[ad_1]

In 2020, FICO, the corporate behind the FICO credit score scores, launched the most recent fashions of their line of credit score scoring algorithms: the FICO Rating 10 and the FICO Rating 10 T.

In 2020, FICO, the corporate behind the FICO credit score scores, launched the most recent fashions of their line of credit score scoring algorithms: the FICO Rating 10 and the FICO Rating 10 T.

The “T” within the latter scoring mannequin stands for “trended,” which displays the incorporation of trended information—your credit score information over time—into the algorithm.

Thanks not solely to the inclusion of trended information but in addition a number of different main adjustments, the corporate claims that the brand new scoring fashions are superior to all earlier FICO scores.

Though nearly all of shoppers should not more likely to see a dramatic change of their credit score scores, some teams of shoppers could expertise extra excessive shifts. Finally, the brand new FICO scores are predicted to widen the hole between shoppers with good credit score versus these with a bad credit score.

Nonetheless, the widespread implementation of FICO 10 and 10 T is probably going nonetheless a number of years away.

Hold studying to get all of the info on FICO 10, together with what makes it completely different from earlier FICO rating variations, the affect it’s going to have on credit score scores, and once we will begin to see lenders adopting it. Most significantly, we’ll inform you methods to get credit score rating with FICO 10.

Why Did FICO Come Out With a New Credit score Scoring Mannequin?

The aim of a credit score rating is to speak a shopper’s degree of credit score threat to lenders in order that lenders could make much less dangerous choices when granting credit score. Lenders need to keep away from extending credit score to debtors who’re more likely to default on a mortgage as a result of defaults characterize losses for the corporate.

So, the extra correct a credit score scoring mannequin is at predicting shopper credit score threat, the extra helpful it’s to lenders. With a predictive credit score scoring mannequin, lenders could make extra knowledgeable lending choices, which helps their backside line.

For that reason, the purpose of every new credit score rating is to make it higher than the final model at predicting credit score threat, and that’s precisely what FICO 10 is designed to do.

Shopper Debt Is on the Rise—However So Are Credit score Scores

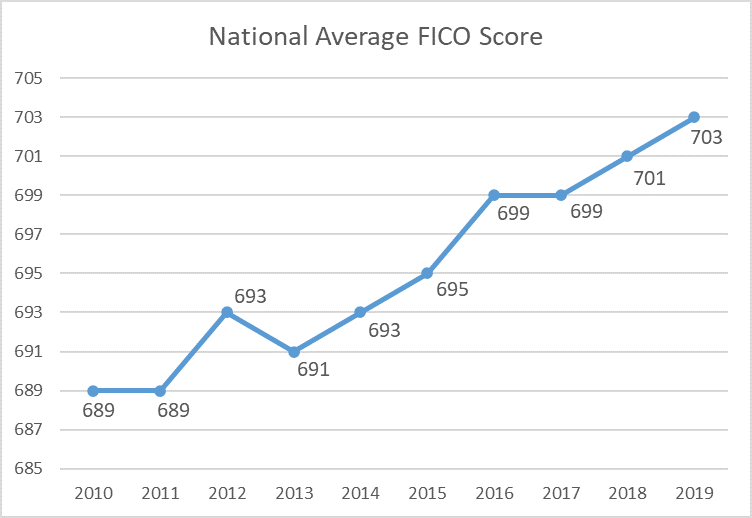

In response to a current report from FICO, shopper debt has elevated to report ranges, and but the typical credit score rating in the US has elevated to a report excessive of 718 as of April 2023. This may be attributed partly to adjustments within the financial system and altering credit score reporting insurance policies, however there may be one other main issue that has the banks anxious.

The nationwide common FICO rating has been on the rise for the previous decade, surpassing the 700 mark in 2018.

Sufficient time has handed because the Nice Recession of 2008 that all the delinquencies and derogatory marks on shoppers’ credit score studies from that interval of economic hardship have been faraway from their data. Subsequently, collectors can now not see how shoppers dealt with the recession and whether or not they have been capable of pay all of their payments when the financial system went south.

Couple this with the worry of one other attainable financial recession on the horizon, and you may perceive why lenders have began to really feel involved that delinquencies and defaults could quickly start to rise to a degree that isn’t mirrored in shoppers’ excessive credit score scores.

