[ad_1]

Up to date on November twenty fourth, 2023

The Dividend Kings are an illustrious group of firms. These firms stand other than the overwhelming majority of the market as they’ve raised dividends for no less than 50 consecutive years.

We imagine that buyers ought to view the Dividend Kings as probably the most high-quality dividend progress shares to purchase for the long run.

With this in thoughts, we created a full checklist of all of the Dividend Kings. You may obtain the complete checklist, together with necessary monetary metrics resembling dividend yields and price-to-earnings ratios, by clicking the hyperlink under:

This group is so unique that there are simply 53 firms that qualify as a Dividend King. One of many constituents of the Dividend Kings checklist is Middlesex Water Firm (MSEX), a water utility firm that has been in enterprise for over 125 years.

This text will focus on the corporate’s enterprise overview, progress prospects, aggressive benefits, and anticipated returns.

Enterprise Overview

Middlesex Water Firm was shaped in 1897, making the corporate one of many oldest water and wastewater utility names within the U.S. The corporate has operations primarily in New Jersey, and annual income of roughly $160 million.

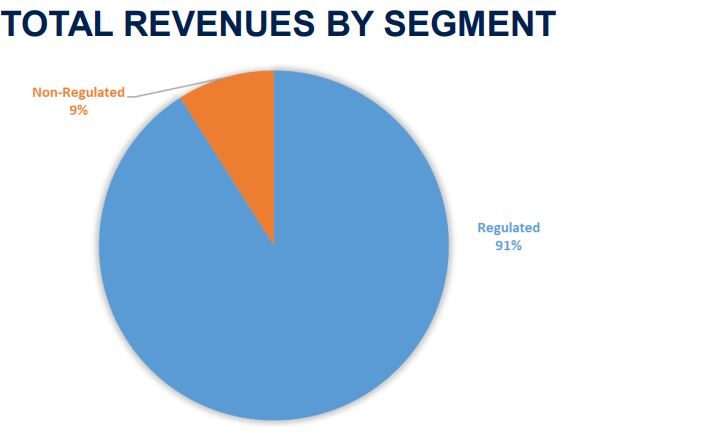

Like lots of its friends, Middlesex is primarily centered on the regulated portion of its enterprise.

Supply: Investor Presentation

Middlesex’s supplies primary water-related companies to prospects, resembling promoting, distributing, amassing, and treating water. The non-regulated enterprise consists of service contracts that embody the operation and upkeep of municipal personal water and wastewater methods in New Jersey and Delaware.

The overwhelming majority of income comes from the regulated aspect. One among its largest service areas consists of Middlesex County, the place the corporate supplies water companies to over 61,000 retail prospects. This enterprise contributed ~60% of income final 12 months.

Middlesex most lately reported third-quarter earnings in November. Income decreased by $1.0 million to $46.7 million in comparison with the identical interval in 2022. This decline was primarily as a consequence of decrease buyer demand in each their Middlesex and Delaware methods, partially offset by a rise in prospects and a fee improve permitted by the New Jersey Board of Public Utilities.

MSEX’s web revenue for the quarter decreased by $4.3 million in comparison with 2022, with diluted earnings per share at $0.56, down from $0.80 in 2022.

For the 9 months ending September 30, 2023, revenues elevated by $4.1 million to $127.7 million in comparison with the identical interval in 2022. This improve was largely because of the last section of the NJBPU-approved base fee improve, offset by decreased revenues within the Delaware System and decrease new connection charges.

The online revenue for the nine-month interval decreased by $9.5 million in comparison with 2022, with diluted earnings per share dropping to $1.44 from $1.99 within the earlier 12 months.

Progress Prospects

Utility firms are usually labeled as sluggish, however regular growers. This doesn’t essentially apply to Middlesex, nonetheless, as the corporate had an earnings-per-share compound annual progress fee of 10% for the 2012 to 2021 time interval. This can be a robust progress fee for a enterprise that’s principally regulated. It ought to be famous that progress for the corporate hasn’t at all times been in a straight line up over the long-term.

For the reason that majority of income comes from regulated enterprise, Middlesex is on the mercy of the approval of fee will increase to develop.

Happily, the corporate closely invests in its infrastructure to be able to justify buyer fee will increase. For instance, the New Jersey Board of Public Utilities permitted a 40% improve in Middlesex’s charges in one of many firm’s largest service areas for 2022. This wasn’t only a one-time elevate both, because the approval board has at all times permitted the corporate’s request to lift charges.

It’s probably that fee will increase will proceed to be a significant factor for the corporate as Middlesex continues to make heavy investments into getting older water infrastructure. This won’t solely enhance the standard of operations, but additionally result in fee hikes being permitted.

Along with fee will increase, Middlesex can develop by including new prospects whereas additionally protecting present prospects.

