[ad_1]

Monetary instability and uncertainty are information of life these days that all of us need to navigate as greatest we will. It’s the identical for lenders. Turkey is among the nations with essentially the most difficult economies on this planet as a result of its geopolitical state of affairs and present inflation.

There is no such thing as a actual blueprint for the way banks ought to handle by means of instances like this. However in reviewing the challenges available in the market immediately, we will recommend some avenues for improved development and profitability.

Turkish Challenges: Inflation, Dangerous Debt and Laws

First, as in any economic system with excessive inflation ranges, the banks are seeing slowing mortgage development and rising dangerous money owed throughout the nation, that are impacting income and capital. With inflation charges at better than 60%, Turkish banks and customers are going through a harder time with ranges anticipated to cut back over the subsequent two years however nonetheless anticipated to be 14% (supply: The Central Financial institution of the Republic of Türkiye). With the present curiosity base price of 40%, the banks are having to consistently revise their financial savings charges for each Turkish lira and overseas foreign money deposits, to reply to aggressive pressures; they’re additionally revising their retail lending technique and actions close to present limitations set by the Central Financial institution.

The second problem is the consistently altering regulatory surroundings. Within the final 12 months there have been extra modifications than within the earlier 5 years. Banks are actually struggling to implement and measure the impression of such laws on their portfolio in restricted time.

Responses: The Judgmental Method

Given these circumstances and challenges, what are banks to do?

For lending selections, you may handle your coverage guidelines and modify scorecard cut-offs. You can herald some new insurance policies that assist to handle the issues during the interval of uncertainty. The coverage guidelines would seemingly be judgemental guidelines based mostly on the circumstances, versus empirically derived. Equally, any modifications to the rating cut-offs may very well be based mostly on earlier expertise solely moderately than current knowledge.

Given the fast market modifications, it might make sense to rebuild your credit score fashions, however having to attend for ample knowledge won’t be acceptable.

For deposits pricing, you might comply with the competitors, which is a standard follow in numerous markets, if charges are clear.

Responses: Simulation and Optimisation

To handle the state of affairs with a extra sturdy and efficient resolution, banks might use optimisation, which permits enterprise customers the power to discover all the many and numerous potential methods inside the choice area. The person can see forecasts based mostly on enterprise as standard to see what is anticipated to occur, after which create situations that take a look at numerous “what if” situations. These “what ifs” leverage the underlying choice impression mannequin that brings collectively a sequence of fashions that mirror the important thing parts of the choice.

Let’s say, I’m the Head of Retail Lending and I wish to understand how I ought to change my choice methods to cut back losses whereas retaining as a lot quantity as potential. I can use simulation to see what my present choice technique will obtain. I can then run a sequence of simulations to discover numerous choices. Moreover, I can run optimisations the place I set a selected set of targets and constraints — similar to a quantity objective with constraints on losses and revenue — to create numerous choices for the enterprise to think about. I may stress-test the situations, enabling me to see how the situation may honest beneath quite a lot of circumstances, similar to growing loss charges.

We regularly hear that constraints, similar to limitations on rates of interest, are purpose sufficient to not use optimisation and AI to plot new methods. Quite the opposite, these constraints make optimisation much more necessary. In a closely regulated and extremely aggressive market, it’s essential to have the perfect instruments potential to set charges and choice methods to make sure you could compete successfully and never lag your competitors.

The Benefits of Optimisation and Simulation

FICO’s optimisation and simulation capabilities permit banks to not solely perceive the artwork of the potential however to stress-test the choice situations beneath quite a lot of circumstances previous to deployment. Moreover, these capabilities present insights into the price of constraints, which allows banks to find out when insurance policies needs to be modified. In an surroundings with consistently altering regulation, banks want a device to completely perceive the enterprise impression of those modifications and the choices open to them.

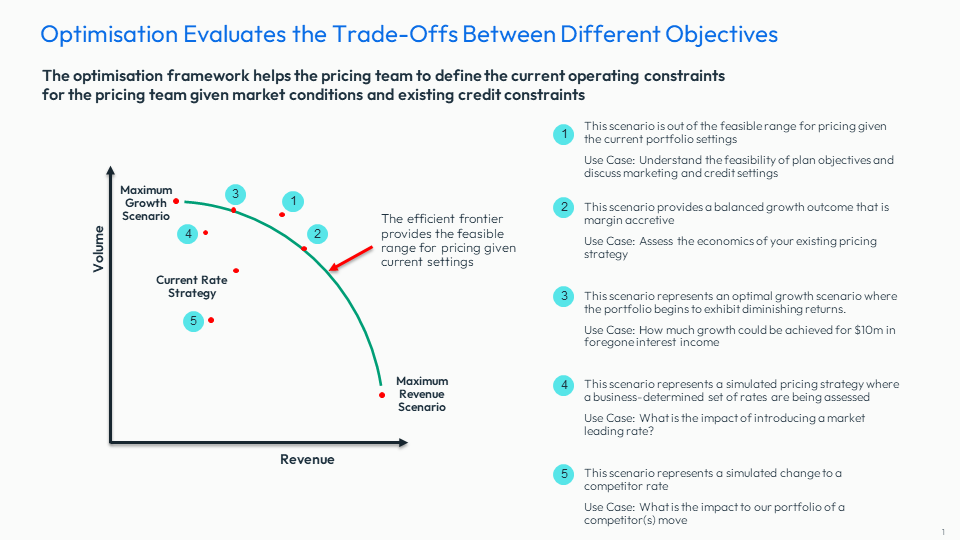

Within the graphic under you may see how the answer gives the power to evaluation different methods in comparison with enterprise as standard.

Optimisation provides you the power to be extra agile when it comes to discovering higher choice methods. One other key element is the power to ship these methods to your operational surroundings, as no fashions or choice methods are helpful in the event that they can’t be deployed in a well timed method. Quick and agile deployment is essential in a fast-changing market. The pliability of the optimisation resolution ensures that the hassle concerned in deployment is minimized, no matter the technique format required.

One of many key causes that optimisation is profitable is that every space of the Financial institution can clearly perceive the seemingly impression of the brand new choice technique. Finance, Advertising, Threat, Product and senior administration can all come collectively to know the impacts on every of their areas and agree upon a standard set of metrics, in addition to perceive the trade-offs between numerous FPIs.

Optimisation expertise doesn’t trigger uncertainty to vanish, nevertheless it does present customers with a set of extremely efficient instruments and strategies for managing it. Situation planning capabilities and the power to stress-test macroeconomic and aggressive assumptions are essential in permitting enterprise customers to plan for the unknown. Efficient optimisation instruments additionally permit for well timed refreshes of value sensitivity fashions, essential in enabling take a look at and be taught in a altering macroeconomic surroundings.

One current success story in Turkey is Akbank, which has deployed its first optimisation mission for managing bank card limits within the present financial local weather whereas complying with rigorous nationwide legal guidelines round credit score gives. The usage of FICO prescriptive analytics for bank card portfolio optimization allowed the financial institution to develop approvals by 45 % and limits by 60 %. You may learn extra about this, right here: https://www.fico.com/blogs/credit-card-portfolio-optimization.

By intervals of financial instability, simulation and optimization have confirmed to be indispensable strategies to banks, offering the perception and agility essential to steer an efficient plan of action by means of uncharted territory.

Be taught Extra About Optimisation’s Prospects

[ad_2]

Source link