Due to these financial elements, the credit score scoring system wanted an overhaul that will bear in mind the altering financial local weather in addition to altering shopper habits and permit for higher predictions of credit score threat and default charges.

FICO 10: Extra Correct Predictions of Credit score Threat

FICO predicts that FICO 10 will decrease defaults on auto loans by 9% and defaults on mortgages by 17%.

Because of the adjustments made to the scoring mannequin that we mentioned above, particularly the inclusion of trended information for the FICO rating 10 T, FICO claims that the brand new scores carry out higher than all earlier FICO scores by considerably reducing shopper default charges.

Right here’s what else FICO has to say about their new merchandise:

“By adopting the FICO® Rating 10 Suite, a lender might scale back the variety of defaults of their portfolio by as a lot as ten p.c amongst newly originated bankcards and 9 p.c amongst newly originated auto loans, in comparison with utilizing FICO® Rating 9. The discount in defaults is even greater for newly originated mortgage loans, at 17 p.c in comparison with the model of the FICO Rating utilized in that business. These enhancements in predictive energy will help lenders safely keep away from surprising credit score threat and higher management default charges, whereas making extra aggressive credit score gives to extra shoppers.”

How Is FICO 10 Completely different Than Earlier FICO Scores?

Though FICO routinely updates their credit score scoring algorithms each 5 years or so, this would be the first time that they’re releasing two completely different variations of the identical basic scoring mannequin: FICO 10 T, which makes use of trended information; and FICO 10, which doesn’t use trended information.

Each FICO 10 and FICO 10 T will probably be drastically completely different than the earlier FICO rating, FICO 9. FICO 9 was designed to be very forgiving to shoppers, which led many to consider that it produced credit score scores that have been greater than they need to have been.

With FICO 9, for instance, medical collections got much less weight than different forms of collections, which was a profit to shoppers scuffling with medical debt.

Moreover, FICO 9 fully ignored paid assortment accounts, which means that in the event you had a group in your credit score report however then paid the stability, it will now not have an effect on your credit score rating. Many felt that this modification contributed to FICO 9 overestimating the creditworthiness of shoppers, which in flip led to the scoring mannequin not being accepted by many industries.

In distinction, the FICO 10 scores characterize a swing again in the wrong way. It’s designed to be much less lenient towards shoppers with dangerous credit score behaviors so as to keep away from understating shoppers’ credit score threat. In that sense, it’s in all probability extra much like FICO 8 than to FICO 9. Nonetheless, FICO 10 additionally rewards shoppers who’ve efficiently managed their credit score.

To perform this, FICO made some important adjustments in creating their newest set of credit score scoring algorithms.

Trended Knowledge

The brand new FICO 10 T rating is the primary FICO rating to take a look at trended credit score information.

The FICO 10 T rating will incorporate trended information, which implies that it’s going to not simply take into account your credit score profile as a “snapshot” in time, however reasonably, it’s going to bear in mind your credit score habits over the earlier 24 to 30 months and the way your credit score profile has modified in that point.

VantageScore 4.0, a competing credit score scoring mannequin, has been utilizing trended information because it debuted in 2017. Now, FICO is following go well with with their 10 T rating.

Due to the temporal information FICO 10 T has to attract from, it’s much more predictive of a borrower’s credit score threat than the essential FICO 10 rating, which might solely see a “snapshot” of your credit score report at a given cut-off date.

For shoppers, the trended information issue is particularly important for the credit score utilization portion of your credit score rating. In fact, credit score scores already checked out your fee historical past from the previous seven to 10 years, however till now, they solely checked out your credit score utilization ratios at a given cut-off date.

Which means that with most credit score scoring fashions, even in the event you max out your bank cards one month and your credit score rating suffers because of this, so long as you pay down your playing cards once more by the subsequent month, your rating can nonetheless bounce proper again to the place it was earlier than you maxed out the cardboard.

With FICO rating 10 T, nevertheless, it will not be really easy to get better from excessive balances, as a result of a report of being maxed out might stick round for the subsequent 24 to 30 months.

As well as, in case your balances have been climbing greater over the past two years or when you’ve got been looking for credit score extra aggressively, you might be penalized by FICO 10 T, as a result of this type of habits signifies a better threat of you defaulting sooner or later.

