[ad_1]

Myths and misinformation about credit score scores, credit score reviews, and credit score restore are extraordinarily frequent. Sadly, many individuals imagine these myths, and their credit score suffers because of taking incorrect actions.

Let’s resolve these credit score myths and be taught the reality about them so you can begin enhancing your credit score the fitting approach.

Fantasy: Everybody routinely has a credit score rating.

Truth: 1 in 5 adults in america don’t have credit score scores.

A report by the Client Monetary Safety Bureau (CFPB) discovered that one-fifth of adults in america don’t have sufficient credit score information to calculate a credit score rating by conventional strategies. These shoppers are known as “credit score invisibles.”

Low-income shoppers are significantly vulnerable to credit score invisibility as a consequence of a scarcity of entry to conventional credit score merchandise. Some shoppers could also be credit score invisible for different causes, akin to a voluntary resolution to not use credit score.

For these that don’t use credit score for no matter motive, it’s doubtless that they don’t have sufficient credit score historical past to generate a credit score rating.

Shoppers which might be credit score invisible could possibly generate a credit score report by piggybacking on the great credit score of others, however don’t assume that everybody has a credit score rating simply by advantage of present.

Fantasy: Checking your credit score report will damage your credit score rating.

Truth: Checking your personal credit score is not going to damage your rating.

About one in 5 Individuals are credit score invisible, which suggests they don’t have credit score scores.

Checking your personal credit score report leads to what is named a “gentle pull,” which suggests the inquiry doesn’t have an effect on your credit score rating.

To know the distinction between arduous and gentle inquiries and the way they have an effect on your credit score rating, see our article, “Are Inquiries Actually Killing Your Credit score?”

Fantasy: Your earnings impacts your credit score rating.

Truth: Your credit score rating doesn’t take a look at your earnings.

Nevertheless, your earnings can have an effect on your credit score not directly in that it influences the “5 C’s” which were proven to foretell credit score efficiency: capability to repay money owed, the collateral backing a mortgage, capital obtainable to repay a mortgage, circumstances that have an effect on earnings and bills, and the character of the borrower.

Your capability to repay money owed in addition to the collateral and capital they’ve obtainable to repay loans might all have a relationship together with your earnings.

That’s a giant a part of the explanation why low-income shoppers are 8 instances extra doubtless than high-income shoppers to haven’t any credit score rating in any respect. In shoppers that do have credit score scores, those that reside in low-income areas have decrease credit score scores. As well as, low-income shoppers are 240 p.c extra more likely to have their credit score file originated as a consequence of derogatory gadgets akin to collections.

Every client can have dozens of various credit score scores.

So whereas your earnings just isn’t technically included into your credit score rating, it may possibly undoubtedly affect your potential to repay money owed, which is the idea of a credit score rating.

Fantasy: You solely have one credit score rating.

Truth: There are numerous completely different credit score scores.

There are two common kinds of credit score scores: FICO scores, developed by Honest Isaac Company, and VantageScore, developed by the three main credit score bureaus (Equifax, Experian, and TransUnion).

FICO 8 is the credit score rating mostly by lenders in the present day, however in some industries, older fashions or industry-specific fashions are used as an alternative. For instance, there are FICO scores tailor-made particularly towards auto loans and bank cards, and mortgage lenders are recognized to make use of the older FICO rating variations 2, 4, and 5. Plus, FICO scores are completely different for every credit score bureau.

VantageScore, which is more and more utilized by some lenders in addition to for client credit score schooling, additionally has a number of variations. The newest model is VantageScore 4.0, however VantageScore 3.0 continues to be essentially the most generally used model in the present day.

Altogether, between the various variations of FICO scores and VantageScores, shoppers can have dozens of various credit score scores.