For instance, Middlesex accomplished a brand new settlement to proceed to handle water and sewer utility operations with the Borough of Avalon, New Jersey. The brand new 10-year settlement takes the place of the prior contract. The brand new contract supplies for upkeep of operations and buyer companies.

The non-regulated enterprise may very well be a serious supply of progress as properly. In 2013, Middlesex was awarded a $32 million contract to assemble and keep the water distribution community for the Dover Air Drive Base in Delaware. This contract will present a long time of recurring income, because the contract is for 50 years.

We anticipate MSEX will generate 6% earnings-per-share progress over the following 5 years.

Aggressive Benefits & Recession Efficiency

Utility firms typically profit from a number of benefits. The primary is that they often function in a near-monopoly on the areas that they service.

Within the case of water utilities, Middlesex and its friends supplies probably the most primary staple of all, water. Clients are going to wish the companies that the corporate presents whatever the power of the financial system. Water payments are additionally typically low in comparison with different utility payments.

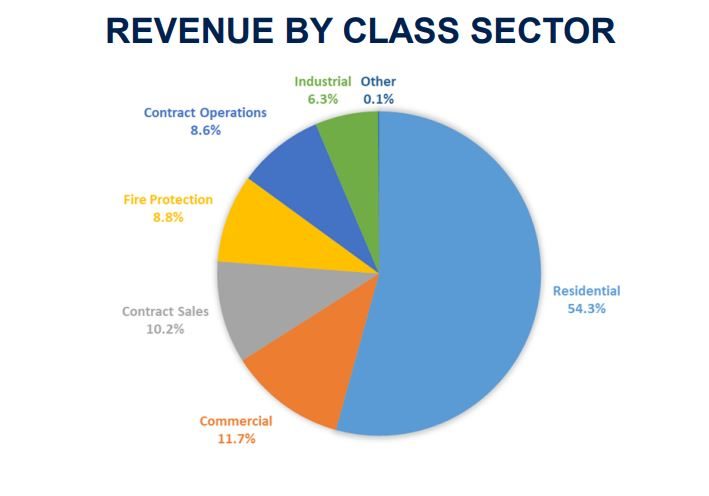

Middlesex additionally advantages from its diversified enterprise.

Supply: Investor Presentation

Middlesex receives barely greater than 50% of its income from residential prospects, however there are different classes, resembling business, contract gross sales, and hearth safety, that contribute meaningfully to the corporate’s enterprise.

Given these built-in benefits, many utilities typically outperform different sectors of the market throughout recessions. Under are Middlesex’s earnings-per-share outcomes earlier than, throughout, and after the Nice Recession:

- 2006 earnings-per-share: $0.82

- 2007 earnings-per-share: $0.87 (6.1% improve)

- 2008 earnings-per-share: $0.89 (2.3% improve)

- 2009 earnings-per-share: $0.72 (19.1% lower)

- 2010 earnings-per-share: $0.96 (33.3% improve)

Middlesex’s earnings-per-share initially grew throughout the recessionary interval earlier than falling by a excessive double-digit quantity in 2009, displaying that the utility wasn’t fully resistant to the financial backdrop of the interval. One optimistic was that income stayed comparatively flat for the 2008 to 2009 interval.

Importantly, the corporate rebounded in a considerable means the very subsequent 12 months and set a brand new excessive for earnings-per-share. Progress has principally been in an uptrend since.

Valuation & Anticipated Whole Returns

Middlesex gained entrance into the Dividend Kings following the corporate’s dividend improve announcement on October twenty first, 2022. MSEX presently yields 2%. The corporate has paid a steady dividend since 1912.

As beforehand talked about, we anticipate 6% EPS progress yearly over the following 5 years.

Lastly, the final element of complete returns will probably be valuation. Shares are presently buying and selling at 32.4 instances our earnings-per-share projection for the 12 months.

Given the corporate’s tailwinds and enterprise mannequin, we imagine truthful worth is 30 instances earnings, which is the typical valuation of the inventory for the final 5 years. Reverting to our goal valuation by 2028 would lead to a a number of contraction decreasing annual returns by 1.5%.

Subsequently, Middlesex is forecasted to return 5.4% yearly by way of 2028.

Last Ideas

There may be a lot to love about Middlesex, particularly its monopoly standing, the excessive success of fee improve approvals, and the lengthy historical past of dividend progress. Solely probably the most well-run companies will pay dividends for so long as Middlesex has.

That mentioned, the inventory is buying and selling at a premium to even its personal lofty valuation common since 2017. Regardless of the attractiveness of the corporate and its dividend progress streak, we imagine buyers are higher off elsewhere as forecasted returns over the medium time period are very weak.

The next articles include shares with very lengthy dividend or company histories, ripe for choice for dividend progress buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link