[ad_1]

Final Automobile Fee

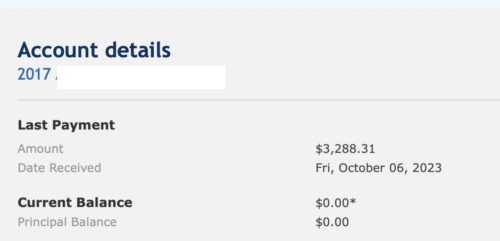

Guess what, pals! I did a factor! In a single fell swoop, I paid off my 2017 automobile mortgage. My stability is now $0!

That is my large win to report, as this was my solely “shopper debt.” My solely remaining money owed are for my scholar loans and our mortgage.

Scholar Mortgage Drama

I’ve talked about earlier than that I’m placing my scholar loans on the again burner. Whereas I’ll be making month-to-month funds towards my loans as required, I’m not planning to place something “further” in the direction of them proper now. As a substitute, I’m formally enrolled in PSLF and plan to experience that out till my remaining loans are forgiven. That mentioned, the federal government and mortgage service suppliers have made the method “clear as mud.” Final time I discussed my scholar loans again in February, I reported that the net platform indicated I had 44 qualifying funds to go.

One way or the other, as we speak, I logged in and see that 2 of my loans point out solely 15 funds remaining….whereas 2 of my loans present 0 eligible funds (thus, 120 funds to go). Like….what? Completely nothing has modified within the interim between February and now, so I don’t know why the net platform is telling me such disparate info. It can’t be correct. I referred to as my service supplier, Mohela, to attempt to discuss to a customer support rep and gave up after a full hour on maintain as a result of I had a gathering I needed to soar into.

I just about detest these loans and allllll the curiosity I’ve already paid. And the servicers don’t make it simple to get info. Lengthy wait instances, rampant misinformation, and so forth. Ick. Sadly, that is one thing I’ll must deal with one other day. Transferring on…..

New Monetary Targets

Once we had our espresso date, I discussed being uncertain easy methods to proceed after my automobile is paid in full. This can be a “running a blog away debt” weblog. However I’m now feeling my priorities shift extra towards saving and investing. My husband and I do pay further on our mortgage, however not with the steadfast dedication with which I paid off my automobile.

As a substitute, I’m serious about shifting to extra financial savings/funding choices. My open enrollment interval opens very quickly. I’d like to extend my financial savings/investments in a number of classes. Listed here are my ideas:

| CURRENT in 2023 | NEW for 2024 |

|---|---|

| HSA: $5500/12 months | HSA: $7750/12 months |

| FSA: $700/12 months | FSA: $1000/12 months |

| 403B: $125/verify | 403B: $175/verify |

| 529: $50/youngster/month | 529: $60/youngster/month |

If I’m doing my math proper, the whole quantity of investments yearly from this desk would quantity to $14,740 (FYI: I’m paid biweekly. I’ve 2 children, and every has their very own 529).

That additionally doesn’t embody my regular retirement investments. By default, I make investments 7% of my wage towards retirement, which is matched by my employer dollar-for-dollar for the complete 7%. In different phrases, I’ve 14% of my wage mechanically invested into retirement (my husband has the same scenario along with his wage, too). Then I’m proposing an extra $15,000/12 months in investments and financial savings unfold amongst HSA, FSA, 529, and 403B.

This transformation is approx. $4,000/12 months increased than my contributions for 2023. A distinction of $153/paycheck. However is that sufficient? Or ought to I be aiming to extend this much more?

Pulled in 1,000,000 instructions

I’ve a number of different shorter-term financial savings presently saved in CapitalOne360 financial savings accounts. By nature, I’m a “splitter” versus a “lumper” relating to financial savings. This is the reason I’ve completely different financial savings accounts for thus many alternative issues. At the moment, I’ve financial savings accounts for:

- scholar mortgage financial savings. My authentic plan was to save lots of a bit of every month till I’ve sufficient to repay one of many 4 scholar loans in full. However I simply dipped into this financial savings to assist cowl the overage from my automobile fee. Additionally, I’m unsure if I even wish to pay “further” to my scholar loans….

- automobile repairs or new automobile

- emergency fund

- journey/Christmas/enjoyable. I save a bit of every month so I can at all times pay money for something “large” or “further” we would do as a household. That is principally used for journey, however might be used to assist fund Christmas presents and experiences, or something that may be over and above to the place it will blow the month-to-month funds… I’ve a financial savings only for that!

- annual charges. Examples: life insurance coverage, automobile insurance coverage (paid bi-annually), HOA (paid quarterly), and so forth.

In spite of everything my current house repairs, of us have additionally urged budgeting and saving particularly for house repairs, in order that may be an account so as to add (or possibly change my scholar mortgage financial savings to “house restore” financial savings…..)

One other thought I’m contemplating is to open a cash market account – one thing that’s not essentially long-term financial savings, however one thing that can yield the next rate of interest than my present financial savings. Whereas this may be impractical for the annual charges I frequently use-and-restock, it would work nice for issues just like the Emergency Fund and New Automobile financial savings. Sure, I do know I actually simply paid off my car. And I plan to maintain it for fairly awhile. However I’d LOVE to have the ability to purchase my subsequent automobile in 5-ish years with money absolutely debt-free! That appears higher stored in a cash market vs financial savings account.

This mentioned, I truthfully don’t know the place to begin! I’ve by no means had a cash market account earlier than. Solely retirement accounts, the funding automobiles listed above (e.g., HSA, FSA, and so forth.) and regular outdated financial savings accounts. I’d need one with low-to-no charges, however an honest price of return. Any suggestions? I’ve longer-term (retirement) investments with Constancy and Vanguard already. Ought to I see about opening up a Cash Market account?

What are your ideas? What ought to be my subsequent large aim or focus for financial savings and short- and long-term investments?

The put up Automobile Paid Off and New Monetary Targets appeared first on Running a blog Away Debt.

[ad_2]

Source link