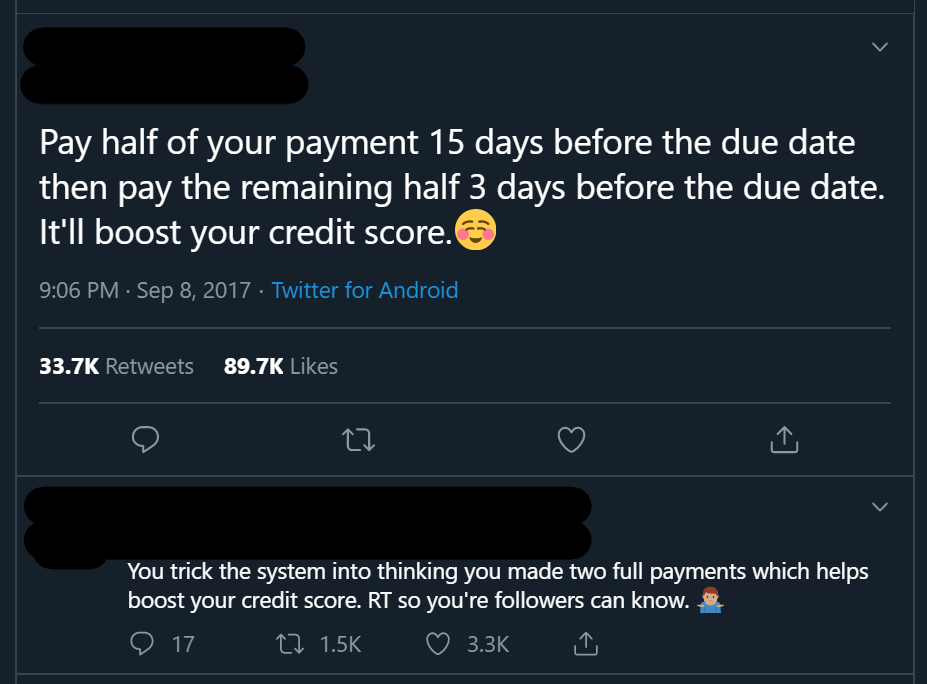

Fantasy: Paying half of your minimal cost twice a month counts as two full funds and methods the system into supplying you with twice the credit score rating increase.

Truth: Dividing your invoice in half and making two funds is identical as paying the total quantity as soon as.

This credit score delusion is unfounded but usually repeated.

If this “credit score hack” sounds slightly too good to be true, that’s as a result of it’s. It’s merely not true that you would be able to “trick the system” into pondering you may have made two full funds by making two half funds.

Making a cost on a credit score account impacts two principal elements of your credit score rating: cost historical past and credit score utilization. Let’s talk about every issue individually.

On the subject of your cost historical past, making a partial cost that’s lower than the minimal quantity due doesn’t fulfill the requirement and won’t depend as an on-time cost. Solely upon getting made the second cost for the opposite half of the quantity due will you may have glad the requirement to be thought-about paid on time.

Due to this fact, you don’t acquire any further profit to your cost historical past from dividing your cost into two components as an alternative of paying the total quantity at one time.

For instance, let’s say you may have a invoice due on the thirtieth and the minimal quantity it’s essential to pay is $50. We’ve got laid out the 2 cost eventualities within the desk beneath.

| Situation 1: Pay the total quantity in a single cost | Situation 2: Make half of the cost twice | ||||

| Date | Quantity Paid | Fee Standing | Date | Quantity Paid | Fee Standing |

| fifteenth | fifteenth | $25 | Inadequate cost—$25 nonetheless due | ||

| thirtieth | $50 | Paid on time | thirtieth | $25 | Paid on time |

As you’ll be able to see from the desk, in each eventualities, you solely get the good thing about paying your invoice on time as soon as per billing cycle, not twice.

Now let’s talk about the utilization issue. Persevering with with the identical instance, the overall quantity you’re paying towards the account is $50 in each eventualities. Due to this fact, the general enchancment in your utilization ratio goes to be the identical both approach.

Should you don’t have any credit score historical past, you’ll be able to start constructing credit score by piggybacking on another person’s good credit score.

Now, if the reporting date for that account is between the primary and second funds, since you may have already despatched a partial cost, it’s possible you’ll quickly get a small increase from having a barely decrease utilization ratio when the account reviews to the credit score bureaus. However on the finish of the billing cycle, the end result would be the similar.

Should you determine to make further funds along with your minimal cost, which is ideally what all accountable debtors must be doing, that may definitely assist your credit score rating by dashing up your debt reimbursement. However merely splitting the minimal cost into two funds gained’t do something to spice up your rating.

Though this so-called credit score hack sadly gained’t assist your credit score very a lot, you will discover some methods that do work in our record of Simple Credit score Hacks That Will Really Get You Outcomes.

Fantasy: Should you don’t have a credit score historical past, you’ll by no means be capable to get credit score.

Truth: You can begin constructing credit score by piggybacking.

Whereas it may possibly undoubtedly be tougher to get credit score once you don’t have any credit score historical past to start with, it’s not unattainable. There are credit score merchandise on the market designed for individuals with no credit score or low credit, akin to secured bank cards and credit-builder loans.

