[ad_1]

In our first weblog submit on the New York and New York Metropolis’s proposed amendments to their debt assortment legal guidelines, we explored the proposed amendments and the choice opt-out legal guidelines within the federal Honest Debt Assortment Practices Act (FDCPA) and the Washington, DC debt assortment modification that obtain the identical aims with out the unintended penalties. On this half two, we discover the advantages of digital communications for shoppers in all different states and jurisdictions—besides New York—in addition to these unintended penalties New Yorkers face from these potential amendments.

For the reason that New York Division of Monetary Companies (NYDFS) remains to be contemplating the feedback obtained to their proposed adjustments and the New York Metropolis Division of Client and Employee Safety remark interval is open till November 29, 2023, there may be nonetheless time for these Departments to revise their proposals to match the federal legislation or Washington DC’s legislation. Each the federal and DC legal guidelines allow debt collectors to speak digitally a few client’s account so long as the digital communications comprise clear and conspicuous opt-out language with strict penalties for failing to abide by the opt-out provisions. Washington, DC goes a step additional and restricts digital communications to 1 per week until a client opts in to extra digital communications in a seven day interval.

Each NYDFS and NY ought to enable their shoppers to have the identical expertise because the shoppers in the remainder of the nation.

Digital Communication Advantages Customers, Collectors, and Collectors

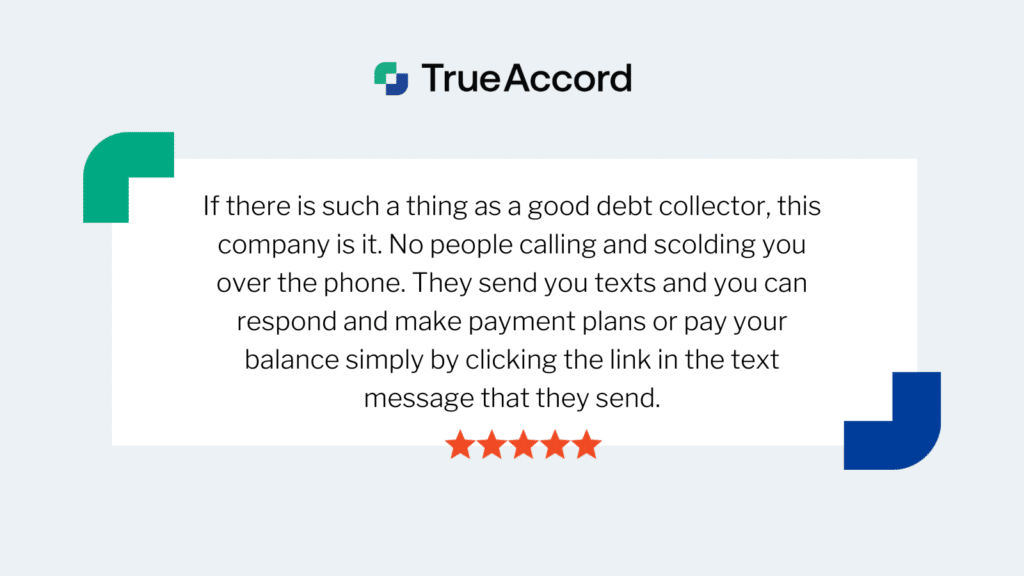

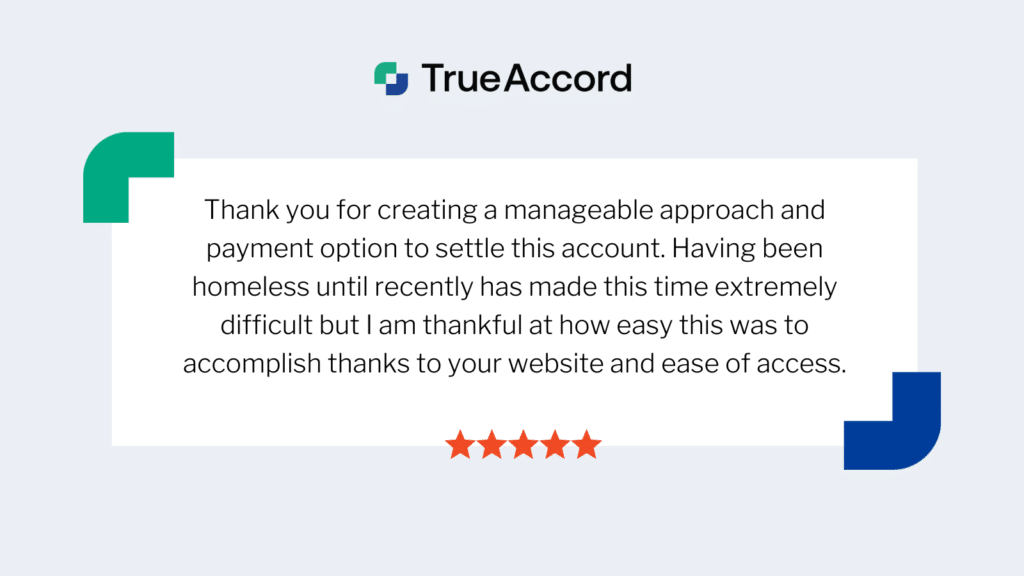

TrueAccord is aware of digital communication advantages shoppers, as evidenced by numerous shoppers who’ve offered suggestions (both immediately or on-line) all through our years in enterprise, like this client who wrote in July 2023:

Digital Communications are a Step Ahead in Client Safety

Digital communications are simply managed by shoppers and tightly managed by service suppliers with inbuilt mechanisms to stop harassment. These strategies already present superior client protections than telephone calls and letters for a number of causes:

- All digital communications are written, documented, and will be searched, mechanically making a paper path of communication between the patron and the collector.

- Digital communications supply considerably higher safety from undesirable or harassing communication in comparison with telephone calls and letters. Customers maintain the ability and might simply choose out of digital communication by clicking “unsubscribe,” marking emails as spam, replying STOP to a SMS, or blocking a quantity solely from their system.

- Service suppliers carefully monitor inbound communications and people senders who seem like mass advertising are sometimes blocked from supply altogether within the spam filters for each e-mail and SMS. Sadly for licensed companies, like legislation abiding debt collectors who’ve a legit motive for these digital communications, their digital communications could by no means attain a client’s telephone or inbox with no very subtle supply technique that takes into consideration frequency.

Moreover, e-mail is designed to journey with a client perpetually, whereas addresses and oftentimes telephone numbers can change. Electronic mail addresses will not be ever reassigned by service suppliers. If shoppers steadily change addresses, like army households, e-mail could also be one of the best channel to make use of to speak because it lowers the chance of missed communication when shoppers neglect to replace their account info with their new bodily deal with.

