[ad_1]

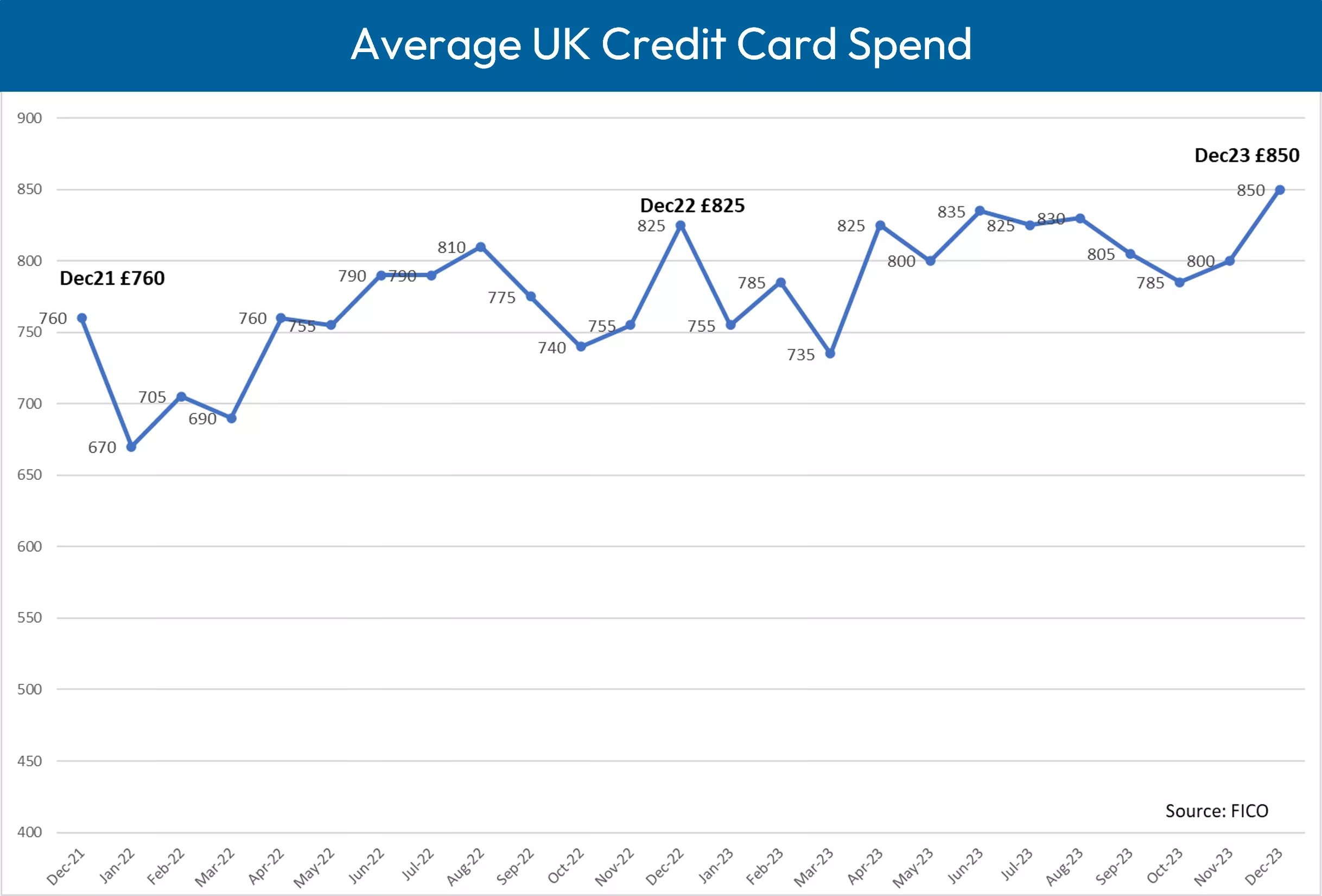

The FICO UK Credit score Card Market Report for December 2023 displays the standard season traits in UK spending and funds. Nevertheless, it additionally displays the impression of continued excessive costs on bank card balances. This newest report exhibits the best ranges of each common spending and common credit score balances on UK playing cards since 2006, when FICO first started benchmarking bank card use and funds within the UK.