However, when you’ve got been managing your credit score effectively and your debt ranges have been reducing over the previous two years, you may be rewarded for that habits.

Private loans from on-line lenders have exploded in recognition, but it surely’s finest to keep away from them if you wish to get a excessive FICO 10 credit score rating.

Private Loans Will Be Penalized

The vp of scores and analytics at FICO, Joanne Gaskin, has mentioned that probably the most important change to the scoring algorithm is the best way it treats private loans.

Private mortgage debt has grown sooner than every other kind of shopper debt over the previous decade, even bank cards. Customers are turning to non-public loans to consolidate bank card debt extra ceaselessly than previously, and the proliferation of economic expertise firms has made private loans simpler to qualify for and extra accessible.

With older FICO fashions, private loans are handled the identical as every other installment mortgage. For the reason that balances of installment accounts don’t have an effect on credit score scores as a lot because the utilization ratios of your revolving accounts, with most scoring fashions, taking out a private mortgage to consolidate bank card debt (basically changing revolving debt into installment debt) would profit a shopper’s credit score rating.

Nonetheless, many shoppers who take out private loans to repay revolving debt don’t change the spending habits that obtained them into debt within the first place. Consequently, after getting a private mortgage and paying down their bank cards, they might run up their playing cards once more and discover themselves even deeper in debt.

In response to FICO, the credit score threat of such shoppers is greater than you’ll suppose primarily based on their credit score scores utilizing earlier FICO fashions. To account for this, FICO 10 is treating private loans as their very own class of credit score accounts and is probably penalizing shoppers for taking out private loans.

With FICO 10 T, current missed funds will matter much more than they already do with different FICO rating variations.

Subsequently, with FICO 10, the technique of consolidating bank card debt with a private mortgage won’t assist your credit score rating as a lot as you hope and would possibly even damage it. Nonetheless, the unfavourable affect of taking out a private mortgage may be mitigated by steadily working to cut back your total debt degree.

However, in case your total debt load stays the identical or continues to extend after you are taking out a private mortgage, that might damage your credit score rating as a result of it reveals lenders that you’re getting deeper into debt and never managing your credit score effectively.

Current Missed Funds Will Be Penalized Extra Closely

Cost historical past has all the time been crucial a part of a FICO credit score rating, however it’s much more necessary with FICO 10 T, the trended information rating.

Utilizing historic information, it will probably assign late and missed funds much more weight primarily based in your habits previously 24 months. For instance, in the event you’ve been getting progressively farther behind on funds over time, the unfavourable affect in your credit score rating could possibly be even larger than it will with a earlier FICO rating.

In case you have delinquencies which are a minimum of a yr previous, although, then these older unfavourable marks in your credit score report received’t damage your rating as a lot, in keeping with MSN.

How Will the FICO 10 Scoring Mannequin Have an effect on Credit score Scores?

Total, it’s predicted that the brand new FICO 10 scoring fashions can have a polarizing impact on shoppers’ credit score scores, which implies that some shoppers who’ve a bad credit score scores may even see them drop even additional, whereas those that have good credit score scores as a result of they’re heading in the right direction could also be rewarded with even greater scores.

40 million shoppers are more likely to expertise a credit score rating drop of 20 or extra factors with FICO 10 in comparison with earlier fashions. This might push some shoppers over the sting right into a decrease credit standing class.

FICO has estimated that roughly 100 million shoppers will in all probability expertise minor adjustments of lower than 20 factors to their scores. The corporate additionally estimates that about 40 million shoppers will see their credit score scores drop by 20 or extra factors, whereas one other 40 million might see their scores improve by the identical quantity.

You might be more likely to see a credit score rating drop in the event you took out a private mortgage to consolidate debt however then stored accruing extra debt as a substitute of paying it off, or when you’ve got bank card debt that you’re not paying down.

You might be most certainly to see a credit score rating improve when you’ve got been penalized for having excessive balances infrequently because the temporal information from FICO 10 T will assist to common out the peaks in your utilization fee.

Whereas a lower of 20 factors in your credit score rating isn’t catastrophic, it could possibly be sufficient to make a distinction in your probabilities of being authorised for credit score or the rates of interest you might qualify for. That is very true for these whose credit score scores sit close to the decrease border of a credit score rating class.