Customers Choose Digital Debt Assortment

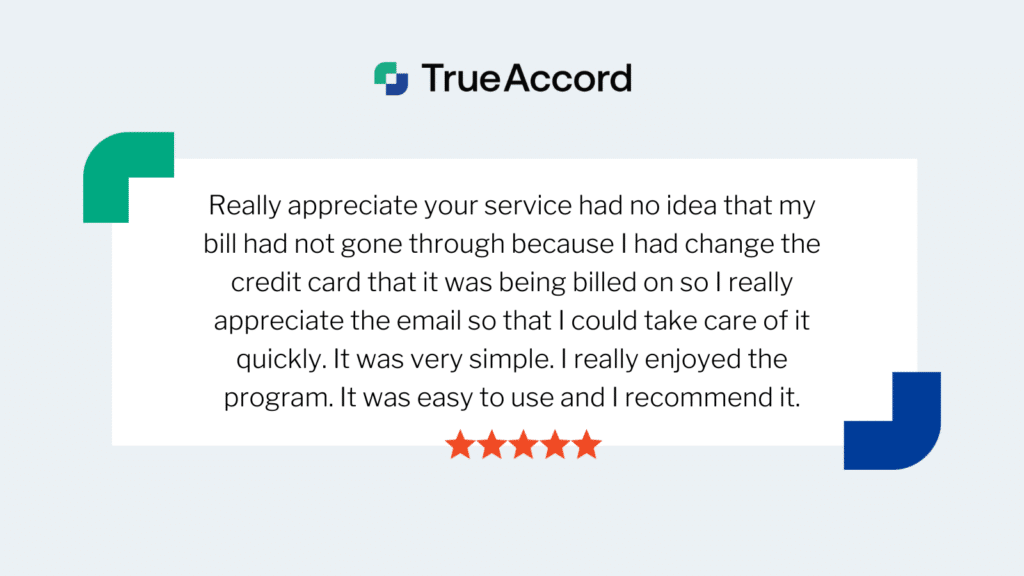

By and enormous, shoppers favor to speak with their assortment companies digitally—they already predominantly talk with their banks, collectors, and lenders digitally, so digital assortment is a clean transition when an account strikes to assortment. As this client reported simply this previous August 2023:

Virtually all TrueAccord communications with shoppers (96%) occur electronically with no agent interplay. That is doable as a result of our digital communications comprise hyperlinks to on-line pages the place shoppers can take motion on their accounts. In reality, greater than 21% of shoppers resolve their accounts outdoors of typical enterprise hours—earlier than 8AM and after 9PM—when name facilities are closed and it’s presumed inconvenient to contact shoppers underneath the FDCPA.

Customers Ought to Not Should Choose-In to Digital Communications Twice

Customers already choose in and talk by means of primarily digital channels with their collectors. Requiring shoppers who’ve already opted in to must once more choose in to digital communications with a view to focus on the identical account with a group company provides burden to shoppers. When a client offers their digital contact info (e-mail deal with or mobile phone quantity) to the creditor, there ought to be little doubt that the patron wishes to speak electronically. If the patron doesn’t, they will unsubscribe or choose out from persevering with to obtain messages by means of these channels.

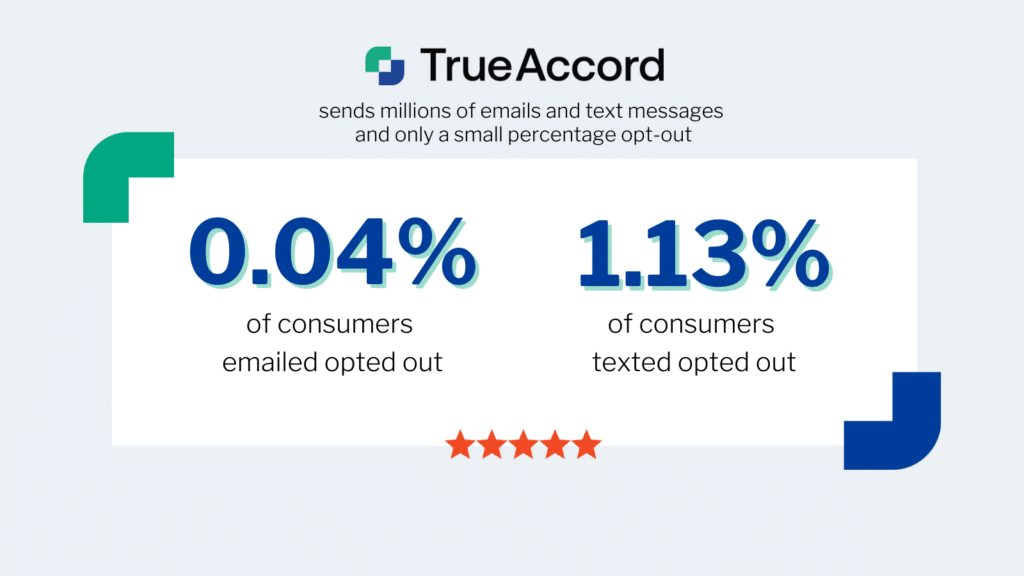

Customers are acquainted with opt-out strategies corresponding to the usual unsubscribe hyperlink in emails and the phrase “Reply STOP to opt-out” in textual content messages, as they do from all different undesirable communications in different industries. Not solely can shoppers opt-out from digital communications by merely replying cease to a textual content or clicking twice to unsubscribe, at TrueAccord shoppers can even reply to any digital communication, telephone into the workplace or ship us a letter. Even with the a number of choices and ease of choose out, few shoppers unsubscribe. Of the hundreds of thousands of e-mail communications TrueAccord sends, solely 0.04% of shoppers unsubscribe, most utilizing the unsubscribe hyperlink offered within the e-mail. And out of the hundreds of thousands of textual content messages we ship, all textual content messages comprise the phrase “Reply STOP to opt-out,” and on common just one.13% of shoppers reply cease.

