[ad_1]

HubSpot calculates it prices greater than $644 for monetary companies organizations to accumulate a brand new buyer. It is important that this funding isn’t wasted, and candidates aren’t misplaced to a poor onboarding expertise. With every new buyer there are potential dangers; candidates could also be a poor credit score danger, a fraudster, and even be a stolen or fabricated id. It’s essential to defend in opposition to these dangers, however most candidates are beneficial new clients, and also you don’t wish to put pointless limitations of their manner.

As you onboard new clients, the checks concerned will be intensive and completely different checks are managed by completely different elements of the enterprise. Usually, every has their very own techniques and processes. As one a part of the enterprise solves their points, the unintended consequence is that they create issues for his or her colleagues, leading to numerous utility fraud and credit score danger challenges for the group. These embody:

False positives – fraud danger prevents good buyer expertise. Suspicion of fraud doesn’t all the time equate to actual fraudulent exercise, however every case have to be investigated. That is pricey by way of assets, and for purchasers who’re unnecessarily investigated it may be a poor expertise as their utility is halted or delayed.

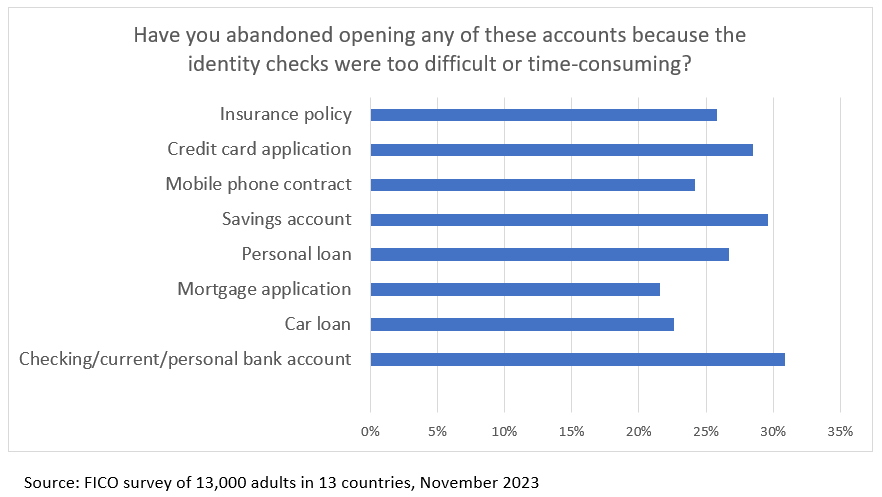

Buyer verification – id fraud checks enhance utility abandonment. Fraud prevention and safety in opposition to cash laundering require acceptable know your buyer (KYC) processes. Whereas clients perceive the necessity for checks, their persistence is restricted. FICO analysis discovered that as much as 31% of individuals have deserted opening a brand new monetary account as a result of id checks carried out by monetary establishments had been both too tough or too time-consuming.

Gross sales drive — undetected fraud creates future losses. As monetary organizations look to fulfill aggressive gross sales targets and originate as many new clients as doable, anti-fraud measures will be recognized as enterprise prevention — this could result in companies decreasing their defenses. With utility fraud, the fraudulent intent is steadily not instantly apparent and notoriously difficult to detect. Fraud can keep dormant with accounts managed by pretend or artificial identities that seem like worthwhile clients, till they’ve amassed sufficient credit score to bust out inflicting most losses.

Mis-identified fraud — first-party fraud creates collections burden. First-party fraud accounts for round 10% of the amount of credit score losses however greater than 20% of the worth. These direct fraud losses are amplified when it’s mis-identified and handled as unhealthy debt. Collections groups waste vital time and useful resource chasing “unhealthy debt” that’s actually fraud and which they can’t recuperate.

3 Methods to Break By way of the Siloes

Breaking down these siloes and fostering a extra collaborative and communicative tradition usually requires a concerted effort from management, modifications in organizational construction, and a dedication to selling cross-functional teamwork and a shared organizational mission. A current FICO ballot of senior executives tasked with stopping utility fraud discovered that 85% of them put a excessive precedence on know-how that helps real-time fraud detection built-in with credit score originations.

Listed below are 3 ways you may break by way of the siloes:

1. Develop a typical language

Numerous interpretations and definitions of essential phrases typically foster remoted pondering, resulting in communication breakdowns, inefficiency, and conflicts. As an instance, quite a few organizations lack universally accepted definitions for numerous fraud typologies, ensuing within the misclassification of fraud as unhealthy debt. The boundaries between fraud, particularly first-party fraud, and unhealthy debt are blurred. Whereas the exact definitions could differ amongst organizations, it’s important to take care of consistency inside your monetary establishment.

By clearly articulating the definitions of first-party, third-party, and artificial id fraud, you considerably improve the probability of acceptable dealing with, thereby decreasing fraud losses and optimizing operational efficiencies.

A refined definition may also play a pivotal function in formulating an efficient technique for fraud administration. Presently, organizations typically segregate the oversight of first-party and third-party fraud, delegating the previous to the credit score danger staff and the latter to the fraud staff. Nonetheless, this method results in problems, significantly when coping with artificial identities that exhibit traits of each first-party and third-party fraud. The ensuing lack of synergy typically leads to the next incidence of artificial id fraud instances being routed to the collections staff. By decreasing the inflow of fraud instances directed towards the collections course of, we empower the collections staff to focus their energies on pursuing recoverable money owed, finally bolstering their general effectivity.

To begin your journey to strong and agreed fraud classifications try these assets from The Federal Reserve and the Euro Banking Affiliation

2. Set up Widespread Reporting Strains

Quite a few monetary establishments have already entrusted the Chief Danger Officer with paramount duty for managing each utility fraud danger and credit score danger. Nonetheless, the true worth emerges when these aims are comprehended and collaboratively embraced all through the reporting hierarchy. The convergence of reporting strains yields vital dividends, together with the institution of efficient communication channels, the formation of cross-functional groups, higher allocation of assets, and enhanced info sharing.

3. Nurture the Essential Variations

Eradicating siloes doesn’t essentially make the entire convergence of various features fascinating. Originations, fraud, monetary crime compliance and collections all intersect with lately established buyer relationships, however they continue to be inherently distinct. Every perform has its personal aims and requires specialised skillsets to attain them. Breaking down siloes requires finesse and mustn’t lose sight of the basic targets every perform should obtain. By specializing in a typical imaginative and prescient, selling cross-functional groups, and fostering efficient communication, we will eradicate these limitations with out jeopardizing core competencies.

Eradicating siloes: Folks, Course of and Know-how

In my subsequent two posts I take into account the function improvements in processes and know-how ship in decreasing or eliminating the limitations that forestall collaborative and efficient originations and fraud administration.

[ad_2]

Source link

:max_bytes(150000):strip_icc()/1.4-f4d6ef0efe254c1f9ab652d24f666e7a.png)