For instance, somebody with a credit score rating of 595 with FICO 8 is taken into account to have honest credit score. If FICO 10 gave them a credit score rating that’s 20 factors decrease, their credit score rating could be 575, which is taken into account a bad credit score. That might very effectively make or break your probabilities of getting authorised for a mortgage or a bank card.

However, the inverse is true for many who stand to achieve 20 factors. If a 20-point improve pushes a shopper over the sting from honest credit score to good credit score, for instance, this might actually be useful when making use of for credit score.

It’s estimated that 80 million shoppers will see a big change of their credit score scores with FICO 10, which can transfer them into completely different credit score rating ranges.

Much less Extreme Rating Fluctuations

As chances are you’ll recall from How you can Select a Tradeline, the extra information there may be contributing to a mean, the tougher it’s to have an effect on that common.

Since FICO 10 T appears to be like at your credit score utilization for an prolonged time frame as a substitute of simply the present month, it’s probably that your credit score rating won’t change as drastically from month to month primarily based in your utilization ratios on the time.

In different phrases, your utilization information from the previous 24 to 30 months can have a stabilizing impact in your rating that may shield it from being closely penalized in the event you sometimes have excessive balances. For instance, in the event you spend additional in your bank cards in December to arrange for the vacations, your rating that month received’t be damage as a lot as it will with out the trended information (so long as you pay it off shortly).

Higher Emphasis on Traits and Current Knowledge

FICO 10 T will particularly reward shoppers who’ve a pattern of bettering their credit score over time.

The inclusion of trended information with FICO Rating 10 T and further emphasis on current information signifies that your credit score rating shouldn’t be primarily based solely on what your accounts appear to be at this time, however as a substitute, it’s going to give extra significance as to whether your credit score is getting higher or getting worse.

Hypothetically, it’s attainable that two shoppers with the identical quantity of debt and derogatory gadgets might have completely different credit score scores primarily based on the pattern of their debt ranges.

If one shopper has $10,000 of bank card debt, however they’ve been making progress on paying that down from a place to begin of $20,000 of debt, then their credit score rating could be helped by FICO 10 T as a result of their debt degree is demonstrating a pattern of enchancment over time.

If the opposite shopper additionally has $10,000 of bank card debt, however they used to solely have $1,000 of revolving debt, that pattern reveals that they’re getting deeper into debt, and their FICO 10 rating could be damage by that sample of accelerating debt.

A Polarizing Impact on Credit score Scores

One of many main results of FICO 10 is that it’s probably going to polarize the pool of shoppers’ credit score scores. In different phrases, these close to the highest of the credit score rating vary will get even greater, whereas these with low credit score scores will sink even decrease alongside the size.

In response to CNBC, shoppers with scores of decrease than 600 will expertise the biggest reductions of their credit score scores with FICO 10. These with scores of 670 and above might presumably achieve as much as 20 factors.

This creates a distribution of credit score scores that’s extra concentrated on the two extremes, versus most shoppers’ credit score scores being concentrated across the common.

Sadly, which means the unfavourable results of the brand new FICO scores will disproportionately affect shoppers who’re already scuffling with debt. This may make it even tougher for shoppers to get out of debt and will pressure them to hunt out pricey, predatory loans, which solely accelerates the downward spiral of debt.

This perpetuation of inequality within the credit score scoring system shouldn’t be new, however it appears that evidently FICO 10 will solely serve to extend credit score inequality reasonably than enhance it.

Finally, FICO’s shoppers are the banks, and their merchandise are designed to offer banks the higher hand, not shoppers.

When Will the New FICO Rating Be Rolled Out?

By widening the divide between shoppers with good credit score and people with a bad credit score, it appears that evidently FICO 10 will exacerbate credit score inequality.

In response to FICO, the FICO Rating 10 Suite of merchandise will probably be obtainable in the summertime of 2020. The vp of scores and predictive analytics at FICO, Dave Shellenberger, advised The Steadiness that Equifax will probably be adopting the brand new rating shortly thereafter.

As to when lenders will truly begin to use the brand new credit score scoring system, that could be a completely different query.

Lenders Are Sluggish to Adapt to New Credit score Scoring Programs

The monetary business adapts very slowly to systemic adjustments. As we mentioned in “Do Tradelines Nonetheless Work in 2020?”, there are numerous, many alternative variations of FICO, and nearly all of lenders are nonetheless utilizing variations of the rating which are years and even many years previous.

