[ad_1]

Up to date on January twenty seventh, 2024

Every year, we individually evaluate every of the Dividend Aristocrats, a bunch of 68 shares within the S&P 500 Index that has raised their dividends for at the very least 25 consecutive years.

To make it on the listing of Dividend Aristocrats, an organization should possess a worthwhile enterprise mannequin with a useful model, world aggressive benefits, and the flexibility to resist recessions. That is why Dividend Aristocrats can proceed elevating dividends in troublesome years.

With this in thoughts, now we have created an inventory of all 68 Dividend Aristocrats.

You may obtain your free copy of the Dividend Aristocrats listing, together with essential monetary metrics reminiscent of price-to-earnings ratios and dividend yields, by clicking on the hyperlink under:

Disclaimer: Positive Dividend shouldn’t be affiliated with S&P International in any means. S&P International owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet relies on Positive Dividend’s personal evaluate, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person buyers higher perceive this ETF and the index upon which it’s based mostly. Not one of the data on this article or spreadsheet is official information from S&P International. Seek the advice of S&P International for official data.

Caterpillar Inc. (CAT) joined the Dividend Aristocrats listing in 2019. Much more spectacular is the truth that Caterpillar operates in a extremely cyclical {industry}, which usually prevents firms from attaining lengthy histories of annual dividend will increase.

Nevertheless, Caterpillar’s administration staff has confirmed its dedication to returning money to shareholders even by means of the inevitable ebbs and flows of the enterprise over time. Caterpillar additionally has sturdy aggressive benefits that enable it to boost its dividend every year, even by means of downturns within the world economic system.

Enterprise Overview

Caterpillar was based in 1925 and in the present day competes within the manufacturing and promoting of development and mining gear. The corporate additionally manufactures ancillary industrial merchandise reminiscent of diesel engines and gasoline generators. Caterpillar inventory has a market capitalization of ~$160 billion, making it one of many largest industrial shares on this planet.

Industrial producers benefited from sturdy demand in 2022 and 2021, which fueled progress and spurred world financial exercise off the low base established in 2020 amid the pandemic.

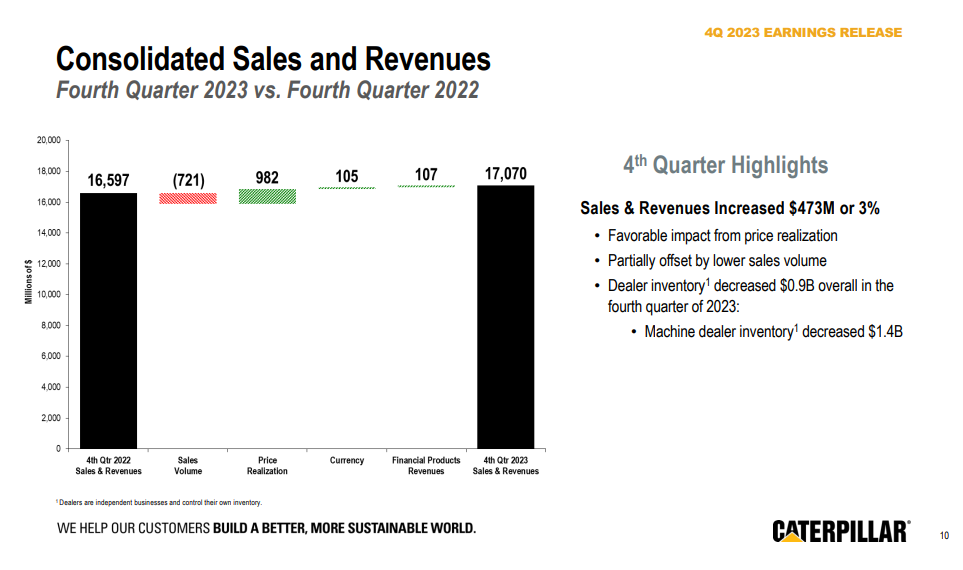

On February fifth, 2024, Caterpillar reported its This autumn and full-year outcomes for the interval ending December thirty first, 2023. For the quarter, the corporate generated revenues of $17.1 billion, a 3% enhance in comparison with the $16.6 billion posted within the fourth quarter of 2022.

Supply: Investor Presentation

The Development Industries and Useful resource Industries segments posted a decline of 15% and 6% in revenues, respectively. Nevertheless, these declines have been greater than offset by 12% larger revenues within the Power & Transportation section.

Caterpillar’s adjusted working revenue margin was 18.9%, in comparison with 17.0% final 12 months. Margin growth mixed with income progress resulted in adjusted earnings-per-share touchdown at $5.23 in opposition to $3.86 within the comparable interval final 12 months. For the 12 months, adjusted earnings-per-share surged 53% to $21.21. For FY2024, we count on adjusted EPS of $21.30.

