B. Fuller is at present buying and selling at 17.8 instances its anticipated earnings per share of $4.00 this yr. Whereas the historic earnings a number of of the inventory is 16.8, we consider {that a} truthful price-to-earnings ratio is 15.0 because of the cyclical nature of the inventory. If the inventory reaches our truthful valuation degree over the subsequent 5 years, it’s going to endure a 3.3% annualized headwind in its returns.

Given 8% anticipated earnings-per-share development, the 1.1% dividend, and a -3.3% impression of an increasing price-to-earnings a number of, we anticipate H.B. Fuller to supply a 5.5% common annual return over the subsequent 5 years. This price of return earns FUL a maintain suggestion right now.

Last Ideas

H.B. Fuller is extremely weak to recessions, nevertheless it has proved markedly resilient throughout the pandemic, due to a powerful enhance in adhesives demand utilized in well being and hygiene merchandise.

Furthermore, due to the dependable long-term development of its area of interest market and its excessive fragmentation, H.B. Fuller is more likely to develop its earnings per share at a excessive single-digit price within the upcoming years.

Nevertheless, the corporate additionally seems to be barely overvalued, whereas the 1.1% dividend yield just isn’t that compelling. In consequence, we’re considerably impartial on H.B. Fuller.

The next articles comprise shares with very lengthy dividend or company histories, ripe for choice for dividend development buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link