One other technique to begin constructing credit score quick is by piggybacking off of the great credit score of another person. You would have somebody you belief cosign on a mortgage or open a joint account with you, or you would turn out to be a licensed person on another person’s seasoned tradeline.

In case you are not fortunate sufficient to know somebody who has a seasoned account with excellent cost historical past that they might add you to, think about buying tradelines from a respected tradeline firm.

Fantasy: Paying off a set will “re-age” the debt as a result of the account falls off your credit score report primarily based on the date of final exercise.

It’s unlawful to “restart the clock” on collections.

Truth: Collections fall off your credit score seven years after the preliminary delinquency and can’t legally be re-aged.

Should you’ve learn our article about collections in your credit score report, then you recognize that it’s the date of first delinquency (DOFD) that determines when the gathering will likely be eliminated out of your credit score report, not the “date of final exercise” (DLA).

The rationale why some individuals might imagine this delusion is as a result of shady debt collectors generally illegally change the date of first delinquency to the date of final exercise in an try and re-age the debt.

As we stated, this observe is against the law. Should you discover {that a} debt collector has improperly modified any details about a set account in your credit score report, you may have the fitting to dispute the incorrect data.

Fantasy: Paying off a set will increase your credit score rating.

Truth: Paying off a set might or might not elevate your rating relying on which credit score rating is used.

Whereas it is sensible to imagine that paying off a set ought to improve your credit score rating, that’s not at all times the case. The truth is, most of the time, that is not the case, though it is determined by which credit score rating is getting used.

With FICO 8 and all earlier FICO scores, each paid and unpaid collections are categorized as main derogatory gadgets in your credit score report. Due to this fact, paying off the account is not going to change how it’s thought-about by the credit score scoring algorithm, which suggests your rating might not go up in any respect.

Alternatively, FICO 9, VantageScore 3.0, and VantageScore 4.0 ignore paid assortment accounts, so your rating ought to get well after paying off a set if one in every of these credit score scoring fashions is getting used.

Fantasy: You need to shut accounts you’re not utilizing.

Truth: You need to maintain accounts open and use them periodically.

Somewhat than closing bank cards you don’t use anymore, use them now and again to maintain them open and in good standing.

When you would possibly suppose that closing accounts you don’t want will assist your credit score rating, the other is definitely true, particularly with regards to revolving accounts akin to bank cards.

The primary motive for that is that credit score utilization is a crucial a part of your credit score rating, and shutting bank card accounts will damage your utilization ratio by lowering your credit score restrict.

It may additionally damage your mixture of credit score, though that’s a much less vital issue.

As well as, cost historical past is the primary issue that helps your rating. It’s higher in your credit score to maintain the account open, use it for small purchases right here and there or a month-to-month subscription, and pay it off each month to maintain constructing further optimistic cost historical past.

The exception to this rule is that if an account comes with an annual payment that’s not definitely worth the worth or if you happen to can’t resist the temptation to overspend. In these circumstances, it may be higher in your pockets to go forward and shut the account anyway.

Fantasy: Closed accounts don’t have an effect on your credit score.

Truth: Closed accounts can have a big influence in your credit score.

Though we simply mentioned why you shouldn’t essentially shut outdated accounts, that’s to not say that closed accounts don’t influence your credit score. They definitely can, significantly with regards to your credit score age.

Closing an account doesn’t take away its cost historical past or age out of your credit score report, so closed accounts nonetheless contribute to your credit score age. As well as, accounts can proceed to age even after they’ve been closed.

Carrying a stability in your bank cards is dear and isn’t needed to construct credit score. Photograph by Hloom on Flickr.

So though it’s finest to maintain accounts open if you happen to can, having closed accounts in your credit score report just isn’t a foul factor. If the account was closed in good standing, it’ll doubtless proceed to assist your credit score.

Fantasy: Carrying a stability in your bank cards will assist your credit score.

Truth: Carrying a stability is not going to enable you construct credit score and it’ll value you curiosity charges.

Whereas you will need to use credit score repeatedly when constructing credit score, it’s not needed to hold a stability in your bank cards from month to month. Should you do that in an try and construct credit score, you can be losing cash by paying pointless curiosity.

One of the simplest ways to construct credit score utilizing your bank cards is to make use of them responsibly after which pay the total stability due every month and even make a number of funds every month to maintain your utilization ratio as little as potential.

