[ad_1]

However the world of insurance coverage and its affect in your funds is usually murky. Though you possible know that you just want insurance coverage, understanding what varieties you want and what your protection choices are isn’t at all times minimize and dried.

Let’s take a more in-depth have a look at a number of the insurance coverage fundamentals that you need to know. Plus, we’ll make clear the distinction between a credit score rating and a credit-based insurance coverage rating.

How Insurance coverage Insurance policies Can Impression Your Credit score Rating

Earlier than we leap into the nitty gritty particulars, it’s vital to grasp how your insurance coverage insurance policies can affect your credit score rating. Though the impacts are oblique, making the connection between your insurance coverage insurance policies and credit score well being is useful when assessing your general monetary image.

As with most issues, the insurance coverage insurance policies you carry might need a constructive or damaging affect in your credit score rating.

Constructive Impression

You probably have an insurance coverage coverage with the suitable protection stage and deductible, you might be much less prone to resort to credit score. If you end up not relying closely on credit score to get via sticky conditions, that tends to have a constructive affect in your credit score rating.

For instance, let’s say that you’re carrying an auto insurance coverage coverage with $100,000 in legal responsibility protection, $50,000 in collision protection, and a $100 deductible. After an at-fault accident, you file a declare together with your insurance coverage firm. The insurer pays out the declare, leaving you with only a $100 deductible to cowl by yourself. Because you in all probability don’t have to show to a high-interest bank card to cowl this quantity, this insurance coverage coverage served to guard your credit score rating.

Unfavourable Impression

In case you don’t have sufficient protection or your deductible is simply too excessive, then an sudden occasion might derail your credit score rating. Relying too closely on credit score for emergency conditions might result in a downward credit score spiral.

For instance, let’s say that you’ve an auto insurance coverage coverage with $10,000 in legal responsibility protection, no collision protection, and a $2,000 deductible. After an at-fault accident, you’ll need to pay a $2,000 deductible earlier than the insurance coverage firm pays out a declare in your legal responsibility protection. Past the excessive deductible, you might be on the hook for automotive repairs with none help out of your insurance coverage firm. It’s simple to see how on this scenario you may get caught slapping these restore prices on a high-interest bank card, which could make it tough to get out of debt.

Credit score Scores vs. Credit score-Based mostly Insurance coverage Scores

When an insurance coverage firm is figuring out your premiums, they take a number of elements under consideration. Based on the Insurance coverage Info Insitute, auto insurance coverage insurance policies sometimes take your age, driving report, and zip code under consideration when figuring out your premium.

Your credit score historical past is one other issue that insurance coverage corporations typically consider. Nonetheless, insurance coverage corporations don’t use your common credit score rating. As a substitute, insurance coverage corporations in some states have a look at your credit-based insurance coverage rating when figuring out premiums.

A credit-based insurance coverage rating is completely different out of your common credit score rating. A credit-based insurance coverage rating is a three-digit quantity that’s calculated by the data in your credit score report. Though this insurance-related rating can also be primarily based in your credit score report and is usually known as an “insurance coverage credit score rating,” it’s not the identical factor as a daily credit score rating.

Right here’s a more in-depth have a look at what makes up your credit score rating versus what makes up your credit-based insurance coverage rating:

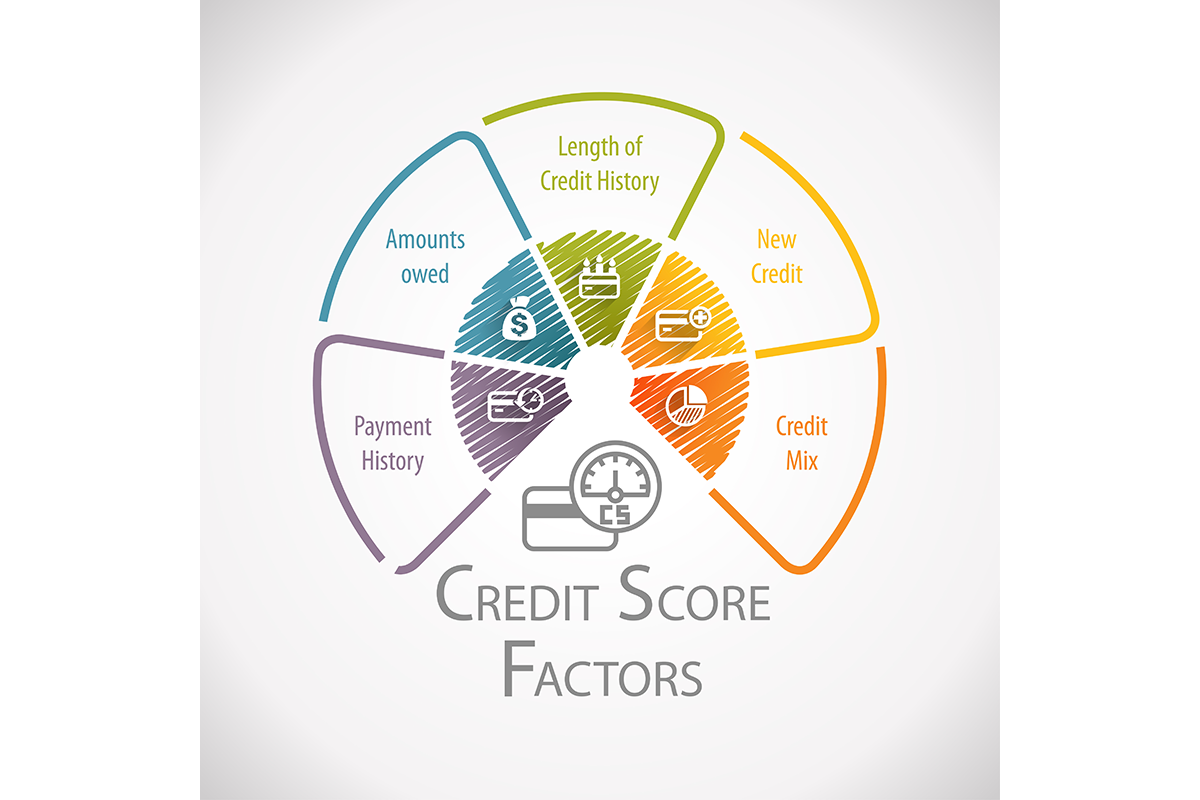

Credit score Scores![Credit scoring factors]()

FICO credit score scores, the model of credit score scores utilized by most lenders, are made up of 5 elements. Right here’s the breakdown:

- Fee historical past accounts for 35%: On-time funds have a constructive affect in your credit score rating.

- Debt accounts for 30%: Having an excessive amount of debt, significantly revolving debt, can have a damaging affect in your credit score rating.

- New credit score accounts for 10%: Once you apply for brand new credit score, you may see your rating dip.

- Size of credit score historical past accounts for 15%: You probably have accounts with longer ages, that has a constructive affect in your credit score rating.

- Credit score combine accounts for 10%: A mixture of various kinds of revolving credit score accounts and installment accounts can have a constructive affect in your credit score rating.

The FICO scoring mannequin makes use of the data in your credit score report and the scoring classes above to provide you with a three-digit credit score rating.

Credit score-based Insurance coverage Scores

Credit score-based insurance coverage scores are additionally made up of 5 elements. Right here’s the breakdown:

- Fee historical past accounts for 40%: On-time funds have a constructive affect in your insurance coverage rating.

- Debt accounts for 30%: Having an excessive amount of debt can have a damaging affect in your insurance coverage rating.

- New credit score accounts for 10%: Once you apply for brand new credit score, you may see your rating dip.

- Size of credit score historical past accounts for 15%: You probably have accounts with longer ages, that tends to have a constructive affect in your insurance coverage rating.

- Credit score combine accounts for five%: A mixture of revolving credit score accounts and installment accounts can have a constructive affect in your insurance coverage rating.

A credit-based insurance coverage rating additionally makes use of the data in your credit score report. However barely completely different priorities result in completely different scores.

Insurance coverage Insurance policies: The Fundamentals You Ought to Know

Relating to choosing out the suitable insurance coverage insurance policies, there are some primary components to concentrate on. After all, you’ll wish to begin your search with the suitable insurance coverage coverage varieties. However you’ll additionally want to pick the very best protection ranges and deductible quantities in your monetary scenario.

Let’s discover these insurance coverage fundamentals.

Premiums

Your insurance coverage premium is the quantity you pay in your insurance coverage coverage. You’ll have the choice to pay your premium month-to-month, yearly, or semi-annually. Sometimes, the extra protection and advantages you get out of your insurance coverage, the upper your premium might be.

Protection Ranges

The best protection ranges could make all of the distinction. With out the suitable stage of protection, you may get caught footing the invoice after an sudden occasion. For instance, signing up for an auto insurance coverage coverage with a minimal quantity of legal responsibility protection might imply you’ll find yourself paying for a portion of a authorized battle out of pocket after an at-fault accident.

You probably have substantial belongings, it’s particularly vital to be sure you have sufficient insurance coverage. In any other case, your belongings may very well be in danger. One approach to discover the suitable protection stage is to speak to a monetary advisor or insurance coverage agent. With their experience, you may be sure you aren’t skimping on protection.

Deductibles

A deductible is the quantity you’ll need to pay out of pocket earlier than an insurance coverage firm pays out the remainder of your declare.

For instance, let’s say you have got an auto insurance coverage coverage with a $500 deductible. After an accident, you file a declare for $2,000 price of injury. With that, you’ll have to pay a $500 deductible earlier than the insurance coverage firm pays for the remaining damages.

Generally, a better deductible results in a extra inexpensive insurance coverage premium. Though it’s tempting to boost your deductible in pursuit of financial savings, don’t elevate it too excessive. It’s vital to decide on a deductible you may moderately cowl. In any other case, you may get caught in a scenario that pushes you right into a cycle of high-interest debt.

