[ad_1]

In an ever-more aggressive market, banks are seeing a variety of enterprise going begging. There could also be quite a few culprits, however a uneven onboarding expertise, avoidable friction and an incapability to supply finance to prospects via the suitable channels are widespread components for many organisations.

Buyer expertise is predicted to change into a better differentiator than worth for a lot of, making the expertise supplied throughout the embryonic, originations stage of the shopper relationship crucial. Provided that poor course of and buyer expertise is usually a results of expertise constraints, it is necessary to contemplate how expertise can be utilized to supply the very best originations expertise. Get it proper and it is doable to keep away from lacking out on worthwhile lending. Get it mistaken and the chance is gone for good.

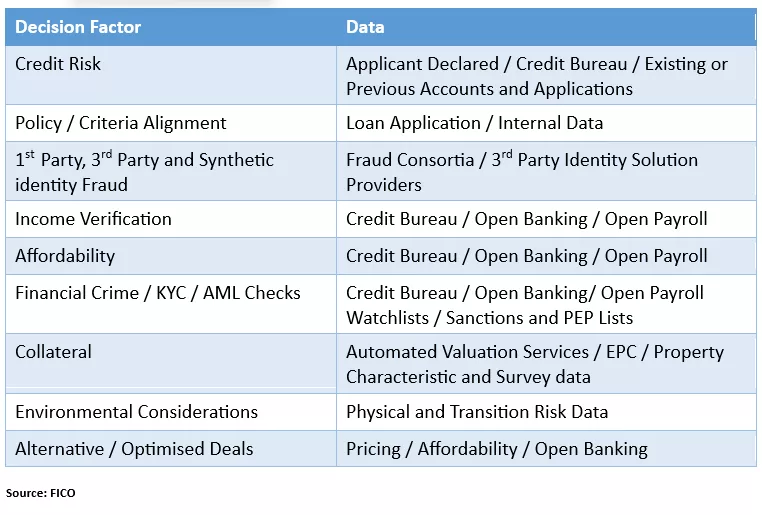

Whereas there may be proof that prospects admire the necessity for a degree of friction inside onboarding, for some merchandise it have to be proportionate. An excessive amount of friction, or a fragmented course of, and candidates might abandon the transaction fully. It’s a difficult balancing act. Originations administration is multi-faceted and underpinned by a mix of crucial determination components, the place the sum of the elements mix to create the general lending determination. Every determination issue requires completely different information sources, which if they’re for use as effectively as doable, require completely different ranges of analytical sophistication.

The Anatomy of Originations Selections

Exploring the Originations Resolution Administration Challenges

For a lot of lenders, the a number of determination components have been a reason for disjointed originations processes, which elongate the journey – as a result of they contain requests for paperwork, or a swap to pricey and needlessly time-consuming legacy decision-making methods. Extra friction and breaks within the course of imply extra candidates are prone to go together with a competitor who is ready to present a extra seamless journey. The problem for lenders is to create originations processes with acceptable ranges of friction, while sustaining sturdy danger assessments, to successfully adjust to regulation and handle ranges of delinquency and loss.

The emergence of latest channels via which prospects receive finance represents an extra origination expertise problem. However it’s one that may unlock the handy, seamless experiences on which prospects are putting rising worth. Value comparability web sites have been a cornerstone inside many markets for years, and embedded finance choices, akin to these the place a finance possibility is chosen on the check-out of an e-commerce portal, are rising quickly. At the moment dominated by fintechs, it is an space the place the British Retail Consortium count on to see as much as 25% year-on-year development between now and 2028. To maximise their market share, banks want methods that may meet the completely different necessities of their inner gross sales groups and a number of third events.

Going through the Originations Challenges

With the suitable expertise it’s now doable to drive out handbook or high-friction interventions and supply seamless, near-instant credit score selections throughout a number of gross sales channels, with out compromising on danger controls in any respect. There are three crucial belongings, which ought to be utilized in mixture:

1. Open Architectures

API-enabled structure is essential to offering the flexibleness required for connecting a typical technique system with a number of gross sales interfaces and information sources. When mixed with the potential to tailor the response message through the favoured requesting channel, with out vital quantities of advanced coding, it turns into far simpler to promote via a number of channels and shut any gaps proscribing new enterprise.

This degree of flexibility is essential to reaching market share as an already aggressive setting turns into extra aggressive nonetheless. Open architectures have allowed the strains between ‘conventional’ lenders, fin-techs and tech-savvy, non-finance organisations, like Apple to change into blurred. It’s necessary for banks to reply via the adoption of their very own equally open and adaptive determination structure.

2. Versatile Knowledge Fashions

API-enabled architectures connecting to new information sources, should be supported by the flexibility to make information available to be used. It’s very important to have a choice system with a versatile information mannequin to facilitate using new information, from throughout the organisation or from third events, shortly and effectively. Think about the tempo of change inside Open Banking, Open Finance and Open Knowledge ecosystems, the place new information sources are frequently rising. Open Payroll, the place wage information may be shared straight with lenders, supplies a latest instance of the continued development of structured information that is out there to underpin automation of originations processes.

The faster banks can leverage the ever-expanding information universe, the better the aggressive benefit will likely be, particularly in terms of delivering a first-class buyer expertise, while retaining sturdy danger controls.

3. Superior Analytics Improve Originations Selections

It’s not sufficient to have the ability to connect with and accommodate all the brand new information sources. The wealthy vein of buyer perception must be discovered so the all-important knowledgeable view may be operationalised shortly with out introducing avoidable delays.

Longstanding parts of an origination’s determination, akin to credit score scoring, revenue verification, affordability assessments, utility fraud and AML checks already require an array of analytical methods to allow their handiest determination improvement and execution. Harnessing new information sources, such because the rising use of Open Banking information for extra sturdy assessments of candidates with little to no credit score historical past, additional embeds the necessity for a variety of superior analytical capabilities.

Consequently, when boardrooms make selections about their analytics and back-office methods, they want to consider carefully concerning the extent of the capabilities supplied – and whether or not they’re sufficiently extensible to make greatest use of latest and rising information sources. Richer information and extra superior analytical capabilities are additionally extending conventional determination making, to supply personalised, various offers for purchasers. They permit automated promotion of different merchandise and pricing, primarily based on what’s recognized as being necessary to every buyer as a person. Typical advantages embody:

-

Settle for charges may be improved by figuring out merchandise for which an in any other case declined buyer is eligible.

-

Automation of the counter-offer course of results in larger conversion charges.

-

Personalising presents ensures higher alignment between buyer and product, supporting the higher buyer outcomes required by the UK Client Responsibility

Whereas the potential for better ranges of determination sophistication is rising, latest rulings in Germany have supplied a well timed reminder for all companies, of the significance of sustaining determination transparency and explainability. The options companies put in place should additionally assist transparency from the purpose of analytical improvement, throughout to determination execution.

How FICO Is Serving to

By combining the three belongings described above, inside their determination system structure, lenders can overcome the challenges offered to their originations groups. FICO Platform ensures the supply of a first-class originations expertise, with out sacrificing danger controls, via any variety of gross sales channels. In doing so, lenders can maximise conversion charges and assist guard towards lack of market share from leaner and extra agile rivals.

[ad_2]

Source link