Highlights

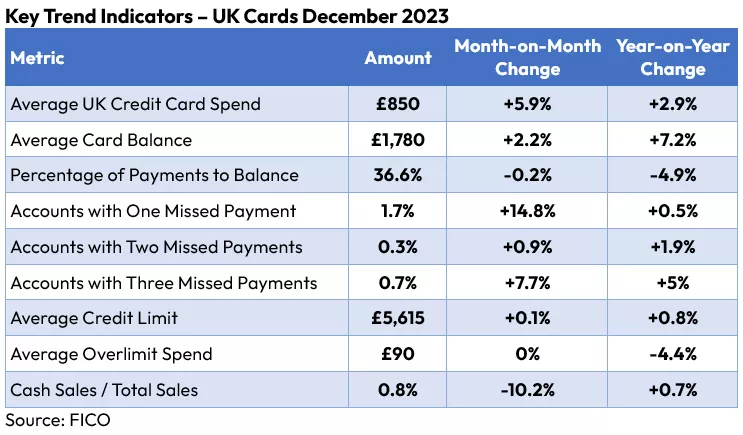

- Common UK spending on bank cards elevated by 5.9% on the earlier month, to £850

- Common stability on bank cards rose by 2.2% month-on-month and seven.2% year-on-year, resulting in a median stability of £1,780

- 14.8% extra UK customers missed a bank card fee month-on-month and 0.5% extra in comparison with the identical month in 2022

- There was a 1.3% lower within the common credit score stability for these customers lacking one fee

Elevated spending on bank cards at all times happens in December, and 2023 was no exception with a 5.9% month-on-month rise, taking the common spending to £850. That is the best spending within the UK since FICO data started in 2006.