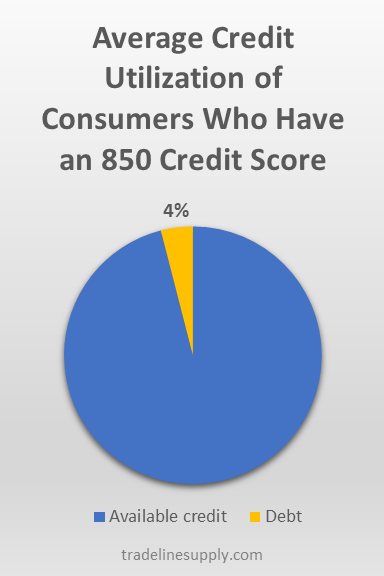

Fantasy: You need to maintain your total credit score utilization ratio beneath 30%.

Truth: You need to maintain your total utilization ratio as little as potential—and don’t overlook about your particular person utilization ratios.

The typical credit score utilization price of shoppers who’ve an 850 FICO rating is about 4%.

Whereas essentially the most often-repeated credit score recommendation says to maintain your credit score utilization beneath 30%, sadly, that’s not the magic quantity.

The truth is, there isn’t actually a magic quantity in any respect with regards to utilization ratios. One of the best rule of thumb is to maintain it as little as potential.

Creditcards.com says that the perfect utilization is having your entire playing cards report a zero stability, apart from one card within the 1-3% vary to point out that you’re really utilizing credit score.

Nevertheless, it’s nonetheless potential to have a excellent credit score rating whereas having an total utilization ratio of about 4%, as we talked about in “The right way to Get an 850 Credit score Rating.”

Should you can’t maintain your utilization between 0-10%, then attempt to shoot for round 20%, not 30%.

As well as, don’t overlook to bear in mind the utilization of your particular person revolving accounts. Having accounts with excessive particular person utilization ratios can nonetheless convey down your credit score rating, even when your total utilization ratio is within the ultimate vary.

You may learn extra credit score utilization suggestions in our article, “What Is the Distinction Between Particular person and General Credit score Utilization Ratios?”

Video: Why You Shouldn’t Consider This Fantasy About Credit score Utilization

Within the video beneath, credit score skilled John Ulzheimer addresses misconceptions about credit score utilization and offers you the details you’ll want to know.

Wish to see extra movies about credit score myths? Try our Credit score Fantasy Busters playlist on YouTube!

Fantasy: Buying round for the perfect charges on a mortgage will damage your credit score rating.

Truth: Getting mortgage estimates from a number of lenders is not going to damage your rating if you happen to full the method inside a selected time window.

Credit score scoring algorithms perceive that it’s sensible to buy round for the perfect charges on a mortgage, not dangerous. Due to this fact, credit score scores usually have methods of stopping the sequence of a number of inquiries that end result from this course of from hurting your rating excessively.

In case you are making use of for scholar loans, mortgages, or auto loans, FICO scores permit a sure timeframe so that you can store round, solely counting one arduous inquiry to your credit score report for this time interval. For older FICO scores, the time window is 14 days; for newer FICO scores, the time window is 45 days.

As well as, FICO scores have a 30-day arduous inquiry “buffer,” that means that the algorithm ignores any inquiries that occurred inside the previous 30 days when calculating your rating.

VantageScore makes use of an easier technique: it teams all inquiries made inside a 14-day window of one another collectively and counts these all as one inquiry, no matter what kinds of accounts the inquiries had been for.

Fantasy: You may repair your credit score by disputing all the pieces in your credit score report.

Truth: Disputing all the pieces in your credit score report may get you into authorized hassle and will not even assist your credit score.

If there may be data in your credit score report that’s inaccurate, outdated, incomplete, or unverifiable, in fact, you’ll wish to dispute these inaccurate gadgets with the credit score bureaus. Nevertheless it’s not essentially a good suggestion to dispute detrimental gadgets in your credit score report that are correct and well timed.

To start with, the derogatory gadgets gained’t essentially get deleted out of your credit score report, particularly if you happen to don’t present proof that they’re inaccurate. They may simply get up to date with the proper data, or they could get deleted quickly till an investigation determines the gadgets are legitimate and so they go proper again in your credit score report.

Moreover, the credit score bureaus don’t have to analyze disputes which might be deemed “frivolous,” and so they may determine that a few of your disputes are frivolous if you’re disputing each merchandise in your credit score file, no matter accuracy.