It’s a requirement of the FDCPA to incorporate a transparent and conspicuous technique to choose out of digital communication. Moreover, failure to honor a request to cease speaking in a specific channel is a violation of the legislation topic to fines that embrace lawyer’s charges. As well as, shoppers count on a straightforward solution to choose out, if that choice just isn’t obtainable in digital communications (not solely is it a violation of the legislation) however shoppers can simply as simply report the communication as spam which can outcome within the incapability of the debt collector to ship digital messages. All of those protections, together with the clear client desire for digital (partly demonstrated by their low choose out charge), negates the necessity to change the expertise to 1 the place the patron has to take steps to telephone in to consent earlier than any digital communications will be despatched notifying the patron of their account in collections as would be the case if the NY and NYC amendments take impact.

Unintended Harms to Customers if Digital Communications are Restricted

Limiting Digital Communication Use Hurts All Customers

Requiring particular consent for e-mail, textual content messaging, or different digital channels, when no such consent is required for calls and letters, hurts shoppers by growing undesirable calls and litigation danger. The proposed adjustments would require debt collectors to seize consent from shoppers immediately, even when shoppers already opted in to textual content and emails about their account with their collectors. Which means a debt collector can’t textual content or e-mail to tell the patron about their account being in assortment, present them with a discover of their rights, and element doable subsequent steps (the quickest, least bothersome strategies of communication).

As a substitute, debt collectors should mail shoppers letters and shoppers should affirmatively reply to these letters by calling into the workplace (one thing that should be accomplished throughout working hours versus digital communications that may be explored at any handy time for shoppers). This stifles the circulation of knowledge that helps shoppers make knowledgeable choices about their funds and concurrently helps collectors make knowledgeable selections about restoration choices and future lending methods. In spite of everything, we all know busy shoppers usually don’t reply to outbound letters.

If shoppers don’t reply, then debt collectors place outbound calls—which we additionally know is not shoppers’ most most well-liked technique of communication—till they get the patron on the telephone to debate their account and seize the direct consent that can be required if the NYC proposal takes impact.

When a debt collector can’t attain a client to speak about their debt the creditor is pressured to make troublesome choices about the best way to get well, absent an understanding of why a client just isn’t reaching out. This features a choice about whether or not or to not file a lawsuit to get well the debt (which, if profitable, ends in garnishment of a client’s paycheck or a lien in opposition to a client’s property).

In some situations the place a client may not personal property or be employed, a creditor could not file a lawsuit however merely settle for the loss. This choice can have damaging impacts on all shoppers: sooner or later it is going to be harder or unattainable to obtain entry to credit score, not just for the person client who was unable to repay the debt however for others shoppers which have poor credit score historical past or no credit score historical past, as lenders grow to be much less more likely to take dangers when there’s a decrease likelihood of restoration. Moreover, and relying on the extent of their loss, lenders could select to lift rates of interest and APRs impacting all shoppers to finally cowl these losses.

Non-Digital Communications Can Be Disruptive to Customers

Customers use the web, cellular gadgets, and their emails for communication, buying, and monetary transactions. When a buyer defaults on their account, it’s a disruption to their lives to instantly obtain telephone calls and letters relating to an account for which they beforehand solely communicated through digital channels. A lot of TrueAccord’s creditor-clients, involved about their client expertise and their model picture, favor a seamless transition to debt assortment communications and prohibit TrueAccord from making any outbound calls or sending letters on their accounts as a result of their prospects have solely ever interacted digitally.

This method has confirmed to learn the shoppers that need assistance essentially the most, as one buyer defined to us in February, 2023:

[ad_2]

Source link

:max_bytes(150000):strip_icc()/GettyImages-849197544-6c2b33925d2743f68903455679f52482.jpg)