[ad_1]

Revealed on January twenty second, 2024 by Bob Ciura

The Dividend Kings include corporations which have raised their dividends for at the very least 50 years in a row. Due to their unparalleled streak of annual dividend will increase, it’s common to view the Dividend Kings as among the many finest dividend development shares within the inventory market.

You’ll be able to see the total record of all 54 Dividend Kings right here.

We additionally created a full record of all Dividend Kings, together with related monetary statistics like dividend yields and price-to-earnings ratios. You’ll be able to obtain the total record of Dividend Kings by clicking on the hyperlink beneath:

Consolidated Edison (ED) not too long ago elevated its dividend for the fiftieth consecutive 12 months. In consequence, the corporate now joins the unique record of Dividend Kings.

Through the years, utilities have change into relied upon for his or her regular dividend payouts, even throughout recessions. This text will analyze the corporate’s enterprise overview, future development prospects, aggressive benefits, and extra.

Enterprise Overview

Consolidated Edison is a large-cap utility inventory. The corporate generates roughly $14 billion in annual income and has a market capitalization of roughly $31 billion.

The corporate serves over 3 million electrical clients, and one other 1 million fuel clients, in New York. It operates electrical, fuel, and steam transmission companies.

On October 1st, 2022, Consolidated Edison introduced that it was promoting its curiosity in its renewable vitality enterprise to RWE Renewables Americas, LLC for $6.8 billion. The transaction is anticipated to shut within the first half of 2023. Because of this transaction, Consolidated Edison is not going to subject widespread inventory this 12 months whereas additionally withdrawing its share issuance steerage for 2023 and 2024. The corporate sometimes commonly points shares for financing.

On November third, 2023, Consolidated Edison reported third quarter outcomes for the interval ending June thirtieth, 2023. For the quarter, income grew 7% to $3.87 billion, which was $36 million greater than anticipated. Adjusted earnings of $561 million, or $1.62 per share, in comparison with adjusted earnings of $579 million, or $1.63 per share, within the earlier 12 months. Adjusted earnings-per-share had been $0.03 above estimates.

As with prior quarters, greater fee bases for fuel and electrical clients had been the first contributors to leads to the CECONY enterprise, which is accounts for the overwhelming majority of the corporate’s property. Common fee base balances are anticipated to develop by 6% yearly by 2025. Consolidated Edison expects capital investments of practically $15 billion for the 2023 to 2025 interval.

Consolidated Edison supplied up to date steerage for 2023 as nicely. The corporate now expects adjusted earnings-per share in a spread of $5.00 to $5.10 for 2023, up from $4.85 to $5.00 and $4.75 to $4.95, beforehand. On the new midpoint, this is able to be a ten.5% improve from the prior 12 months.

Progress Prospects

Earnings development throughout the utility business sometimes mimics GDP development. Over the subsequent 5 years, we count on Consolidated Edison to extend earnings-per-share by 3.5% per 12 months.

We count on ConEd to proceed its sample of modest development transferring ahead. ConEd ought to proceed to generate modest earnings development annually by a mix of latest buyer acquisitions and fee will increase, helped by the gradual enchancment of the U.S. economic system and a return to normalized climate circumstances,

The expansion drivers for Consolidated Edison are new clients and fee will increase. One good thing about working in a regulated business is that utilities are permitted to boost charges frequently, which nearly assures a gentle degree of development.