Earlier than FICO 10, the most recent model had been FICO 9, which has largely gone unused by lenders.

FICO 8 is the credit score scoring mannequin that’s at the moment being utilized by the three main credit score bureaus and additionally it is probably the most broadly used mannequin amongst lenders at this time. FICO 8 debuted in 2009, which implies it has now been round for over a decade.

There are specific industries that rely closely on FICO rating variations which are even older than FICO 8. Within the mortgage business, the most well-liked FICO scores are variations 2, 4, and 5, the earliest of which debuted within the early Nineteen Nineties. Auto lenders could use FICO scores 2, 4, 5, or 8, whereas bank card issuers use fashions 2, 3, 4, 5, and eight.

Moreover, many industries and even some giant lenders have their very own proprietary FICO scoring fashions which have been custom-made for that specific establishment and the buyer base they serve.

Lenders have amassed enormous troves of information primarily based on a selected credit score scoring mannequin. Having dependable information is essential to minimizing threat in the course of the underwriting course of. If lenders have been to alter to a brand new scoring mannequin, all the credit score scoring data they’ve collected to this point would now not be relevant, because it was calculated utilizing a distinct algorithm.

It’s probably that the FICO 10 T rating will take longer to implement than the essential FICO 10 rating as a result of FICO 10 T would require companies to coach workers to make use of a brand new set of purpose codes.

They might basically be ranging from scratch, which might imply taking up extra threat till they’ve examined the brand new mannequin for lengthy sufficient to grasp the way it works for his or her companies. Due to this, lenders are sometimes reluctant to improve to a more recent scoring mannequin and sluggish to implement it.

Subsequently, we are able to make an informed guess that it’s going to most certainly take a minimum of a number of years for FICO 10 to achieve traction with lenders on a big scale. In response to Shellenberger of FICO, it could take “as much as two years” earlier than lenders begin utilizing the brand new mannequin, though primarily based on previous examples, it appears probably that it might take considerably longer than that.

FICO 10 T Will Be Extra Difficult for Lenders to Undertake

In response to FICO, the usual FICO 10 rating makes use of the identical “purpose codes” as older FICO scores.

Cause codes, additionally known as “hostile motion codes,” are the codes that lenders should present if they’ve rejected your software for credit score primarily based on data out of your credit score report. These codes often encompass a quantity and a quick assertion of one thing that’s impacting your rating in a unfavourable method, reminiscent of revolving account balances which are too excessive in comparison with your revolving credit score restrict.

As a result of FICO 10 shares the identical purpose codes with earlier variations of FICO scores, this implies it will likely be appropriate with lenders’ present techniques, a minimum of with regard to purpose codes.

In distinction, FICO 10 T comes with a brand new set of purpose codes, which implies it will likely be a extra in depth endeavor for banks to implement the brand new rating and prepare workers on methods to use it.

For that reason, it appears probably that the essential model FICO 10 may even see widespread use amongst lenders earlier than FICO 10 T does.

How you can Get a Good FICO 10 Credit score Rating

Though some important adjustments have been made to the FICO 10 credit score scoring merchandise, the general rules of managing credit score stay the identical. Most significantly, make your entire funds on time, each time, and attempt to maintain your credit score utilization low.

Nonetheless, there are a number of particular factors to bear in mind if you wish to get credit score rating with FICO 10.

-

Assume twice about taking out a private mortgage

Since private loans will probably be extra closely penalized with FICO 10 scores, you’ll need to keep away from taking out a private mortgage except it’s completely crucial. As an alternative of counting on private loans to help your spending, attempt to save up for big purchases prematurely, and begin funneling some money from every paycheck into an emergency fund in case you run into monetary hardship.

For those who do find yourself needing to make use of a private mortgage, attempt to pay it down as shortly as you may. As well as, don’t run up the balances in your revolving accounts once more, as a result of the FICO 10 T algorithm doesn’t reward this habits, and your credit score rating will replicate that.

Take into account establishing automated funds for your entire accounts so that you just by no means by chance miss a fee.