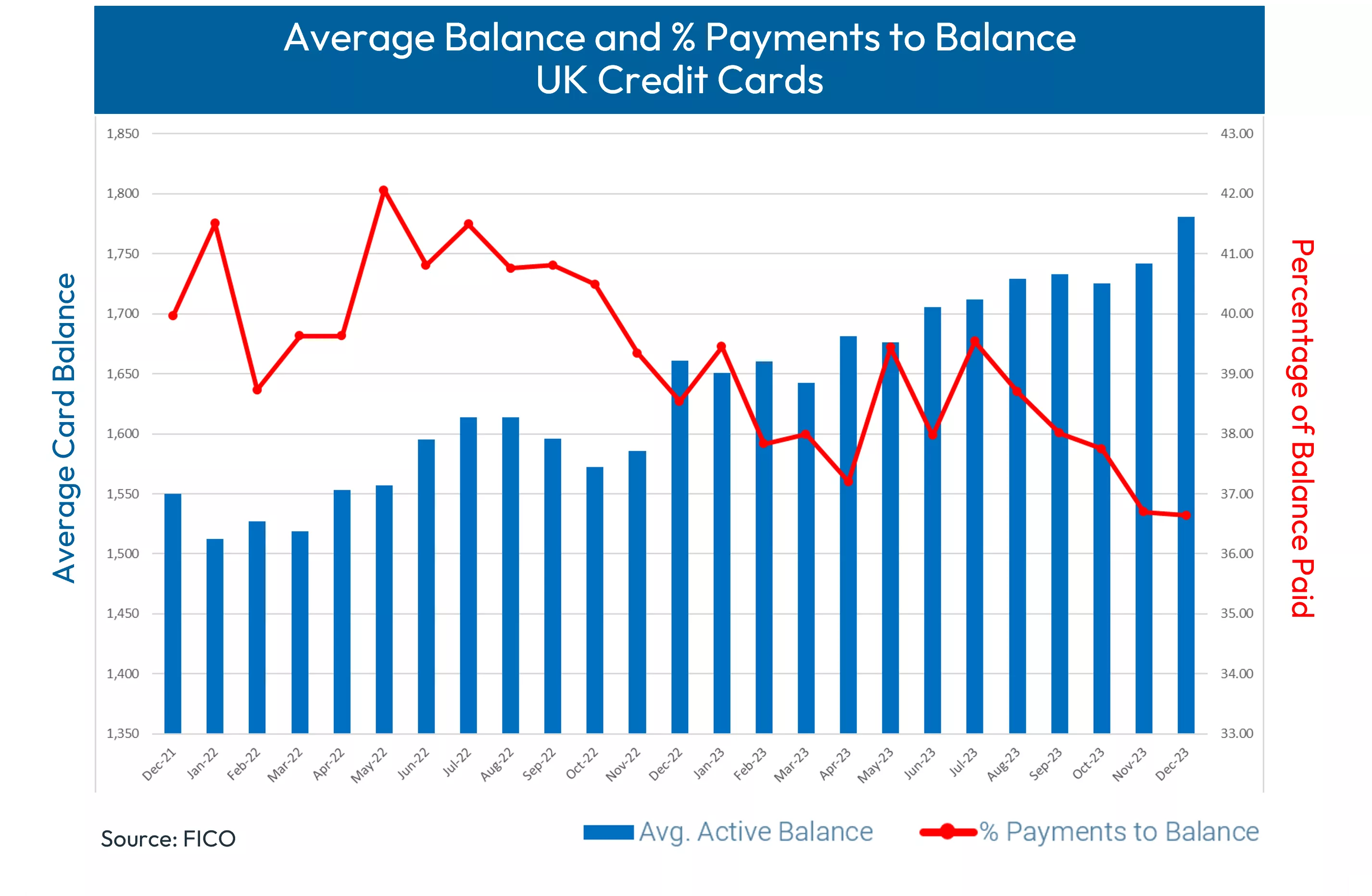

The common credit score stability within the UK continued to development upwards, as anticipated within the lead as much as Christmas. December 2022 noticed document common balances on bank cards. In December 2023 that document was damaged with common credit score balances up 2.2% month-on-month and up 7.2% year-on-year. The common stability now stands at £1,780. It’s anticipated that this development will fall post-Christmas, nonetheless with costs remaining excessive lenders will wish to monitor carefully how a lot it would fall, and for a way lengthy it would stay decrease.

One other sample typical of December was the quantity paid off bank card balances as UK customers focussed their cashflow on Christmas spending. In December 2023 the common stability paid off dropped barely, by 0.16%, month-on-month. Nevertheless, this measure has been trending down since July.

Balances and Late Funds

Pre-COVID-19, for UK customers the common bank card fee in comparison with the general stability was roughly 30%, however with lockdown and elevated financial savings this rose to 42%. The FICO information now exhibits this dropping again, though it’s at present nonetheless 6% greater than earlier than the pandemic.

One other signal of stress on funds was the variety of UK customers lacking one, two and three bank card funds. This elevated from November to December 2023, with the biggest enhance seen for these lacking one fee: a 14.8% enhance month-on-month and a 0.5% enhance in comparison with 2022. Once more, seasonality influences outcomes with related volumes anticipated in January because of the post-Christmas spending hangover. Lenders can even wish to be conscious that greater numbers of UK customers lacking one bank card fee in December are more likely to roll over into two funds in January.

Issuers ought to be aware that established cardholders – those that have had their bank card between one and 5 years – are the most probably to overlook funds. This group incorporates prospects whose 0% presents have expired, and they’re now paying off balances at the usual fee. FICO recommends monitoring this group for indicators of vulnerability and indebtedness. Now is a superb time to evaluate current collections methods and look at whether or not something extra could be achieved to proactively establish and help financially distressed customers.

These bank card efficiency figures are a part of the credit score information shared with subscribers of the FICO® Benchmark Reporting Service. The information pattern comes from shopper stories generated by the FICO® TRIAD® Buyer Supervisor resolution in use by some 80% of bank card issuers within the UK. For extra info on these credit score traits, contact FICO.

How FICO Can Assist You Handle Credit score Card Threat and Efficiency

[ad_2]

Source link