[ad_1]

As we realized within the earlier weblog transaction analytics is a robust device reshaping the banking {industry}. We delved into the idea of transaction analytics, its significance, and the way it gives a 360-degree view of buyer conduct and preferences. Right this moment, we’ll dive deeper into the sensible functions of transaction analytics in banking and the way it can revolutionize decision-making throughout the lending lifecycle.

Originations – Saying “YES” to extra prospects with a greater and extra appropriate supply.

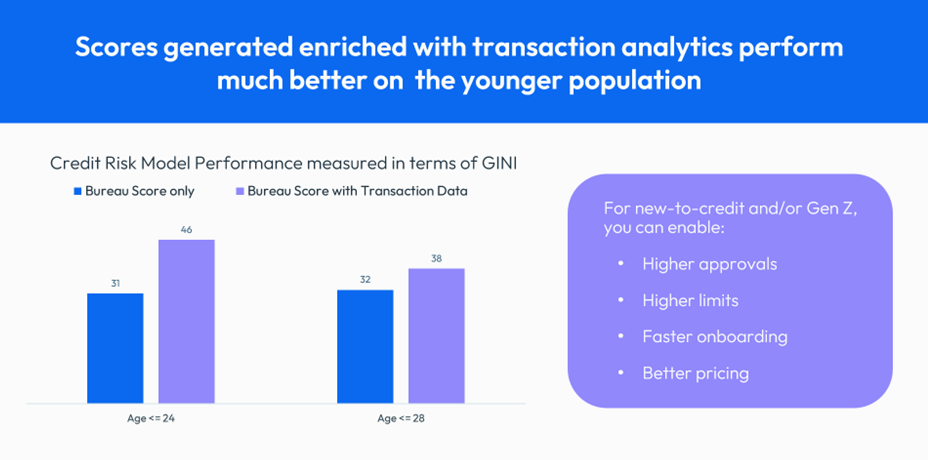

Primarily based on our intensive expertise in delivering quite a few transaction analytics initiatives, we have noticed that credit score scoring frameworks pushed by transaction knowledge present a considerable uplift in GINI scores, starting from 8% to 18%, relying on the inhabitants phase.

GINI coefficient measures the accuracy of a credit score danger evaluation mannequin in screening high-risk prospects and low-risk prospects. A better GINI signifies a more practical credit score danger mannequin, with banks having the ability to tailor therapies and choices primarily based on the client’s danger stage.

Transaction analytics additionally gives the power to attain prospects who’re new to credit score enabling higher gives for the shoppers and sooner onboarding.

A extra correct credit score scoring mannequin ends in elevated approval charges with out an related enhance in danger. This implies banks can approve extra buyer loans. The benefit extends to scoreability as effectively.

Many purchasers who’re absent from credit score bureau data or have minimal illustration can now obtain a credit score rating, enabling credit score underwriting. Moreover, credit score scores derived from transaction knowledge outperform these primarily based solely on bureau knowledge, notably for younger prospects.

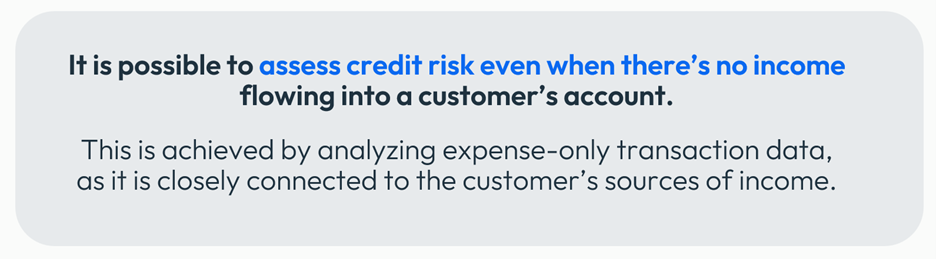

Furthermore, financial institution accounts with no verified proof of earnings however full expense data can nonetheless be used to foretell outcomes and generate a sturdy credit score rating.

It’s because a buyer’s spending conduct is carefully tied to their earnings, and any modifications in earnings are mirrored of their bills. That is notably related when employers can not straight deposit earnings into their workers’ accounts, and workers deposit their earnings themselves to allow digital spending by means of on-line banking or smartphone funds.