Development Prospects

Caterpillar is intently tied to world financial progress and commodity costs. Its clients extract assets from the earth and construct and assemble all kinds of buildings, so financial progress is vital to funding that growth.

This results in some pretty excessive cyclicality in Caterpillar’s outcomes, which then sees the inventory swing wildly between extremes of the sentiment scale.

The coronavirus pandemic weighed closely on the corporate, however the world financial restoration that ensued enabled Caterpillar to change into extremely worthwhile in 2021 and 2022. Caterpillar is offsetting elevated manufacturing prices with elevated pricing. Caterpillar generated document leads to 2023.

Whereas outcomes could proceed to be unstable, it seems the corporate is again on monitor. In truth, the $1.2 trillion bipartisan infrastructure invoice ought to to maintain sturdy demand for Caterpillar’s equipment.

We’re forecasting $21.30 in earnings-per-share for 2024 to go together with a 3% progress charge over the subsequent 5 years.

This displays each some warning with regard to the cyclical nature of the enterprise and Caterpillar’s means to bounce again when demand returns.

Aggressive Benefits & Recession Efficiency

Aggressive benefits in industrial purposes could be difficult, provided that some opponents make related merchandise for many purposes.

Nevertheless, over time, Caterpillar has constructed itself into one of many largest gamers in profitable finish markets reminiscent of development, vitality, and mining.

Its world presence affords it some diversification of income by section and {industry}, but additionally geographically, which has served it nicely lately. Its scale additionally provides it the flexibility to leverage down variable prices per unit, which boosts margins.

Nevertheless, Caterpillar is actually not immune from recessions, as slowdowns within the world economic system are usually accompanied by decrease commodity costs and slowing development spending.

These components took a serious toll on Caterpillar’s backside line through the Nice Recession, as its earnings have been devastated, if solely briefly.

Caterpillar’s earnings-per-share through the Nice Recession are under:

- 2007 earnings-per-share of $5.32

- 2008 earnings-per-share of $5.71 (7% enhance)

- 2009 earnings-per-share of $1.43 (75% decline)

- 2010 earnings-per-share of $4.15 (190% enhance)

Whereas Caterpillar actually felt the ache from the Nice Recession, its earnings rebounded pretty shortly and reclaimed its pre-recession earnings-per-share quantity in 2011.

Caterpillar additionally skilled a big decline in earnings-per-share in 2020 as a result of coronavirus pandemic however recovered strongly since then in a brief time frame.

Due to this fact, it’s clear that Caterpillar is uncovered to recessions as a result of financial bellwether nature of the heavy equipment {industry}. Nevertheless it additionally has a historical past of recovering from downturns pretty shortly.

Valuation & Anticipated Returns

Caterpillar’s present price-to-earnings ratio is 15.2, based mostly on the 2024 anticipated EPS of $21.30. That is an elevated valuation degree for Caterpillar. Since 2013, shares of Caterpillar have traded with a median P/E ratio of about 17. We consider 15 is an affordable, honest worth estimate for Caterpillar, given its cyclical enterprise and vulnerability to recessions and the present rising charge setting.

Durations of cyclicality are regular for Caterpillar in terms of valuation. Nonetheless, the inventory seems to be simply barely overvalued. A declining P/E a number of might scale back future returns; if the P/E a number of declines from 15.2 to fifteen.0 over the subsequent 5 years, it could decrease annual returns by 0.3% per 12 months in that timeframe.

The opposite unfavorable facet of shares with elevated valuations is that additionally they have decrease dividend yields. As Caterpillar’s share value has risen up to now 12 months, its dividend yield has declined to 1.6%. Dividends and earnings-per-share progress (anticipated at 3% per 12 months) will add to shareholder returns, however the overvaluation of the inventory is a hurdle to clear.

Primarily based upon the components mentioned above, we see whole returns of 4.3% per 12 months. This leads us to charge Caterpillar a maintain in the present day.

Ultimate Ideas

Caterpillar inventory continues its spectacular rise, having elevated over 35% up to now one 12 months in comparison with a 27% rise within the S&P 500 index. Ends in 2024 are anticipated to be sturdy, simply as in 2023 when income and earnings-per-share surged considerably as a result of sturdy demand and rising commodity costs. Whereas the inventory is buying and selling above its common PE and our honest worth estimate, it’s not severely overvalued.

Caterpillar has an industry-leading model and a constructive long-term progress outlook, however we really feel the inventory has merely change into overpriced as a result of rally because the pandemic lows. With a mid-single digit anticipated future return, we charge the inventory a maintain. Buyers could also be higher off look forward to a decline within the share value.

Additional studying: See evaluation on our favourite agriculture shares.

Moreover, the next Positive Dividend databases comprise probably the most dependable dividend growers in our funding universe:

In the event you’re in search of shares with distinctive dividend traits, think about the next Positive Dividend databases:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link

:max_bytes(150000):strip_icc()/GettyImages-1484627119-cbcd57b8b8d54643a8c399765fd5c922.jpg)