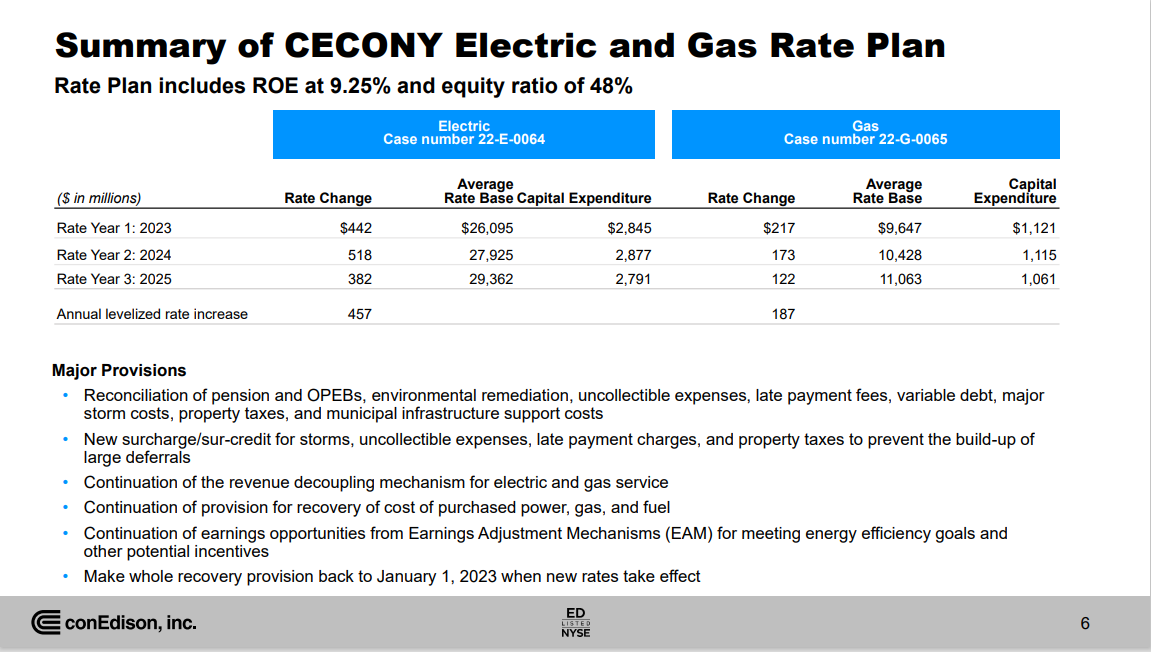

Supply: Investor Presentation

Consolidated Edison expects to extend its fee base by ~7% annually, by 2024. This can be a pure method for a utility to generate regular income and earnings development.

One potential risk to future development is rising rates of interest, which might improve the price of capital for corporations that make the most of debt, reminiscent of utilities. Happily, the market is more and more anticipating the Federal Reserve to cease elevating rates of interest this 12 months and probably even start to chop them. Decreasing charges helps corporations that rely closely on debt financing, reminiscent of utilities, so traders don’t have to be involved about Consolidated Edison in a falling-rate cycle.

Even when charges do proceed to go up, Consolidated Edison is in sturdy monetary situation. It has an investment-grade credit standing of A-, and a modest capital construction with balanced debt maturities over the subsequent a number of years. A wholesome steadiness sheet and powerful enterprise mannequin assist present safety to Consolidated Edison’s dividends.

Buyers can moderately count on low single-digit dividend will increase annually, at a fee just like the corporate’s annual adjusted earnings-per-share development.

Aggressive Benefits & Recession Efficiency

Consolidated Edison’s foremost aggressive benefit is the excessive regulatory hurdles of the utility business. Electrical energy and fuel providers are crucial and important to society. In consequence, the business is very regulated, making it nearly inconceivable for a brand new competitor to enter the market. This supplies an excessive amount of certainty to Consolidated Edison.

As well as, the utility enterprise mannequin is very recession-resistant. Whereas many corporations skilled giant earnings declines in 2008 and 2009, Consolidated Edison held up comparatively nicely. Earnings-per-share throughout the Nice Recession are proven beneath:

- 2007 earnings-per-share of $3.48

- 2008 earnings-per-share of $3.36 (3% decline)

- 2009 earnings-per-share of $3.14 (7% decline)

- 2010 earnings-per-share of $3.47 (11% improve)

Consolidated Edison’s earnings fell in 2008 and 2009 however recovered in 2010. The corporate nonetheless generated wholesome income, even throughout the worst of the financial downturn. This resilience allowed Consolidated Edison to proceed growing its dividend annually.

The identical sample held up in 2020 when the U.S. economic system entered a recession because of the coronavirus pandemic. Final 12 months, ConEd remained extremely worthwhile, which allowed the corporate to boost its dividend once more.

Valuation & Anticipated Returns

Utilizing the present share worth of ~$89 and the midpoint of 2023 steerage, the inventory trades with a price-to-earnings ratio of 17.6. That is above our honest worth estimate of 16.0, which is according to the 10-year common price-to-earnings ratio for the inventory.

In consequence, Consolidated Edison shares look like overvalued. If the inventory valuation retraces to the honest worth estimate, the corresponding a number of contractions would scale back annualized returns by 1.9%.

Happily, the inventory might nonetheless present constructive returns to shareholders, by earnings development and dividends. We count on the corporate to develop earnings by 3.5% per 12 months over the subsequent 5 years. As well as, the inventory has a present dividend yield of three.7%.

Utilities like ConEd are prized for his or her steady dividends and protected payouts. Placing all of it collectively, Consolidated Edison’s whole anticipated returns might seem like the next:

- 3.5% earnings development

- -1.9% a number of reversion

- 3.7% dividend yield

Added up and Consolidated Edison is anticipated to return 5.3% yearly over the subsequent 5 years. This can be a modest fee of return, however not excessive sufficient to warrant a purchase suggestion.

Earnings traders might discover the yield enticing, as the present yield is meaningfully greater than the yield of the S&P 500 Index and grows very persistently. The corporate has a projected payout ratio of 64%, which signifies a sustainable dividend.

Ultimate Ideas

Consolidated Edison is usually a beneficial holding for revenue traders, reminiscent of retirees, resulting from its 3.7% dividend yield. The inventory provides safe dividend revenue, and can also be a Dividend King, that means it ought to increase its dividend annually.

Due to this fact, risk-averse traders trying primarily for revenue proper now–reminiscent of retirees–might see better worth in shopping for utility shares like Consolidated Edison. Nevertheless, we fee the inventory as a maintain at right this moment’s present worth of $89.

The next articles comprise shares with very lengthy dividend or company histories, ripe for choice for dividend development traders:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link