Enabling deeper buyer relationships and driving buyer loyalty

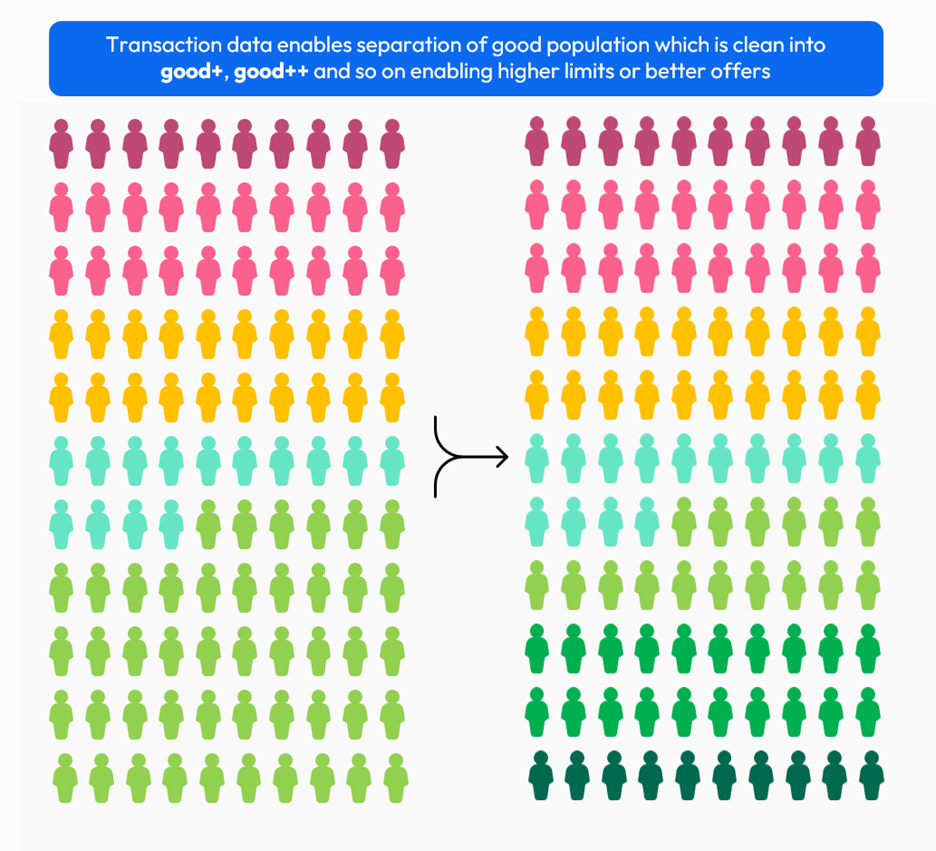

Transaction knowledge gives profound insights into buyer conduct, enabling higher buyer differentiation and the supply of extremely customized gives that foster stronger buyer relationships. For example, transaction knowledge, when built-in into cross-selling methods, can supply evaluation to distinguish buyer varieties.

Distinguishing between good prospects, who make up the bulk, and tailoring differentiated gives utilizing conventional knowledge parts will be difficult. Nevertheless, transaction knowledge makes this differentiation potential, leading to improved buyer experiences, decreased churn, and elevated loyalty. In our expertise, we have recognized a definite phase comprising 8% to 13% of the great inhabitants, which was beforehand difficult to establish. This has enabled the implementation of extra customized gives and enhanced buyer journeys for this particular group.

Defending buyer vulnerabilities and lowering the price of collections

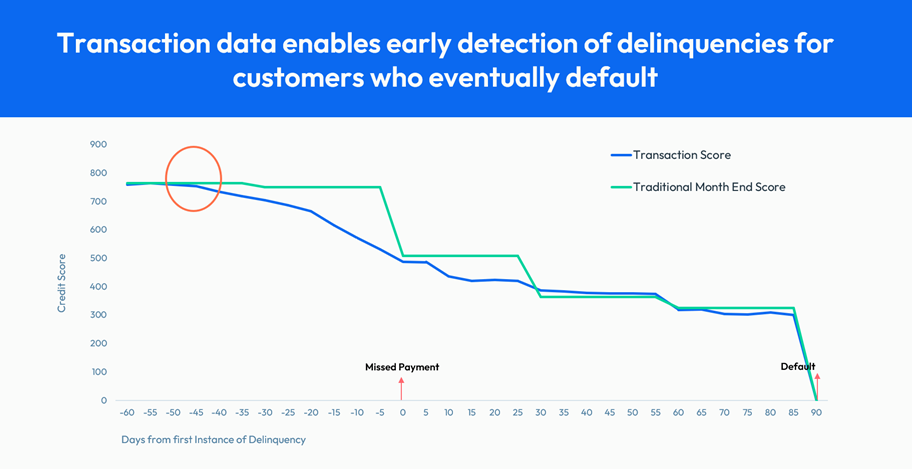

Transaction knowledge’s real-time nature empowers banks to proactively monitor prospects, permitting for intervention in case of any points with a buyer’s profile.

In a number of eventualities, we have noticed that transaction data-driven buyer scores can detect profile points at the very least 40 days earlier than prospects grow to be delinquent. This gives banks with alternatives to intervene and help prospects a lot earlier, enhancing the client expertise and resulting in a better Internet Promoter Rating (NPS) for the financial institution.

Transaction knowledge additionally optimizes collections operations by providing higher buyer segmentation, leading to extra tailor-made and environment friendly assortment therapies.

As we have mentioned, AI-powered transaction analytics is a potent device within the banking {industry}’s mission to serve underbanked and unbanked market segments. By facilitating extra knowledgeable credit score choices, enabling sooner buyer onboarding, delivering hyper-personalization of companies, pricing with confidence, and assigning optimum mortgage quantities, transaction analytics has the potential to remodel the banking panorama.

By efficient transaction analytics methods, the period of one-size-fits-all banking options is quickly giving strategy to hyper-personalized companies pushed by a profound understanding of every buyer’s particular person spending habits, earnings patterns, and monetary objectives. This granular understanding empowers banks to supply tailor-made monetary options and well timed functions, in the end resulting in improved buyer outcomes throughout the lifecycle.

How FICO Can Assist You Harness the Energy of Transaction Analytics:

FICO’s transaction analytics is powered by FICO Platform integrating our proprietary mannequin, the place we use patented characteristic technology expertise and a multi-model method. It follows the identical blueprint design as most of FICO’s industry-level scoring initiatives.

Transaction analytics powered by FICO Platform are versatile and modular – which means they are often lifted, personalized, reused for brand spanking new use circumstances or functions with minimal rework.

With this state-of-the-art framework, monetary establishments are empowered with a centralized decisioning platform to generate actionable insights from transaction knowledge that seamlessly analyze and combine the insights into lending choices throughout the client lifecycle.

Able to take the subsequent step? Contact us to debate extra.

Additionally,

[ad_2]

Source link