Plus, mendacity on a credit score dispute might be thought-about fraudulent. In keeping with the FTC, “Nobody can legally take away correct and well timed detrimental data from a credit score report.”

Even if you happen to had been to get away with disputing all the pieces in your report, this may not essentially assist your credit score as a lot as you hoped. Should you’ve gone by way of an aggressive credit score sweep and don’t have anything left in your report, you then primarily haven’t any credit score historical past and certain no credit score rating, which might be simply as problematic as having low credit.

Fantasy: CPN numbers can be utilized instead of social safety numbers to create a brand new, clear credit score file.

Truth: CPNs are unlawful and utilizing one to use for credit score is a federal crime.

Utilizing a CPN to use for credit score is a federal crime. Photograph by way of seniorliving.org.

Though you may need heard some individuals declare that “credit score profile numbers” or credit score privateness numbers” are a official technique to defend your privateness or wipe your credit score slate clear, in actuality, there isn’t any official or authorized supply for CPN numbers.

More often than not, these numbers are both faux social safety numbers that haven’t been created but or actual SSNs which were stolen from kids, the aged, deceased individuals, people who find themselves incarcerated, and people who find themselves homeless. Both approach, utilizing a CPN means getting concerned in id fraud, which is a federal crime.

The Social Safety Administration and the Federal Commerce Fee have each explicitly said that making use of for credit score utilizing a CPN is against the law and that those that promote CPNs are scamming shoppers.

Study extra about the hazards of CPNs in our article on the subject.

Fantasy: The credit score rating you test on-line is identical one lenders see after they pull your credit score.

Truth: Lenders usually don’t use the identical credit score scores which might be supplied at no cost on-line.

If you test your credit score rating at no cost on-line, the credit score rating you see is most probably going to be a VantageScore. That is the rating mostly utilized by free on-line providers akin to Credit score Karma.

Nearly all of lenders, nonetheless, primarily use FICO scores, though some lenders at the moment are beginning to use VantageScore. Simply remember the fact that the rating you see on-line is probably not the identical because the rating lenders see, as there can usually be a big distinction between your VantageScore and your FICO rating.

If you wish to test your FICO rating at no cost, test together with your bank card issuer, since many banks now provide this service freed from cost.

Fantasy: Should you don’t have any debt, you should have a superb credit score rating.

Truth: It’s good to use credit score to construct your credit score rating.

Having good credit score doesn’t simply come all the way down to the quantity of debt you may have—that’s only one a part of your credit score rating. Fee historical past is crucial a part of a credit score rating, so if you happen to’ve by no means had debt and also you don’t have any cost historical past, you may not actually have a credit score rating in any respect.

To get a superb credit score rating, it’s important to use some type of credit score and exhibit that you should utilize credit score responsibly by build up a optimistic cost historical past over time.

Fantasy: There’s no have to test your credit score report till it’s time to use for a giant mortgage.

Truth: It’s vital to observe your credit score repeatedly.

Ready to test your credit score rating till you’ll want to apply for credit score is a mistake as a result of there might be errors in your credit score report bringing your rating down. Research estimate that about one-fifth of shoppers have no less than one error on their credit score report, a few of which might be severe sufficient to lead to larger rates of interest, much less favorable mortgage phrases, or being denied credit score.

It’s vital to regulate your credit score with the intention to right errors and combat fraud as quickly as potential as an alternative of ready till it’s too late. There are a number of respected web sites that provide free credit score monitoring, akin to Credit score Karma, and a few bank card issuers additionally present free entry to your credit score report and credit score rating.

In our article on what you’ll want to find out about credit score reviews, we clarify that more often than not, shoppers are allowed to entry their credit score reviews from every of the three main credit score bureaus yearly at no cost by going to annualcreditreport.com.

Nevertheless, throughout the COVID-19 pandemic, because it has precipitated a lot monetary stress and devastation for a lot of Individuals, the credit score bureaus are at present permitting shoppers to test their very own credit score reviews at no cost as much as as soon as every week till April 20, 2021.

Fantasy: A late cost will make your rating go down by 50 factors.

Truth: There isn’t a set quantity of factors that’s related to any explicit merchandise in your credit score report.

Whereas it’s definitely potential {that a} 30-day late cost may trigger a 50-point drop (or extra) in somebody’s credit score rating, this isn’t at all times going to be the case. There isn’t a fastened variety of factors that your rating will go up or down by for every merchandise in your credit score report. Somewhat, the way in which wherein a late cost impacts your rating is at all times going to rely in your particular person credit score profile.