Forms of Insurance coverage

Some sorts of insurance coverage are pretty apparent. However a number of the insurance coverage insurance policies you may want aren’t essentially an apparent selection. Right here’s a more in-depth have a look at a number of the most vital sorts of insurance coverage:

Auto Insurance coverage

It’s unlawful to drive with out auto insurance coverage in most states. However even when driving with out insurance coverage was authorized, it’s possible not a threat you wish to take. As a driver, you have got a number of insurance coverage coverage choices. A couple of embrace:

- Legal responsibility protection: In case you trigger property harm or harm to a different individual, legal responsibility protection will kick in. Nonetheless, a liability-only coverage is not going to cowl any restore prices in your personal automobile.

- Collision protection: In case you get into an accident, collision protection will assist pay for restore or substitute prices.

- Complete protection: Complete protection pays to restore or change your automobile after a lined occasion. A number of the lined occasions might embrace vandalism, hearth, hail, floods, and theft.

- Uninsured and underinsured motorist protection: This protection applies for those who get into an accident with a driver who doesn’t have sufficient insurance coverage to cowl your restore or medical prices.

Though legal responsibility protection is the one required protection in most states, choosing extra in depth protection can higher defend your pockets if an accident happens.

Householders Insurance coverage

As a house owner with a mortgage, you might be possible required to pay for any such insurance coverage. However even householders with a free and clear residence will possible select to guard their property with any such insurance coverage.

- Dwelling protection: If one thing occurs to your private home, like a fireplace or vandalism, any such protection would pay to restore or rebuild the constructing.

- Private property protection: The sort of protection protects the belongings within your private home. For instance, a coverage may cowl substitute prices in your furnishings.

- Legal responsibility protection: If somebody will get damage in your property, this protection would pay for his or her medical payments and your authorized charges.

Renters Insurance coverage

You don’t have to personal a house to get renters insurance coverage. With renters insurance coverage, you will get protection for the fee to interchange your belongings. For instance, renters insurance coverage can assist you pay to interchange your electronics after a theft.

Umbrella Insurance coverage

Umbrella insurance coverage gives additional legal responsibility protection in your belongings. You possibly can consider any such insurance coverage as an additional layer of safety. However you could have an underlying householders, auto, or renters coverage. If somebody sues you for greater than the coverage limits of the underlying account, your umbrella protection will step in.

Life Insurance coverage

Life insurance coverage presents a approach to change your revenue for those who cross away unexpectedly. This can assist defend your dependents from monetary catastrophe if the unthinkable occurs.

- Time period life insurance coverage: Time period insurance coverage includes buying a coverage for a set variety of years. For instance, you should purchase a 15-year coverage. After the 15-year time period, your dependents are now not lined. However at that time, you might need saved sufficient to guard them with out an insurance coverage coverage.

- Entire life insurance coverage: Entire life insurance coverage protects your dependents in your whole life. Once you cross away, your dependents will obtain a demise profit and the money worth of the investments tied into this coverage.

Well being Insurance coverage

Medical health insurance can defend your funds from sudden medical payments. Some can get this coverage via an employer-sponsored healthcare plan. However others receive protection via the federal market.

For these going through unaffordable premiums, think about a better deductible well being plan. Though the upper deductible isn’t ideally suited, it nonetheless presents some safety within the occasion of a significant medical emergency.

Incapacity Insurance coverage

In case you develop into disabled and can’t work anymore, incapacity insurance coverage protects your revenue. Sometimes, these insurance policies change between 40% to 70% of your base revenue. In case you are involved about surviving with out your main revenue, incapacity insurance coverage is a worthwhile possibility to think about.

Lengthy-term Care Insurance coverage

Lengthy-term care can contain getting help with on a regular basis duties or staying at a nursing residence for an prolonged time frame. Many seniors want this help, nevertheless it’s not low cost. Lengthy-term care insurance coverage presents a approach to cowl these prices. Sometimes, shopping for any such insurance coverage in your 50s or 60s is essentially the most cost-effective as a result of your premiums will improve as you age.

Regularly Requested Questions

What are 2 issues you are able to do to guard your credit score rating?

Relating to defending your credit score rating, there are many choices. Two of the simplest options embrace paying your payments on time and paying off debt.

Does insurance coverage credit score rating have an effect on credit score rating?

In some states, insurance coverage corporations can use an insurance-based credit score rating when figuring out your premiums. The rating takes the small print of your credit score report under consideration. Nonetheless, your credit score rating shouldn’t be impacted with an insurance coverage firm requests your credit-based insurance coverage rating.

Does canceling insurance coverage have an effect on credit score?

An insurance coverage coverage isn’t a credit score account. With that, canceling an insurance coverage coverage received’t immediately affect your credit score rating.

The Backside Line

It’s vital to lock in the suitable insurance coverage insurance policies. In any other case, your protection may not go so far as you want it to while you file a declare. Take a while to discover your entire insurance coverage choices. You probably have questions on your particular insurance coverage wants, don’t be afraid to speak over the small print with a monetary skilled or insurance coverage agent.

[ad_2]

Source link