[ad_1]

Late final yr, we reported that after a 2-point improve from the yr prior, the nationwide common FICO® Rating held regular from April 2023 to July 2023 at 718.

The most recent credit score rating information is in and as of October 2023, the nationwide common FICO® Rating now stands at 717. That is one level decrease than it was earlier in 2023 and displays the primary time the metric has decreased in a decade as proven in Determine 1. Provided that the FICO Rating is a lagging, not main, financial indicator, this implies that the results of excessive rates of interest and protracted inflation could also be beginning to weigh on shoppers, particularly these already struggling to handle their funds.

|

Common FICO® Rating 8 |

|||||||

|

October 2005 |

688 |

April 2011 |

688 |

October 2015 |

696 |

April 2020 |

708 |

|

October 2006 |

690 |

October 2011 |

689 |

April 2016 |

699 |

October 2020 |

713 |

|

October 2007 |

689 |

April 2012 |

690 |

October 2016 |

699 |

April 2021 |

716 |

|

April 2008 |

690 |

October 2012 |

689 |

April 2017 |

700 |

October 2021 |

716 |

|

October 2008 |

689 |

April 2013 |

691 |

October 2017 |

701 |

April 2022 |

716 |

|

April 2009 |

687 |

October 2013 |

690 |

April 2018 |

704 |

October 2022 |

716 |

|

October 2009 |

686 |

April 2014 |

692 |

October 2018 |

705 |

April 2023 |

718 |

|

April 2010 |

687 |

October 2014 |

694 |

April 2019 |

706 |

July 2023 |

718 |

|

October 2010 |

687 |

April 2015 |

695 |

October 2019 |

706 |

October 2023 |

717 |

Determine 1. Having stabilized earlier within the yr, the nationwide common FICO® Rating decreased by one-point in late 2023.

The info signifies that the one-point drop within the common FICO® Rating throughout this era is pushed by will increase in missed borrower funds and shopper debt ranges. Let’s dive into among the key tendencies impacting common credit score scores, together with total shopper credit score information and credit score well being, in a bit extra depth:

-

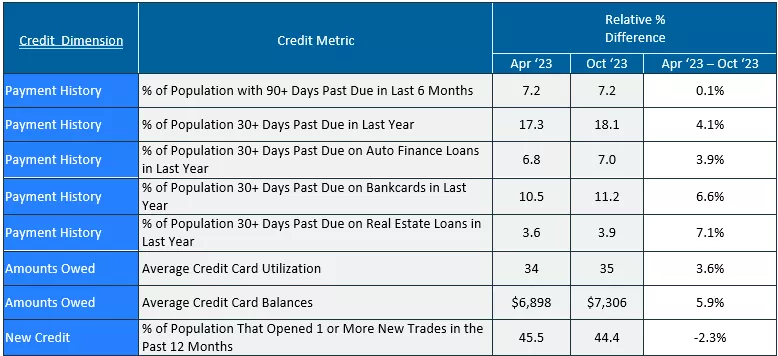

Missed funds proceed to rise: As of October 2023, simply over 18% of the inhabitants have had a 30-day or worse past-due cost on a number of credit score accounts within the final yr. That is up by 4% in comparison with April 2023.

Whereas missed funds on mortgages and auto loans have gone up, they’re nonetheless beneath their pre-pandemic ranges. Missed funds on bankcards have elevated, and now exceed their pre-pandemic ranges. The obvious cumulative impression of upper rates of interest, elevated shopper costs and financial uncertainty has put a monetary pressure particularly on these shoppers who closely depend on bank cards to cowl on a regular basis bills. This will result in increased bank card utilization and subsequent defaults on bank card funds. Paying payments on time can have a major and constructive impression on the FICO® Rating with the “Cost Historical past” class representing 35% of the general FICO Rating calculation.

- Shopper debt is increased than pre-pandemic ranges: As of October 2023, the typical credit score utilization was at 35%. That is up not solely from 34% as of April 2023, but additionally from 33% as of April 2020 and from 34% as of October 2019 (which might be seen as a seasonally adjusted pre-pandemic benchmark).Bank card balances exceeded $1 trillion (about $3,100 per particular person within the US) final fall and elevated by one other $50 billion (about $150 per particular person within the US) in This fall of 2023, based mostly on the newest fed from the Federal Reserve Financial institution of New York. Knowledge from the Federal Reserve additionally signifies that revolving credit score, which might be seen as a proxy for bank cards, elevated at an annual fee of 17.7% in November 2023. Persistent inflation and will increase in the price of securing and carrying debt seems to be inflicting shoppers, particularly these with restricted cashflow, to hold elevated ranges of debt. Conserving balances low on bank cards can have a considerable and constructive impression on the FICO® Rating. In reality, the “Quantities Owed” class which is closely weighted in direction of bank card balances and utilization represents 30% of the general FICO Rating calculation.

-

New credit score exercise slows down: As of October 2023, 44.4% of the inhabitants has opened at the very least one new credit score account previously yr. That is down not solely from 45.5% as of April 2023, but additionally from 47.3% as of April 2020 and 47.2% as of October 2019. This lower from April to October in 2023 was doubtless pushed by the continued decline in mortgage origination volumes in the identical interval. The most recent report from the Federal Reserve illustrates that mortgage origination volumes had been at $394 billion in This fall of 2023 — a modest improve from the earlier quarter, however nonetheless effectively beneath the trillion greenback quarterly origination volumes witnessed between 2020 and 2021.

Whereas auto mortgage and lease origination volumes had been largely unchanged between April and October in 2023, combination credit score limits elevated by 2.5% in the identical interval suggesting that buyers had been acquiring extra credit score both by securing increased limits on their present bank cards or by opening new bank card accounts. This development signifies an offset by the decline in mortgage origination volumes with fewer debtors acquiring credit score between April and October in 2023. The “New Credit score” class represents 10% of the FICO® Rating calculation, and this deceleration in credit score searching for conduct over the previous yr can, to a sure extent, offset the results of will increase in shopper delinquency and debt ranges.

Determine 2. FICO® Rating inhabitants has continued to degrade in key metrics between April and October 2023.

Our newest credit score rating information offers proof of persistent will increase in default charges and re-leveraging of shopper debt. Whereas these rising rating tendencies don’t appear to be substantial sufficient in combination to materially transfer the nationwide FICO® Rating distribution downwards, they had been important sufficient to trigger the nationwide common FICO Rating to drop by one level in late 2023. Whether or not this common rating drop is an anomaly, or an early warning of an inflection level in shopper reimbursement conduct will rely upon a number of elements: will excessive inflation and elevated shopper costs proceed to put monetary stress on debtors and result in extra missed funds and elevated debt ranges, leading to a downward shift within the nationwide FICO® Rating distribution, or will the Federal Reserve’s rate of interest selections and the outlook of the roles market all through the brand new yr assist alleviate the financial uncertainty which shoppers are dealing with right this moment?

FICO will proceed reporting on these rating tendencies and is dedicated to serving to lenders higher perceive the credit score danger that every borrower represents and make better-informed lending selections. By means of portals equivalent to myFICO.com and packages equivalent to Rating a Higher Future and FICO® Rating Open Entry, we are going to proceed to coach and empower shoppers. We proceed to take a position closely in secure and accountable monetary inclusion by providing various data-driven options equivalent to FICO® Rating XD and the UltraFICO™ Rating to offer tens of millions of shoppers with an onramp to mainstream credit score.

To be taught extra about FICO® Scores, try these assets:

How is FICO serving to with monetary inclusion?

The FICO® Rating is Constructed to Final

FICO® Scores vs. Credit score Scores

[ad_2]

Source link