[ad_1]

Up to date on March nineteenth, 2024 by Bob Ciura

Lowe’s Firms (LOW) has a extremely spectacular observe document of long-term dividend progress. The corporate has elevated its dividend for over 50 years in a row. This makes Lowe’s a uncommon dividend inventory, even among the many Dividend Aristocrats, as the corporate qualifies for Dividend King standing due to greater than 5 many years of annual dividend will increase.

Yearly, we evaluate every of the Dividend Aristocrats, a gaggle of 68 corporations within the S&P 500 Index with 25+ consecutive years of dividend will increase.

Now we have constructed a full record of all 68 Dividend Aristocrats. You’ll be able to obtain a free copy of our Dividend Aristocrats record, together with vital metrics like dividend yields and payout ratios, by clicking on the hyperlink beneath:

Disclaimer: Positive Dividend isn’t affiliated with S&P International in any approach. S&P International owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet is predicated on Positive Dividend’s personal evaluate, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person traders higher perceive this ETF and the index upon which it’s primarily based. Not one of the data on this article or spreadsheet is official knowledge from S&P International. Seek the advice of S&P International for official data.

Along with being a Dividend Aristocrat, Lowe’s is on the unique record of Dividend Kings, which have raised their dividends for a tremendous 50+ years in a row. You’ll be able to see the whole record of Dividend Kings right here.

Lowe’s is also a high-growth dividend inventory. This text will focus on Lowe’s’ enterprise mannequin, progress potential, and valuation.

Enterprise Overview

Lowe’s was based in 1946. Within the 75 years since, it has grown into the second largest house enchancment retailer, behind solely The Dwelling Depot (HD).

The corporate operates greater than 1,700 shops within the U.S., Canada, and Mexico. Lowe’s affords a variety of merchandise, for upkeep, restore, reworking, and adorning the house. It has a big selection of main nationwide manufacturers, in addition to numerous personal manufacturers.

Lowe’s reported fourth quarter 2023 outcomes on February twenty seventh, 2024. Whole gross sales got here in at $18.6 billion in comparison with $22.4 billion in the identical quarter a 12 months in the past. Comparable gross sales decreased by 6.2%, whereas web earnings-per-share of $1.77 in comparison with $1.58 in fourth quarter 2022.

Nonetheless, adjusted EPS within the year-ago interval was $2.28 when excluding the transaction prices associated to the sale of the Canadian retail enterprise within the prior 12 months. The corporate continues to be negatively impacted from a discount in DIY discretionary spending.

The corporate repurchased 1.9 million shares within the fourth quarter for $404 million. Moreover, it paid out $633 million in dividends.

Lowe’s initiated its fiscal 2024 outlook and expects to earn adjusted diluted EPS of $12.00 to $12.30 on complete gross sales of $84 to $85 billion. Capex will probably are available at $2 billion, and Lowe’s expects an working margin of 12.6% to 12.7%.

Progress Prospects

We consider that Lowe’s will ship 9% annual earnings-per-share progress over the following 5 years. Lowe’s has an extended runway of progress up forward.

Lowe’s has made a concerted effort in recent times to enhance its in-store expertise for purchasers by way of merchandising and stock apply optimization, in addition to investing within the capabilities to satisfy orders outdoors of its shops.

This consists of particular options for Professional prospects that drive recurring income, in addition to making it simpler for DIY prospects to order their merchandise on-line, and choose them up or have them delivered. It is a strategic shift from the outdated mannequin Lowe’s operated beneath, and it has labored properly in recent times.

Lowe’s usually opens a small variety of new shops every year, so that’s not a significant driver of progress. Nonetheless, it continues to seek out methods to capitalize on rising housing and development spending, and we see these as progress drivers shifting ahead attributable to nonetheless comparatively low mortgage charges, whether or not or not the shop rely rises.

The U.S. economic system continues to develop, regardless of progress headwinds reminiscent of excessive inflation charges. Optimistic GDP progress is arguably crucial financial indicator for Lowe’s, as the corporate is very reliant on shopper spending. The continued U.S. financial progress is a constructive catalyst for Lowe’s.