Avoiding late or missed funds is of the utmost significance with any credit score rating, however it’s much more necessary with the brand new FICO scoring system. Late and missed funds could also be assigned extra weight primarily based in your current credit score historical past, particularly missed funds that occurred throughout the previous two years.

To keep away from lacking any funds, arrange your entire accounts to robotically deduct a minimum of the minimal fee out of your checking account earlier than your due date every month. Additionally, it’s a good suggestion to get into the behavior of checking your accounts recurrently to verify there haven’t been any errors or points with processing your automated funds.

For those who do by chance miss a fee, pay the invoice as quickly as you discover and take into account asking your lender to waive the late price. For those who handle to catch up earlier than 30 days have passed by, then you may keep away from getting a derogatory merchandise added to your credit score report.

Within the occasion that you end up with a 30-day late (or worse) in your credit score report, then you’ll need to be additional vigilant about making funds on time for a minimum of the subsequent one to 2 years if you’d like your rating to get better.

-

Repay your bank cards in full each month

Paying off your bank cards in full is all the time a good suggestion normally as a result of that method, you may keep away from losing cash on curiosity charges. As well as, paying off your full stability every month prevents your credit score utilization from growing from month to month, versus carrying over a stability after which including extra to it every month.

With trended information taking part in a big position in your FICO 10 T rating, consistency is essential, and paying your payments in full each time will assist enhance your rating.

If you wish to get credit score rating with FICO 10 and FICO 10 T, attempt to maintain your revolving debt low by paying off your bank cards in full each month.

-

Decrease your credit score utilization ratios

With FICO 10 T, it will likely be extra necessary than ever to be vigilant about sustaining a low credit score utilization ratio. For the reason that trended scoring mannequin accounts for patterns in your credit score utilization over the previous 24 months, it received’t be really easy to get away with maxing out your bank cards one month after which shortly paying the stability down to enhance your rating once more the subsequent month.

Excessive credit score utilization at any level previously two years could possibly be factored into your credit score rating, particularly in case your utilization has been growing over time.

For that reason, in case your credit score is being scored with the FICO 10 T mannequin, you’ll get one of the best outcomes in case your credit score utilization has been constantly low or if it has proven a sample of reducing over time.

Nonetheless, simply since you repay your bank card in full each month doesn’t imply it’s going to report a zero stability. The stability that studies to the credit score bureaus is the stability that you’ve on the finish of your assertion interval. In case your stability occurs to be excessive on that date, then it might negatively have an effect on your rating, even in the event you repay the stability quickly after.

One straightforward credit score hack to get round that is to pre-pay your bank card invoice earlier than your due date and your assertion deadline. That method, the stability will probably be low when the cardboard studies to the credit score bureaus, which is healthier on your credit score rating.

One other useful credit score hack is to unfold out a number of smaller funds all through the month in order that the stability by no means climbs greater than it ought to be to start with.

Learn extra about methods to get one of the best credit score utilization ratio in our article, “What Is the Distinction Between Particular person and Total Credit score Utilization Ratios?”

Requesting a credit score line improve may be a simple method to enhance your utilization fee, however this technique ought to be used with warning in the event you suppose it’d encourage you to rack up extra debt.

-

Improve your credit score restrict

One approach to simply decrease your utilization fee is to extend your credit score restrict. Spending $1,000 on a card with a credit score restrict of $5,000 is rather a lot higher on your utilization ratio than spending the identical quantity on a card with a credit score restrict of $2,000.

Growing your credit score restrict may be simpler than you suppose. It could possibly be so simple as calling up your card issuer on the telephone or making use of for a credit score line improve on-line. The truth is, most individuals who ask for a better credit score restrict get authorised.

Nonetheless, this technique shouldn’t be inspired for shoppers who could also be tempted by the upper credit score restrict to spend much more on the cardboard.

For recommendations on methods to get a bigger credit score restrict, in addition to some pitfalls to be careful for earlier than requesting a credit score line improve, try “How you can Improve Your Credit score Restrict.”

-

Work to enhance your credit score well being over time

With FICO rating 10 T together with extra details about your credit score historical past over the previous 24 months, it will likely be necessary to exhibit an enchancment in your credit score over time. Customers who’ve been working to handle their credit score responsibly and who’ve diminished their quantity of revolving debt over time will probably be rewarded.