There isn’t a set quantity of factors related to lacking a cost.

Credit score scoring algorithms are very advanced and so they incorporate a whole lot of variables, akin to how current the late cost is, whether or not you may have different late funds in your credit score historical past, and the way extreme the delinquency is, to not point out the myriad different variables related to the opposite classes inside a credit score rating.

As a result of delinquencies in your credit score report are at all times going to be relative to no matter else is in your file, there’s a “diminishing returns” impact the place the primary late cost hurts your rating essentially the most and every subsequent late cost tends to have a smaller influence.

Somebody who has a excessive credit score rating and has by no means missed a cost earlier than goes to expertise a extreme drop from their first missed cost, whereas somebody who already has late funds on their report and a decrease credit score rating goes to be damage much less by a subsequent late cost.

In keeping with credit score skilled John Ulzheimer in a weblog article, “Delinquencies, like inquiries, don’t have impartial worth… It’s fully inappropriate and incorrect to say that ‘X’ lowered my rating by ‘Y’ factors.”

He continues, “The late cost didn’t decrease your rating however as a result of including a late cost to a credit score report strikes different issues round it precipitated your rating to be completely different than it was earlier than the late cost was added. In case your rating is 50 factors decrease it’s not as if the brand new late cost lowered your rating 50 factors…however as a result of the addition of that merchandise precipitated a distinct analysis of EVERYTHING in your credit score reviews…the brand new actuality for you is 50 factors decrease.”

The identical precept goes for different gadgets in your credit score report as nicely, not simply late funds.

Fantasy: You don’t have to fret about your child’s credit score.

Truth: You need to regulate your child’s credit score report, too.

Be sure you monitor your child’s credit score along with your personal.

The proliferation of scammers and hackers stealing individuals’s personal data means even your child’s credit score profile might be prone to id theft. When individuals use “credit score profile numbers” (CPNs), for instance, these numbers are sometimes actual social safety numbers stolen from kids.

You don’t wish to wait till your little one is grown up and able to apply for credit score to comprehend they’ve low credit because of id theft. Think about freezing your child’s credit score to stop fraudsters from opening accounts of their identify.

Along with monitoring and defending your little one’s credit score, it’s also possible to assist your little one begin to construct credit score early in life by way of methods like credit score piggybacking. See “At What Age Can You Begin Constructing Credit score?” for extra steerage on this matter.

Fantasy: Everybody’s credit score rating is calculated in the identical approach.

Truth: Credit score scores have “scorecards” that categorize shoppers and rating them otherwise.

You already know that credit score scoring algorithms are extraordinarily advanced, however what many individuals don’t find out about is the “scorecards” or “buckets” inside every credit score scoring mannequin. These “buckets” consist of various classes of shoppers.

For instance, in response to John Ulzheimer, “There are scorecards for skinny recordsdata or these with few accounts, chapter, derogatories, and people with clear credit score recordsdata… Evaluating like populations provides this inhabitants a possibility to be thought-about based on [the] habits of that group somewhat than a comparability to a different, higher group.”

The credit score scoring formulation is completely different for every bucket. In different phrases, gadgets in your credit score report may be handled otherwise primarily based on which scorecard you fall into.

Generally your credit score rating modifications in a approach that you just don’t count on. For instance, maybe an inaccurate assortment account acquired deleted off of your credit score report and your rating went down, as an alternative of up. This might be since you modified scorecards because of the deletion, inflicting your credit score rating to be calculated another way. Basically, you would possibly now be on the backside of a distinct bucket as an alternative of on the prime of your earlier bucket.

It’s at all times good to maintain the idea of scorecards in thoughts, particularly when making an attempt to foretell any type of change to your credit score rating. You may by no means guess precisely how your rating will change due to all of the complexities and commerce secrets and techniques that go into credit score scores.

John Ulzheimer reveals how these buckets work in one in every of our Credit score Countdown movies on our YouTube channel!

Conclusions

Sadly, there are tons of credit score myths on the market, and believing them might lead you to mismanage your credit score and finally find yourself with poor credit score. We hope that this text helped to dispel lots of the misconceptions about credit score and helped you get began on the trail to raised credit score.

What credit score myths have you ever heard of? Did you beforehand imagine any of those? We’d love to listen to from you, so share your expertise with us within the feedback!

[ad_2]

Source link