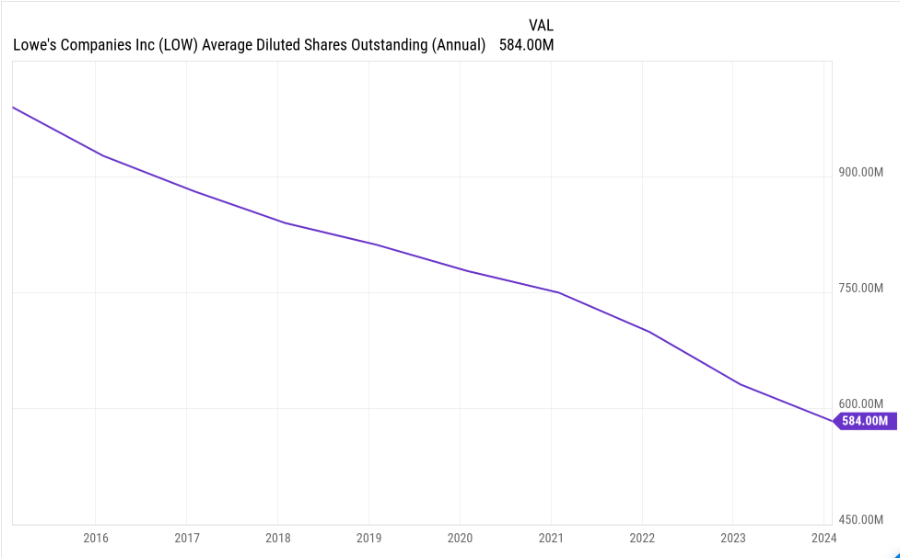

Lowe’s has steadily been repurchasing shares on the open market in recent times. These buybacks shrink the corporate’s share rely, which interprets right into a rising portion of the general income that the corporate generates for every remaining share.

Buybacks have been a serious driver within the compelling earnings-per-share progress that Lowe’s loved, and we consider the identical will maintain true sooner or later:

Supply: YCharts

The mixture of continued enlargement in e-commerce, total financial progress in the long term, and working ought to drive income for Lowe’s. With the influence of buybacks added, we consider annual earnings-per-share progress within the mid-single-digit vary could be very a lot achievable.

Aggressive Benefits & Recession Efficiency

The retail trade usually doesn’t provide many aggressive benefits. It is a extremely difficult retail setting, because the rise of Amazon and different Web retailers threatens to undercut brick-and-mortar shops. Customers have shifted spending {dollars} towards e-commerce for the comfort and low costs.

Nonetheless, Lowe’s is a specialty retailer, which gives it with a aggressive benefit. Dwelling enchancment tasks are sometimes advanced. Customers are keen to journey to shops, to examine merchandise in individual, and to ask inquiries to employees members. This has helped shield house enchancment retailers from Amazon (AMZN).

That stated, Lowe’s isn’t immune from recessions. The buyer is vulnerable to declining throughout financial downturns. Lowe’s depends upon a financially-healthy shopper, with stable housing and development markets. The Nice Recession was a very steep downturn, which took a major toll on Lowe’s backside line.

Lowe’s earnings-per-share throughout the Nice Recession are beneath:

- 2007 earnings-per-share of $1.86

- 2008 earnings-per-share of $1.49 (20% decline)

- 2009 earnings-per-share of $1.21 (19% decline)

- 2010 earnings-per-share of $1.44 (19% enhance)

Lowe’s earnings fell sharply throughout the recession, however the firm nonetheless remained worthwhile. This helped it proceed rising its dividend every year. And, it bounced again fairly fast, as by 2013, Lowe’s earnings-per-share had surpassed 2007 ranges.

Valuation & Anticipated Returns

Lowe’s is anticipated to generate adjusted EPS of $12.15 for 2024. Because of this, the inventory trades at a price-to-earnings ratio of 20.2. That is above our honest worth estimate of 19, so we see the inventory as barely overvalued. Because of this, a contracting price-to-earnings ratio may cut back future returns by roughly 1.2% per 12 months for the following 5 years.

Along with valuation modifications, Lowe’s returns will include earnings progress and dividends.

We see annual earnings-per-share progress at 9% yearly, plus the present 1.8% yield, offset considerably by a declining valuation a number of. That will produce total complete annual returns of roughly 9.6%, which is a gorgeous potential price of return.

The dividend payout ratio stays close to 36% of earnings, so there may be actually loads of room for extra dividend progress within the coming years.

Last Ideas

Lowe’s has elevated its dividend for 60 consecutive years. The present setting is troublesome for retail, however Lowe’s operates in a distinct segment that ought to stand up to aggressive threats from on-line retailers.

Lowe’s continues to be rising gross sales and earnings, which ought to enable for continued dividend progress. And, it has a conservative dividend payout ratio, which additionally helps excessive dividend will increase. With a stable anticipated price of return of round 10% per 12 months, Lowe’s inventory receives a purchase ranking at present costs.

Moreover, the next Positive Dividend databases include essentially the most dependable dividend growers in our funding universe:

In the event you’re on the lookout for shares with distinctive dividend traits, contemplate the next Positive Dividend databases:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link

:max_bytes(150000):strip_icc()/GettyImages-1238317363-2993d6654aae4777bac34a9b18cd890e.jpg)