However, these whose credit score well being has been declining attributable to growing debt ranges or a collection of missed funds will see their credit score scores take a dive.

For sources on methods to enhance your credit score, try the credit score articles and infographics in our Information Middle, reminiscent of “The Quickest Methods to Construct Credit score,” “Straightforward Credit score Hacks That Will Truly Get You Outcomes,” and “How you can Get an 850 Credit score Rating.”

Will the New FICO 10 Rating Have an effect on the Tradeline Business?

First, do not forget that it’s probably that it’s going to take a minimum of a number of years for FICO 10 to be broadly adopted by lenders (if lenders select to make use of it within the first place, which they might not), which signifies that nothing is altering for the tradeline business within the close to future.

Secondly, many lenders could select to undertake solely FICO 10 and never FICO 10 T as a result of it will likely be technically simpler to implement. For lenders utilizing FICO 10 with out the trended information, there shouldn’t be a change to how approved consumer tradelines work.

Nonetheless, issues get extra attention-grabbing when contemplating the affect of FICO 10 T, the trended model of the brand new rating, on patrons and sellers of tradelines. Till FICO 10 T is adopted by main lenders, we are able to solely speculate as to the adjustments that may end result, however right here is one risk.

What If FICO 10 T Reveals a Tradeline’s Steadiness Historical past?

One concern that buyers could have is that FICO 10 T might expose a tradeline’s earlier excessive stability if it had one at any level in the course of the previous 24 to 30 months. Which may be true, however we additionally know that FICO 10 T locations lots of significance not simply on the numbers themselves, however on how they alter over time.

The entire tradelines on our tradeline listing are assured to have a utilization ratio of 15% or decrease. If a tradeline had a better stability sooner or later previously two years or so, then it will present a pattern of the stability reducing, because the stability would have been introduced all the way down to beneath 15% so as to take part within the tradeline program.

FICO 10 T rewards downward tendencies in utilization, so it appears that evidently approved consumer tradelines would nonetheless present worth even when greater balances may be seen previously.

If a tradeline has not had a excessive stability previously two years, then which means it’s going to present a sample of constantly low utilization over time, which can be useful.

Conclusion: What Does the New FICO 10 Credit score Rating Imply for Customers?

Quite a lot of hypothesis and daring claims have been circulating in regards to the new FICO scores, FICO 10 and FICO 10 T. Naturally, shoppers and tradeline sellers alike are involved with the query of how the brand new scoring algorithms would possibly have an effect on approved consumer tradelines.

It’s true that FICO has made some important adjustments to their newest credit score scoring mannequin, and it’s additionally probably that some shoppers could expertise marked will increase or decreases of their credit score scores in comparison with earlier FICO scoring fashions. Fortuitously, nevertheless, there isn’t any have to panic.

Comply with the overall tips of fine credit score to get a excessive rating with any credit score scoring mannequin.

First, let’s do not forget that FICO 10 shouldn’t be in use but, and it’s in all probability going to take a number of years or extra for almost all of lenders to undertake it.

As well as, the scoring mannequin that individuals are most involved about, FICO 10 T, will take even longer than FICO 10 to succeed in mainstream recognition because it requires lenders to discover ways to begin utilizing a brand new set of purpose codes.

For that reason, shoppers don’t want to fret about lenders seeing the previous two years of their credit score histories simply but. Nonetheless, understanding that widespread use of trended information could also be on the horizon, chances are you’ll need to begin making ready your credit score now. That method, when trended information credit score scores turn out to be extra well-liked, your credit score will probably be sturdy and able to face up to the adjustments.

To obtain a excessive credit score rating with FICO 10 and FICO 10 T, keep away from taking out private loans in the event you can, as they are going to be penalized extra closely than previously. It’s additionally necessary to exhibit both an enchancment in your credit score over time or constantly good credit score habits, which will probably be rewarded.

Other than these particular concerns, FICO 10 and FICO 10 T nonetheless rely totally on the identical credit score rating elements you’re already aware of: your fee historical past, credit score utilization, size of credit score historical past, credit score combine, and new credit score. Whereas the peripheral particulars of various scoring fashions could fluctuate, the core parts all the time stay the identical.

Finally, in the event you work on growing good credit score practices in these basic areas, your credit score will probably be in nice form regardless of which scoring mannequin is used.

[ad_2]

Source link